Federal Reserve Reports: Supervision and Regulation; Financial Stability

Assessment of near-term risks and supervisory and regulatory priorities

Download the Regulatory Alert

Download PDFKPMG Regulatory Insights:

- Supervisory Findings and Ratings: Increasing number of LFIs deemed to be “well-managed” due in part to changes in the LFI rating system; decreasing numbers of outstanding MR(I)As across all institution sizes due in part to the ongoing MR(I)A review. Weaknesses identified across financial risk management practices (including capital planning and liquidity), operational resilience, and BSA/AML compliance.

- Regulatory “Modernization”: Forthcoming guidance and rulemakings to include a framework for permitted payment stablecoin issuers, capital and liquidity reforms, model risk management and AI-specific guidance, and expansion of the regulatory umbrella (e.g., increased oversight of private credit, access to Federal Reserve Bank accounts and services).

- “Salient” Near-Term Risks: As identified by the agencies and market participants, to include risks from cyber events, geopolitical conflicts, persistent inflation/higher-than-normal interest rates, AI related issues and opportunities (e.g., augmenting cyber threats), and private credit markets.

The Federal Reserve Board (FRB) has issued its Spring 2026 Supervision and Regulation Report and also its Spring 2026 Financial Stability Report.

The Supervision and Regulation Report assesses current banking system conditions, details regulatory developments, and describes the FRB’s supervisory priorities and actions, including:

- Continued capital and liquidity levels above regulatory requirements and strong profitability and loan growth.

- Ongoing modernization of the regulatory framework, including capital reforms and a risk-focused approach to technology advancement.

- Enhancements to impact supervisory effectiveness, efficiency, fairness, transparency, and public accountability.

The Financial Stability Report presents the FRB’s current assessment of the stability of the overall U.S. financial system, noting:

- Elevated asset valuation pressures, moderate vulnerabilities from borrowing by businesses and households, vulnerabilities from financial leverage, and moderate funding risks.

- “Salient risks” identified by market participants, including geopolitical risks, AI, private credit, persistent inflation/ higher-than-anticipated long-term interest rates, and cyber events.

Separately, the Office of the Comptroller of the Currency (OCC) issued its Semiannual Risk Perspective highlighting key risk themes facing OCC-supervised financial institutions, including credit, market, operational, and compliance risks.

Supervision and Regulation Report

The FRB’s Supervision and Regulation Report highlights include:

Banking System Conditions. The FRB states, “The U.S. banking system continues to maintain strong capital and liquidity levels while maintaining strong profitability and healthy loan growth...The vast majority of banking organizations continue to report capital levels well above applicable regulatory requirements through year-end 2025...Loan balances continued to grow steadily [while] loan delinquency rates increased slightly across several loan categories…Large banks reported strong first quarter 2026 earnings.”

Regulatory Developments. Regulatory developments include a(n):

- Interagency (FRB, OCC, FDIC) proposal on Basel III implementation and amendments to the U.S. standardized approach along with an FRB proposal on the global systemically important bank (GSIB) surcharge framework (see KPMG Regulatory Alert here).

- New policy statement on permissible activities for FRB-supervised state member banks.

- FRB proposal to codify removal of reputation risk from FRB bank supervision, following FRB’s announcement of its removal from examination programs in 2025.

- Interagency (FRB, OCC, FDIC) final rule amending the community bank leverage ratio (CBLR) framework (see KPMG Regulatory Alert here).

- Interagency (FFIEC members) proposal to revise the Uniform Financial Institutions Rating System framework, commonly referred to as CAMELS (see KPMG Regulatory Alert here).

Supervisory Developments. The FRB continues to tailor supervisory approaches based on size, complexity, business model, and risk profile. Supervisory programs have been updated following release of the Statement of Supervisory Operating Principles (SSOP) in October 2025 as well as an updated version issued in May 2026, which clarified standards for matters requiring attention or immediate attention (MR(I)As) and enforcement actions.

The FRB adds that it is engaged in a two-phase review of all outstanding safety-and soundness-related MR(I)As to identify misalignment with the SSOP—including issues that have already been remediated or pose no significant probability of significant harm to a banking organization’s financial condition. The review is intended to ensure consistent treatment across banking organizations regardless of asset size, complexity, business model, or risk profile. The FRB states that MR(I)As that are not aligned with the SSOP will be downgraded to observations or closed.

