FinTechs, Innovation, and Federal Reserve Bank “Payment Accounts”

Executive Order and related FRB rule proposal

Download the Regulatory Alert

Download PDF

KPMG Regulatory Insights

- Eligibility: While the Executive Order and FRB proposals have similar themes, they do not directly correlate. The Executive Order asks FRB to consider whether Reserve Bank accounts and services may be extended to non-bank financial companies, which are not currently eligible institutions; the current FRB proposals add account options for only currently eligible institutions. Potential impacts from both could expand the scope and access to FRB’s payment system but for two different audiences.

- New Limited Option: The FRB proposed special-purpose payment account is expected to offer a more streamlined review process compared to the traditional Master Account though Tier 2 and Tier 3 institutions must still anticipate a 90-day (or more) review period.

- Strategic Opportunity: Fintechs, stablecoin issuers, and developers of innovative payment models have opportunity to inform the final rule and potentially the FRB’s report on non-bank financial company access to Reserve Bank accounts/services.

The Administration recently issued Executive Order 14405, entitled “Integrating Financial Technology Innovation into Regulatory Frameworks.” The Executive Order lays out the Administration’s policy to “streamline regulatory processes, reduce unnecessary barriers to entry, and encourage collaboration between fintech firms, federally regulated financial institutions, and federal financial regulators.” To that end, the Executive Order has two primary directives:

- Streamline regulatory processes - Identify existing regulations, guidance, supervisory practices, and application processes across the federal financial regulators that might be updated to enhance fintech access to financial services (e.g., through partnerships, charters, products, and services).

- Expand access to Federal Reserve services - Evaluate, report, and establish procedures for uninsured depository institutions and non-bank financial companies to access Federal Reserve Bank payment accounts and payment services.

Following the Executive Order, the Federal Reserve Board (FRB) issued three proposals that together would facilitate the offering of a new special-purpose payment account (Payment Account) to clear and settle payment activity. The proposals include revisions to:

- The Policy on Payment System Risk and Account Access Guidelines

- Regulation A (Extensions of Credit by Federal Reserve Banks)

- Regulation D (Reserve Requirements of Depository Institutions)

The agency states the proposals are intended to support private-sector innovation in payments and are primarily directed toward non-federally insured depository institutions interested in direct access to Reserve Bank accounts and services.

Comments will be accepted through July 27, 2026.

Executive Order: Integrating Financial Technology Innovation into Regulatory Framework

For purposes of the Executive Order, the following definitions apply:

- “Fintech firm” – would mean a non-bank company that uses or develops technological means to offer or support the offering of financial products or services, including any application or technology that facilitates access to, management of, or data processing for financial products or services. Such financial products or services may include payment processing, lending, deposit-taking, derivatives, investment management, brokerage services, underwriting and capital-market activities, custodial and fiduciary services, digital banking, digital asset-related services, securities and commodities market activities, and blockchain-based services.

- “Federal financial regulators” – would mean the Commodity Futures Trading Commission, Consumer Financial Protection Bureau, Federal Deposit Insurance Corporation, National Credit Union Administration, Office of the Comptroller of the Currency, and the Securities and Exchange Commission as well as the Federal Reserve Board.

Streamline Regulatory Processes – Each federal financial regulator is required to take the following actions:

Action Required | Timeframe |

|---|---|

| 90 days |

| 180 days |

Access to Federal Reserve Services – The FRB is directed to:

Action Required | Timeframe |

|---|---|

| 120 days |

| 180 days |

Proposals: Federal Reserve Special-Purpose Payment Account

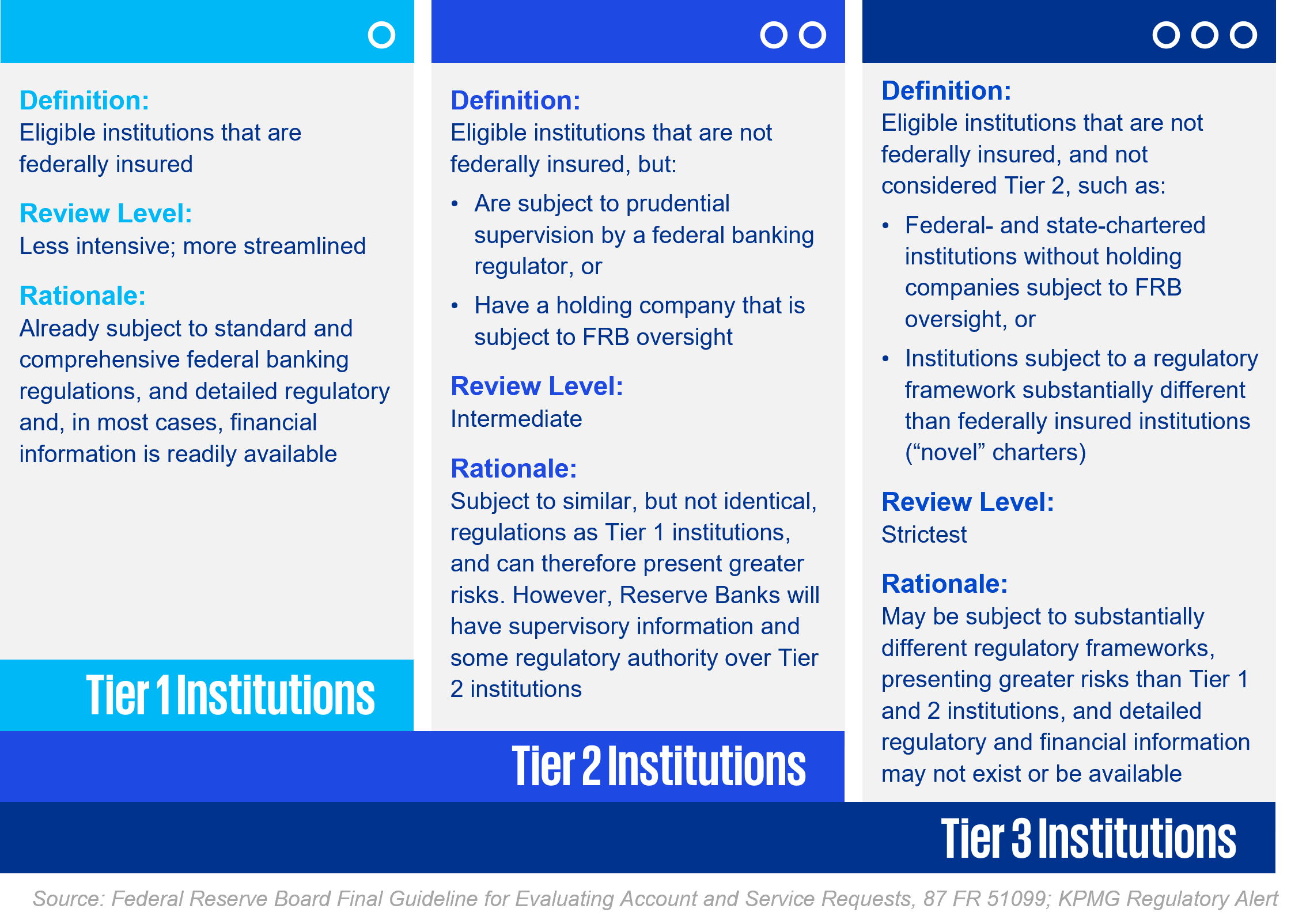

The proposals to establish the FRB Payment Account follow the 2022 release of the FRB’s Account Access Guidelines (Guidelines - see KPMG Regulatory Alert here), which established a three-tiered framework to guide Reserve Bank assessments of requests for accounts and services, as well as a recent request for information on a “prototype Payment Account,” which sought information on whether a tailored payment account could meet the needs of eligible entities that are not federally-insured (considered Tier 2 and Tier 3 institutions under the Guidelines) and also meet the material risks identified in the Guidelines (e.g., operational, liquidity, cyber, fraud, money laundering).

The FRB summarizes that the proposed Payment Account would facilitate access by eligible institutions, including uninsured depository institutions, to Federal Reserve services for clearing and settling payment activity, subject to a standardized set of terms that together would reduce the operational complexity and residual risk profile of the Payment Account relative to a Federal Reserve Master Account. Reserve Banks would be expected to continue to assess all account requests, including Payment Account requests, against the Guidelines.

The three rule proposals would work together, with amendments to the Payment System Risk Policy (PSR Policy) and Guidelines including references to the Regulation A and Regulation D amendments that would implement certain standardized terms for Payment Accounts. Key features follow.

Topic | Payment Account Standard Terms – As Proposed | Implementing Document |

|---|---|---|

Eligibility | Institutions that are legally eligible under the Federal Reserve Act or other federal statute to maintain an account at the Reserve Banks and receive services.

| Federal law |

Closing Balance | Closing balance limits would be set by the Reserve Bank based on expected payment activity in the account, though subject to a limit of $1 billion. There would be no limit on intraday balances.

| PSR Policy |

Intraday Credit | Access to intraday credit would not be permitted. Transactions that would cause an overdraft would be rejected.

| PSR Policy |

Available Services | Only those services for which the Reserve Banks can automatically reject transactions that would cause an overdraft would be permitted to settle in a Payment Account (i.e., currently, the Fedwire Funds Service, the FedNow Service, National Settlement Service, and the Fedwire Securities Service for securities transfers free of payment).

| PSR Policy |

Prohibitions | A Payment Account holder may not act as a:

| PSR Policy |

Illicit Finance Risk | A Reserve Bank may require a Payment Account holder to provide (ad hoc or periodically) information to demonstrate its compliance with BSA/AML and OFAC requirements.

| PSR Policy |

Discount Window | Access to credit at the discount window would not be permitted.

| Regulation A |

Interest on Balances | Interest would not be paid on balances.

| Regulation D |

Excess Balance Account Participation | Participation in an excess balance account would not be permitted.

| Regulation D |

Request Review Timeline | Reviews of Payment Account requests from Tier 2 and Tier 3 institutions would generally be completed within 90 calendar days of receiving all requested documents.

| Account Access Guidelines |

Additional clarifications to the requirements for Payment Accounts include:

- Reserve Banks would not recognize third-party interests for Payment Accounts.

- An institution may only maintain one account except in very limited circumstances.

- Master Accounts do not have a standard set of risk-mitigating terms (although Reserve Banks have discretion to impose terms on Master Accounts) and are separate from Payment Accounts.

- Proposed changes to Regulation A would change neither the existing programs under which the Reserve Banks generally provide discount window credit (primary credit, secondary credit, and seasonal credit) nor the process for establishing the primary credit, secondary credit, and seasonal credit rates.

- The FRB is encouraging Reserve Banks to pause decisions on requests for Reserve Bank accounts and services from Tier 3 institutions until it has completed the policy development process on the Payment Account proposal.

Guidelines for Evaluating Fed Member Account & Services Requests

Dive into our thinking:

FinTechs, Innovation, and Federal Reserve Bank “Payment Accounts”

Executive Order and related FRB rule proposal

Download PDFExplore more

Get the latest from KPMG Regulatory Insights

KPMG Regulatory Insights is the thought leader hub for timely insight on risk and regulatory developments.

Meet our team