It has been another very strong full year result for the major Australian banks, who have continued to grow during the year, despite cash profits and net interest margins falling in the second half as strong competition and rising funding costs offset the benefits of higher interest rates.

Results summary

- Income

- Costs

- Liquidity

- Asset quality

- Shareholder returns

Income

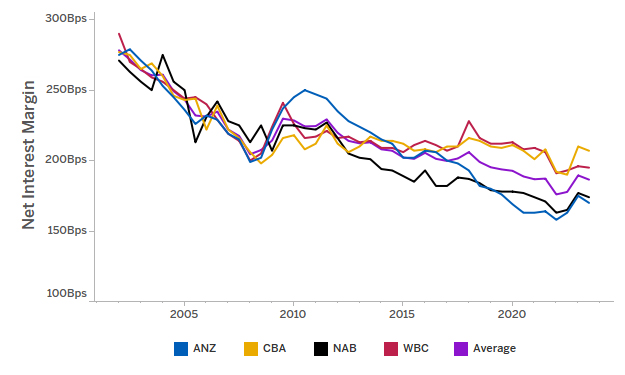

Net interest margins across the Major Banks continued to increase in FY23 by an average of 9 basis points compared with FY22. This is a result of improved interest earned on the loan portfolio driven by cash rate increases during the last 12 months. While net interest income has increased by 12.7% compared to FY22 to $74.8 billion, interest expense has increased by 504% compared to FY22.

Average interest earning assets increased by 7.3% from FY22 to $4.0 billion with all four banks reporting increases. This was driven by growth in both mortgages and non-housing (i.e. business and unsecured lending) in the period with portfolios increasing by 4.8% and 6.5% respectively across all the Major Banks from FY22.

Net interest margin

Costs

The average cost to income ratio decreased from 49.7% in FY22 to 46.3%. Overall, however operating expenses have increased by 3.9% compared with FY22 reflecting an increase in personnel costs which increased by $1,807 million (or 8.0%) from FY22, with headcount increasing by 1.9%.

Investment spending has been relatively stable across Major Banks. However, there has been an overall shift away from risk and compliance investment spend, with an increasing share of investment in productivity and growth initiatives.

Liquidity

Capital and liquidity ratios are well above regulatory minimums demonstrating balance sheet and liquidity strength. The average Liquidity Coverage Ratio (LCR) increased to 134.3%, up 3.75 percentage points from FY22 and the average CET1 is 12.5%, an increase of 88 basis points compared with FY22.

The average leverage ratio decreased by 2 basis points from FY22 to 5.3%, driven by an increase in exposures due to higher lending volumes. However, this was still well above the 3.5% APRA minimum requirement.

Liquidity coverage ratio

Asset quality

The Majors booked $2.8 billion in impairment charges in FY23, which is a turnaround from releases in FY22. This contributed to a 1 basis point increase in the average provisions as a percentage of gross loans and advances of 0.67% compared to FY22.

This is primarily due to an 8.7% increase in the Collective Provision, reflecting a shift in the forward-looking macroeconomic projections.

The 90 day+ delinquencies as a percentage of gross loans and advances increased to 1.91% as compared to 1.73% in FY22.

Provision as a percentage of Gross Loans and Advances (GLA)

Shareholder returns

Return on Equity (ROE) continued an upward trend in FY23 across the Majors. Average ROE increased by 85 basis points compared with FY22 to 11.7%, continuing the momentum from last year's ROE.

The Majors declared higher dividend payments in FY23 with an increase in the average dividend per share of 15.7% compared to FY22, resulting in an increase of 32 cents per share. Notwithstanding the increase in dividend payments across the Majors, the average dividend payout ratio has remained steady at 70.5%.

Return on equity

Download results snapshot

KPMG Major Banks insights

- Interest margins

- Cost pressure

- Credit quality

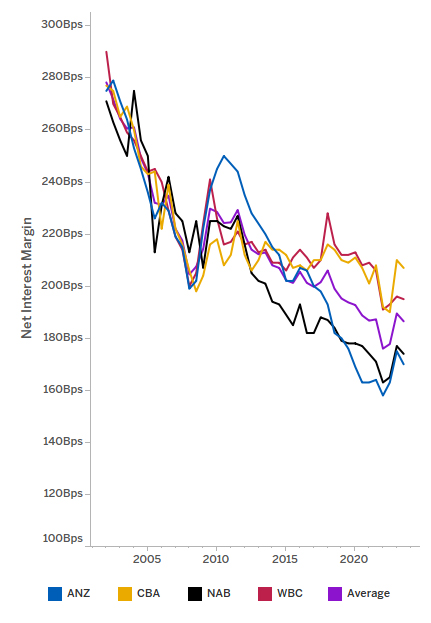

Interest margins have peaked, growth opportunities are limited

Overall the results from the Major Banks were strong, bolstered by increasing interest rates which reached their highest levels since 2012. However, consumer net interest margin (NIM) shows that interest income is through its peak, with declining NIM in the second half results for all Major Banks. The impact of competitive mortgage pricing and back book repricing, coupled with continued rising cost of deposits has tightened interest margins.

"We have seen great resilience and very strong results from the Major Banks this year. NIMs have been impacted by competitive pricing and rising cost of deposit funding and appear to have peaked in this rates cycle."

Major banks continue to battle cost pressure

Expense growth continues to impact the banks’ cost bases. In the first half of the year the majors re-based their expectations of costs in this environment to balance the need to invest for the future and drive productivity through strategic investment.

They are now turning their focus to transforming the cost base by lifting employee productivity, transforming and automating more of their underlying business processes and driving more tangible cost and efficiency ROI from their technology investments.

"Sustainable cost transformation remains at the top of the Banks’ agenda. Recent cost reduction activities have provided some immediate relief from inflationary pressures, with the more challenging sustainable transformation of the cost base now the focus."

Vincy Ng

Partner, Customer & Operations Advisory

KPMG Australia

Credit quality remains resilient

Australia’s resilient economy and high employment have dampened the impact of multiple interest rate rises on credit portfolios.

However, the small rise in early-stage delinquencies may suggest that interest rate rises and the erosion of savings buffers are starting to impact consumers.

The majors’ active management of customers moving from fixed to variable rates and accommodating hardship policies have so far mitigated the impact of the much discussed mortgage cliff.

The majors continue to monitor customer stress closely and take provisions for potential further economic softening given the lagged effect of rate rises to date.

"Arrears rates continue to tick up, but are still relatively small, demonstrating the resilience of bank customers to date. The majors are increasing forward looking provisions to prepare for the lagged impact of rate rises already in the economy."

Connect with KPMG’s banking specialists

- Item 1

- Item 2

- 3

- 4

- 5

- 6

KPMG's banking services and insights

Something went wrong

Oops!! Something went wrong, please try again

Frequently asked questions

The KPMG Major Banks Full Year Results Analysis will include the results from Australia's four largest banks: ANZ, Commonweath Bank (CBA), National Australia Bank (NAB) and Westpac (WBC).

This data is drawn from the big four Australin banks' financial statements and disclosures, augmented with financial statistics from The Australian Prudential Regulation Authority (APRA).