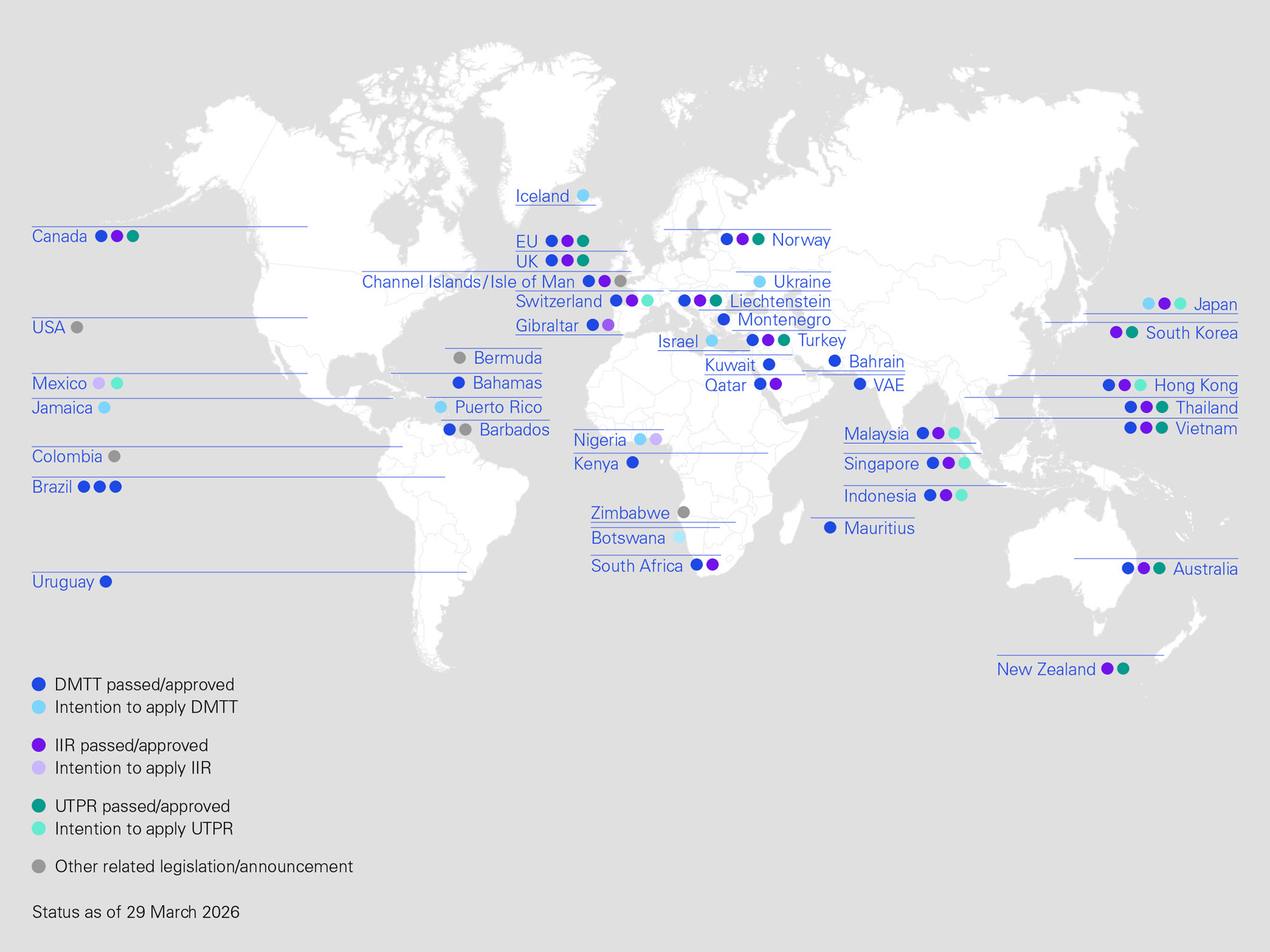

The process of implementing global minimum tax under BEPS 2.0/Pillar 2 continues alongside ongoing developments. Around 60 countries have already introduced corresponding regulations.