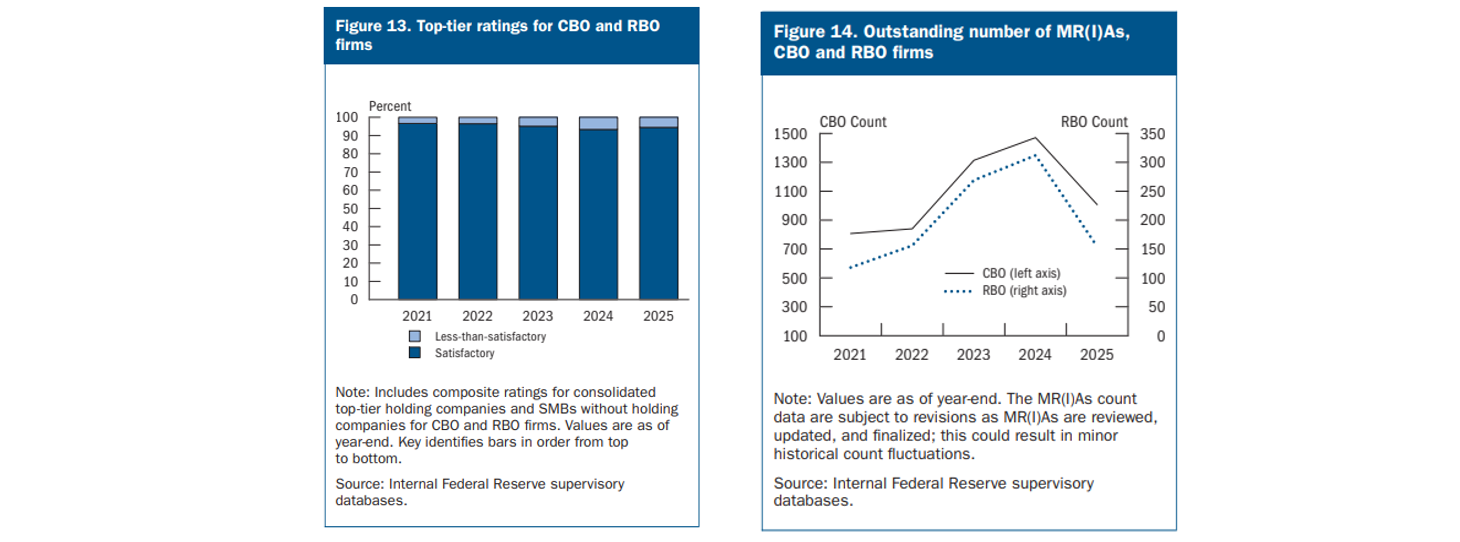

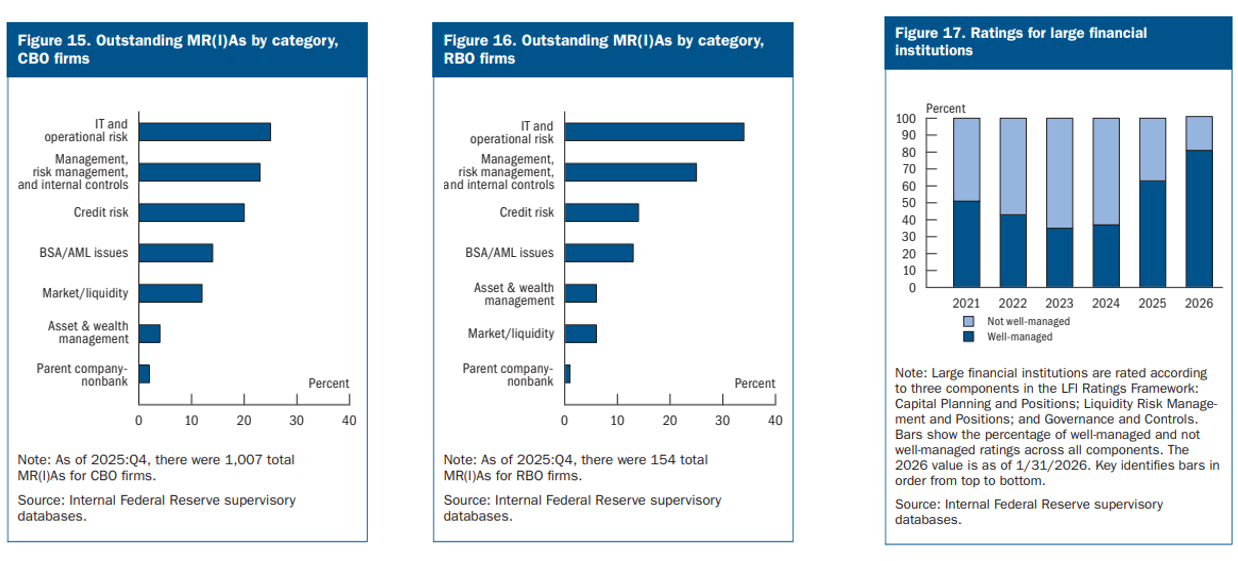

Trends in Supervisory Findings and Ratings. Using the LFI Rating System, most LFIs (Large Financial Institutions with $100 billion or more in total assets, including G-SIBs, and LFBOs (Large Foreign Banking Organizations) were deemed to be satisfactory across all three LFI rating components (figure 17) and were considered “well-managed.” The remaining LFIs were rated less-than-satisfactory in at least one component and were not considered “well-managed.” Following revisions to the LFI Rating System, effective January 16, 2026, the proportion of LFIs considered “well-managed” increased based on the revised definition. (See KPMG Regulatory Alert here.) Weaknesses were identified in financial risk management practices including capital planning and liquidity, operational resilience, and BSA/AML compliance. Outstanding MR(I)As at LFIs decreased in the second half of 2025.

Most CBOs (community banking organizations with less than $10 billion in total assets), RBOs (regional banking organization with total assets of $10 billion or more and less than $100 billion), and FBOs (Foreign Banking Organizations with combined U.S. assets of less than $100 billion) remain in satisfactory condition with effective risk-management practices and adequate financial performance (figure 13). The number of outstanding MR(I)As at CBOs and RBOs fell notably to levels roughly in line with levels prior to 2023; this trend has continued in 2026, due in part to the review of MR(I)As. For CBOs and RBOs, the largest number of outstanding MR(I)As were related to IT and operational risk, followed by risk management and internal controls (figures 15 and 16). For FBOs, the largest share of outstanding MR(I)As related to Bank Secrecy Act/anti-money laundering and Office of Foreign Assets Control compliance.

Near-Term Supervisory Priorities. The report outlines near-term supervisory priorities for LFIs, CBOs, RBOs, and FBOs. The core material and financial risks prioritized for supervision are outlined in the table below.

