Capital Proposals

Basel III Amendments, Revised Standardized Approach, GSIB Surcharge

KPMG Regulatory Insights

Net Capital Relief: The proposed revisions to the risk-based capital framework align more closely with the Basel standards and work together with other related rulemaking activity including stress testing and leverage capital resulting in a potential for net capital relief. Recalibration could create opportunities for banks to reassess binding constraints, release excess management buffers, and redeploy capital toward lending growth, balance sheet optimization, and M&A.

Simplification: Category I and Category II firms are no longer required to calculate two parallel sets (e.g., standardized and advanced approaches) of risk-based capital ratios, adopting a single approach, the “expanded risk-based approach.” Category III and Category IV firms retain a revised “standardized approach.”

Modernization: To better align capital with observed risk, operational risk is explicitly included in risk-weighted assets, using a business indicator-based component, including a noninterest component that downscales for certain treasury and investment services. Proposals to modify capital requirements for servicing and originating mortgages are intended to align capital requirements for traditional lending activities with risk.

Minimization: Although the stress capital buffer (SCB) remains applicable, operational risk losses and global market shocks would be adjusted in stress testing to minimize double‑counting between stress tests and proposed Basel III rules. Stress tests remain a forward-looking backstop, but with a lower SCB.

Implementation: While there is a 90-day public comment period, the proposals are generally silent to effective dates and implementation; given the expected overall “moderate” capital impact, there is potential for implementation to exclude a phase-in when effective dates are announced.

The Federal Reserve Board (FRB), Office of the Comptroller of the Currency (OCC), and Federal Deposit Insurance Corporation (FDIC) (collectively, “agencies”) have issued two joint proposals to revise and “modernize” the capital framework for banking organizations of all sizes. The agencies state the intent is to “better align regulatory capital with risk while maintaining the safety and soundness of the banking system.” The proposals include the:

In a separate but related release, the FRB proposes amendments to its rule that identifies and establishes risk-based capital surcharges for global systemically important bank holding companies (GSIBs). The GSIB Surcharge proposal would also amend the Systemic Risk Report (FR Y-15) and is intended to improve measurement of systemic risk in the GSIB surcharge framework.

The agencies are soliciting public comment on each of the proposals, with a common submission deadline of June 18, 2026. The proposals do not include proposed compliance dates.

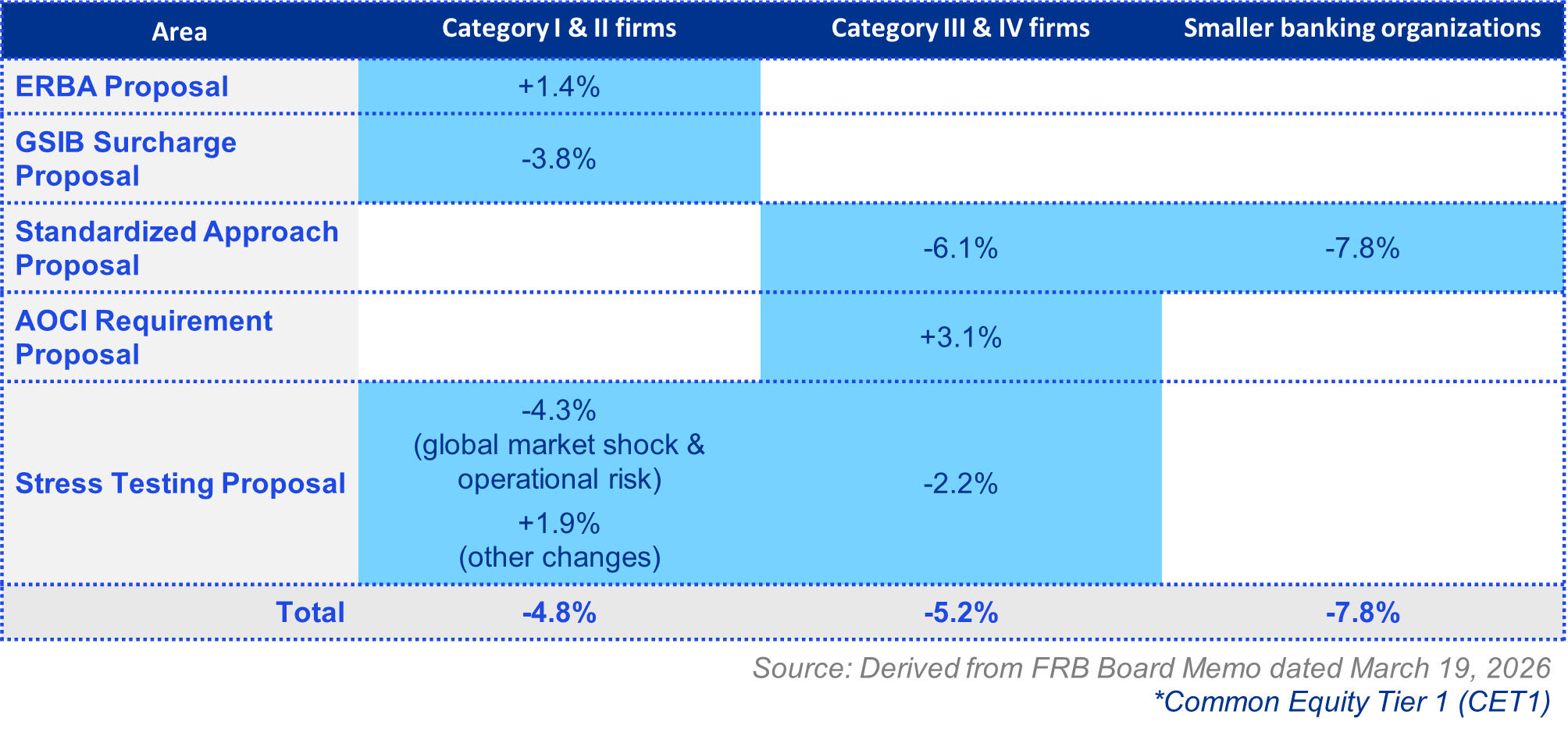

Cumulative Change in Aggregate CET1* Capital Requirements

The ERBA, Standardized Approach, and GSIB Surcharge proposals are intended to work together and also to take into account the aggregate impact of revisions introduced across multiple rulemakings:

Dive into our thinking:

Explore more

Subscribe to receive regulatory and compliance transformation insights

By registering you will periodically receive additional compliance-related communications from KPMG.

Meet our team