This includes Switzerland, where the qualified domestic minimum top-up tax (QDMTT) and income inclusion rule (IIR) have been implemented as core elements. At the same time, new developments are changing international framework conditions – in particular the side-by-side approach pursued by the US and new Administrative Guidance issued by the OECD.

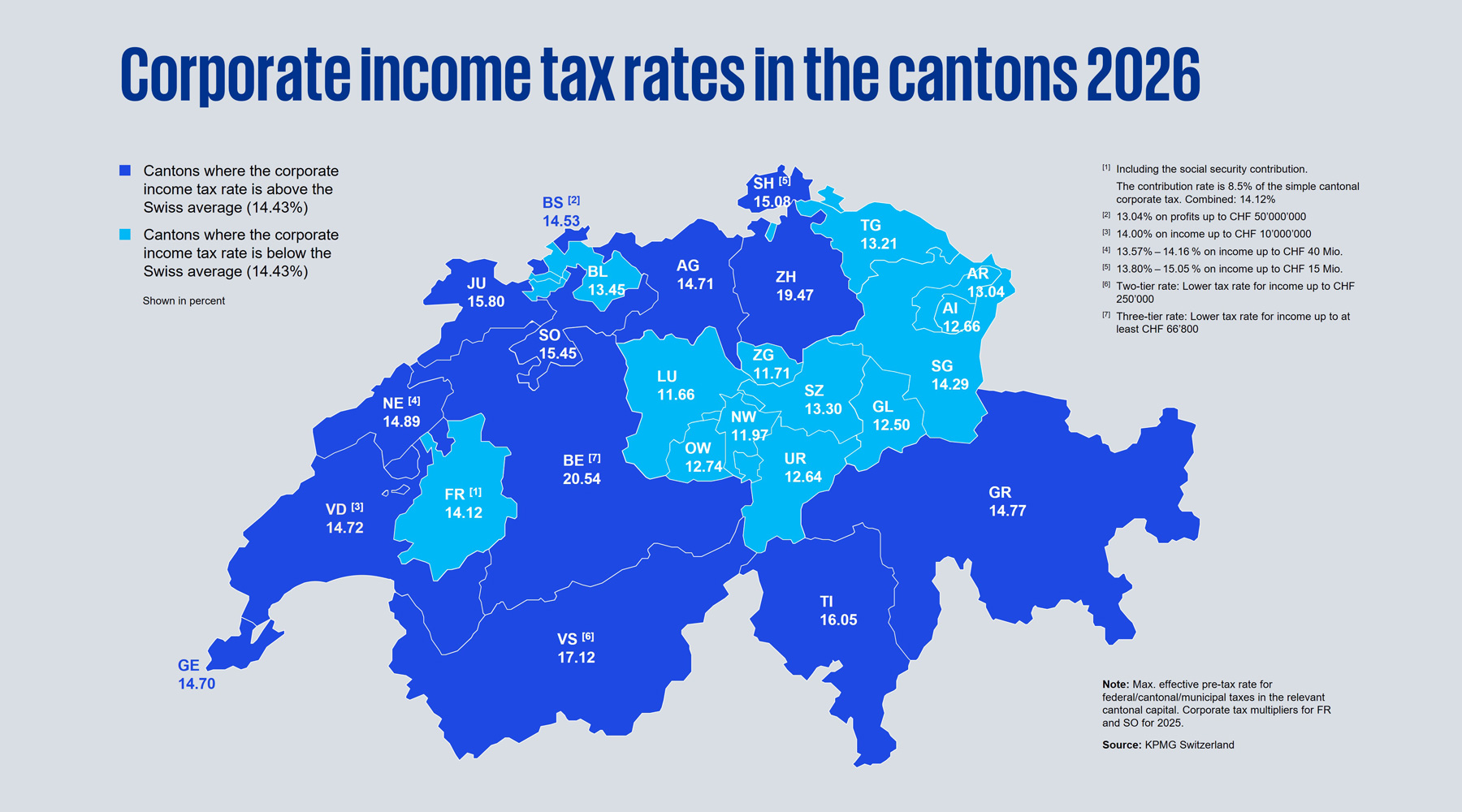

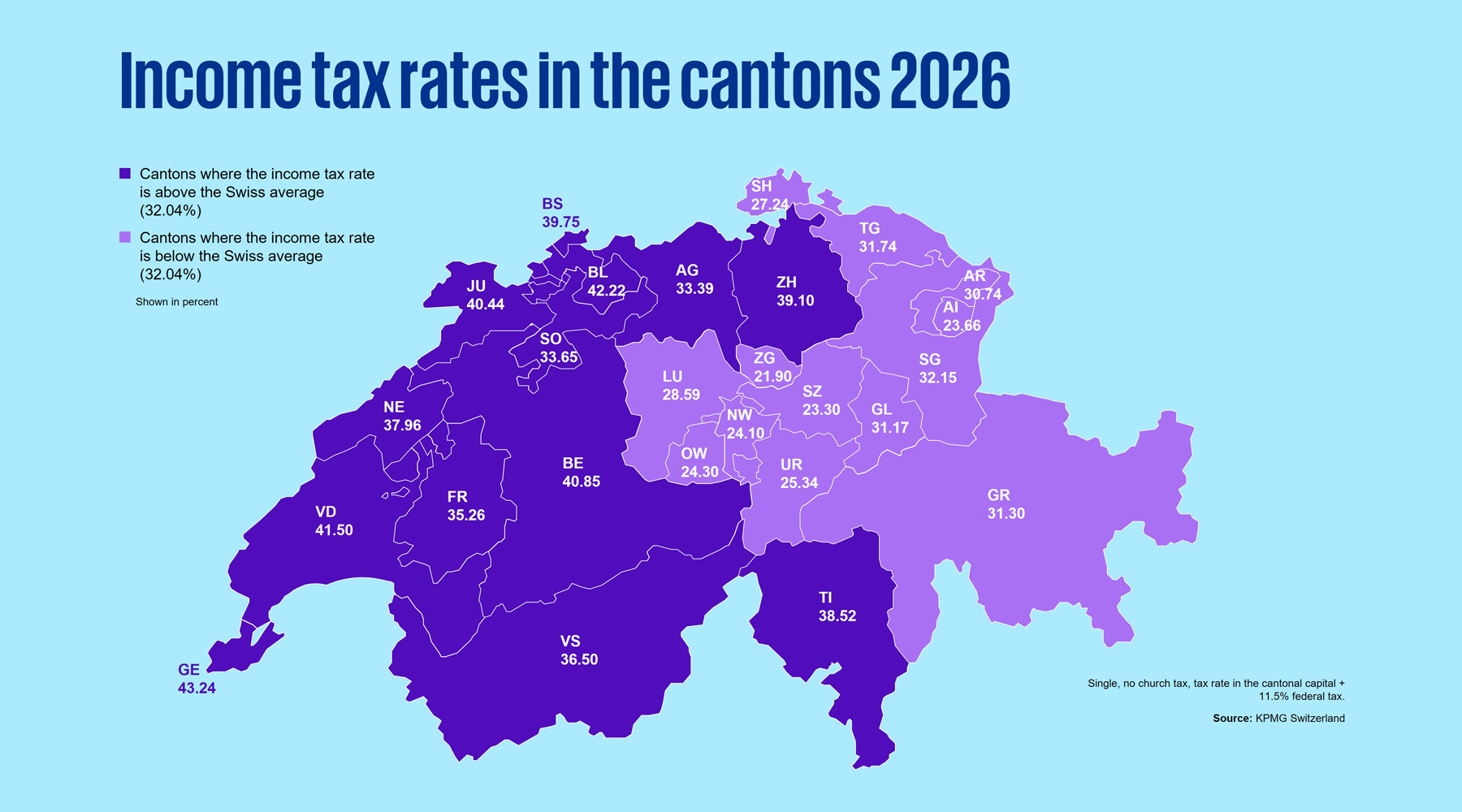

For Switzerland, then, the question is not just one of technical implementation, but of how to remain attractive as a business location. Several cantons are already responding with tax rate adjustments, QRTCs and other incentives, particularly in the area of research and development (R&D). Qualified tax incentives (QTIs) are also growing in importance as substance-based tax incentives may receive more favorable treatment under Pillar 2.

As conditional top-up taxes are not allowed, Switzerland will have to continuously re-evaluate whether the benefits of securing tax revenues in the country through the QDMTT outweigh the need to protect its position as a competitive tax location, especially compared to the US.