LFIs | CBOs and RBOs |

|---|---|

Capital planning and positions, including:

Liquidity risk management and positions, including:

Governance and controls, including:

Recovery and resolution planning | Credit risk, including;

Liquidity risk, including:

Other risks, including:

|

Bank Applications and M&A. The FRB adds highlights of bank application and mergers and acquisition (M&A) activity in 2025 to include:

- Review of 942 transaction applications, up from 807 in 2024.

- Approval of 145 M&A applications, up from 99 in 2024.

- Average processing time of 85 days for M&A applications, down from 101 days.

- Average processing time of 162 days for M&A applications requiring action by members of the Federal Reserve Board, down from 259 days in 2024.

Financial Stability Report

The FRB’s Financial Stability Report provides an overview of financial system vulnerabilities since the last report issued in November 2025, across four areas:

- Asset Valuations: Asset valuation pressures were elevated, though risk premiums increased in several markets. Equity valuations stayed high despite increased volatility. Corporate bond and loan spreads were low by historical standards, but credit concerns increased for riskier debt. Commercial real estate (CRE) prices continued to stabilize following significant declines, while residential real estate prices and farmland valuations were historically high.

- Borrowing by Businesses and Households: Vulnerabilities from business and household debt remained moderate. Total debt of businesses and households as a fraction of gross domestic product (GDP) continued to trend down. Business debt growth was flat; credit to small businesses was flat. Delinquencies remained above pre-pandemic levels. Outstanding household debt adjusted for inflation remained mostly stable; mortgage credit risk remained low, while consumer debt (e.g., student, auto, credit card) delinquencies remained elevated relative to the past decade.

