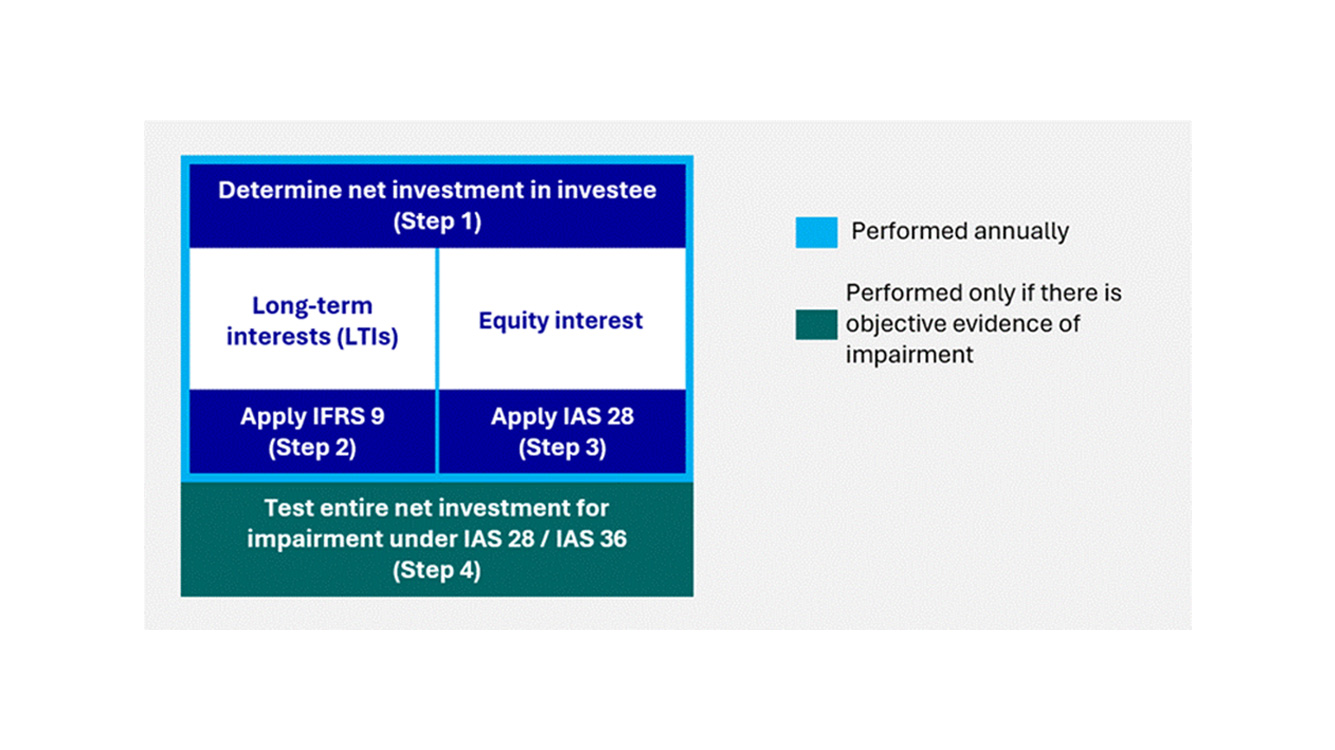

Step 4: Assess net investment in investee for impairment

An investor assesses whether there is an indication that its net investment in the associate or joint venture is impaired. IAS 28 provides potential indicators, including (but not limited to) significant financial difficulty of the investee, and significant adverse changes in the technological, market, economic or legal environment in which the investee operates.

If objective evidence of impairment exists, the investor performs an impairment test. The net investment (as determined in Steps 1 to 3) is tested as one single asset under IAS 36, by comparing its carrying amount to the recoverable amount. The carrying amount includes any fair value adjustments and goodwill arising from the acquisition of the investment – i.e. the goodwill is not tested separately or allocated to a larger cash-generating unit.

Recoverable amount is the higher of value in use and fair value less costs of disposal. An investor may determine the value in use of the investment by calculating either:

- its share of the present value of the estimated future cash flows that the investee is expected to generate, including cash flows from the operations of the investment and any proceeds from its ultimate disposal; or

- the present value of the expected future dividend cash flows, together with any proceeds from the ultimate disposal of the investment.

The investor compares the recoverable amount with the carrying amount of the net investment after applying the equity method to determine any additional impairment loss. If the carrying amount of the net investment is higher than the recoverable amount, the investor recognizes an impairment loss on the investment as a whole.

Any impairment loss is subsequently reversed only to the extent that the recoverable amount of the investment increases.