- Leverage within the Financial Sector: Vulnerabilities associated with financial leverage were “notable.” Banks maintained historically high levels of regulatory capital; leverage at broker-dealers was “subdued;” leverage at large life insurance companies remained high; and hedge fund leverage remained near historical highs and concentrated in a small number of large firms. Bank lending to other financial institutions continued to grow “robustly.”

- Funding Risks: Funding risks remained moderate and in line with historical norms. Most domestic banks maintained high levels of liquidity and reliance on uninsured deposits was “well below” peaks in 2022 and 2023. Assets in cash-management vehicles continued to grow. Stablecoin growth was moderate. Central counterparties increased margin requirements during heightened volatility, but margin calls were met without difficulty. Life insurers non-traditional liabilities increased but remained a small share of assets. Some private credit vehicles saw increases in redemption requests.

Potential Near-Term Risks to the Financial System. The FRB identifies potential near-term risks, based in part on topics cited in its market outreach, “Survey of Salient Risks to Financial Stability.” Respondents identified cyber attacks and other cyber events, geopolitical risks and energy shocks, AI-related issues (e.g., equity valuations, labor market weaknesses), private credit (e.g., increasing pressure from investor redemptions) and persistent inflation.

OCC Semiannual Risk Perspective

The OCC’s Semiannual Risk Perspective identifies key issues facing national banks, federal savings associations, and federal branches and agencies. Trends identified include:

- Credit risk. Portfolio quality remained satisfactory across retail and corporate credit, with past-due and nonaccrual loan ratios and net charge-off ratios below long-term averages for most loan categories. Commercial real estate refinancing risk merits continued attention. Private credit markets show signs of weakening, including debt restructurings and paid-in-kind mechanisms that may mask deterioration.

- Market risk. Net interest margins improved across the banking system in 2025, driven by lower funding costs. Unrealized losses on securities portfolios fell to their lowest levels since 2021. Uninsured deposits increased modestly as a share of total deposits and remained in line with long-term averages.

- Cybersecurity. Threats from foreign state-sponsored actors and sophisticated cybercriminal groups targeting the financial sector appear as “notable” risks. Specific cybersecurity concerns arise from AI capabilities, which can increase the speed, scale, and sophistication of cyberattacks.

- Fraud risk. A key driver of operational losses. Financial institutions continue to face elevated levels and rising sophistication of fraud and scams, including impersonation scams facilitated by text messages and social media.

- Compliance risk. Geopolitical tensions may increase sanctions and money laundering risk, straining bank compliance systems and increasing the potential for sanctions and Bank Secrecy Act/anti-money laundering violations.

- AI. Financial institutions are generally using generative and agentic AI through specific use cases with guardrails and human-in-the-loop accountability. Broader AI use may present opportunities for core operational and customer service activities. Governance and risk management remain important given the needs and challenges of explainability, data privacy, cybersecurity, and validation for AI.

- Digital assets. The OCC continues to monitor digital asset activity, including payment stablecoins under the Guiding and Establishing National Innovation for U.S. Stablecoins Act.

- Bank performance. Bank profitability increased in 2025. Revenue growth accelerated, loan growth improved, and credit quality remained stable. Growth in net interest income was a key driver of profitability. Funding costs declined, while loan growth accelerated.

Figure 13. Top-tier ratings for CBA and RBO firms

Figure 14. Outstanding number of MR(I)As, CBO and RBO firms

Figure 15. Outstanding MR(I)As by category, CBOO firms

Figure 16. Oustanding MR(I)As by category, RBO firms

Figure 17. Ratings for large financial institutions

Source: FRB Supervision and Regulation Report Spring 2026

Dive into our thinking:

FRB Reports: Supervision and Regulation; Financial Stability

Assessment of near-term risks and supervisory and regulatory priorities

Download PDFExplore more

Get the latest from KPMG Regulatory Insights

KPMG Regulatory Insights is the thought leader hub for timely insight on risk and regulatory developments.

Meet our team