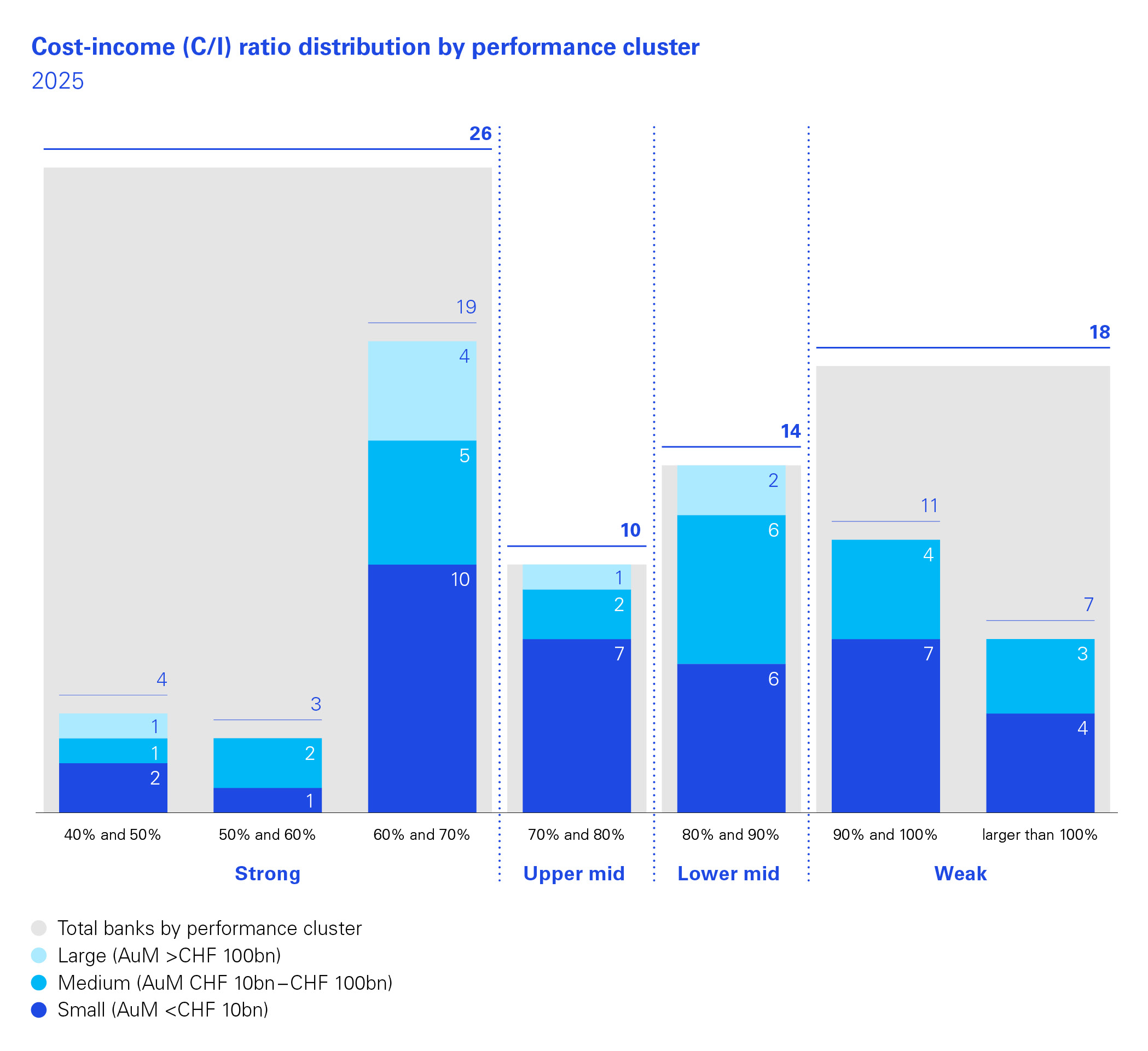

It is against a backdrop of great economic and geopolitical uncertainty that we carried out this year’s study of 68 private banks in Switzerland. The results are clear and positive: Swiss private banks are performing very well.

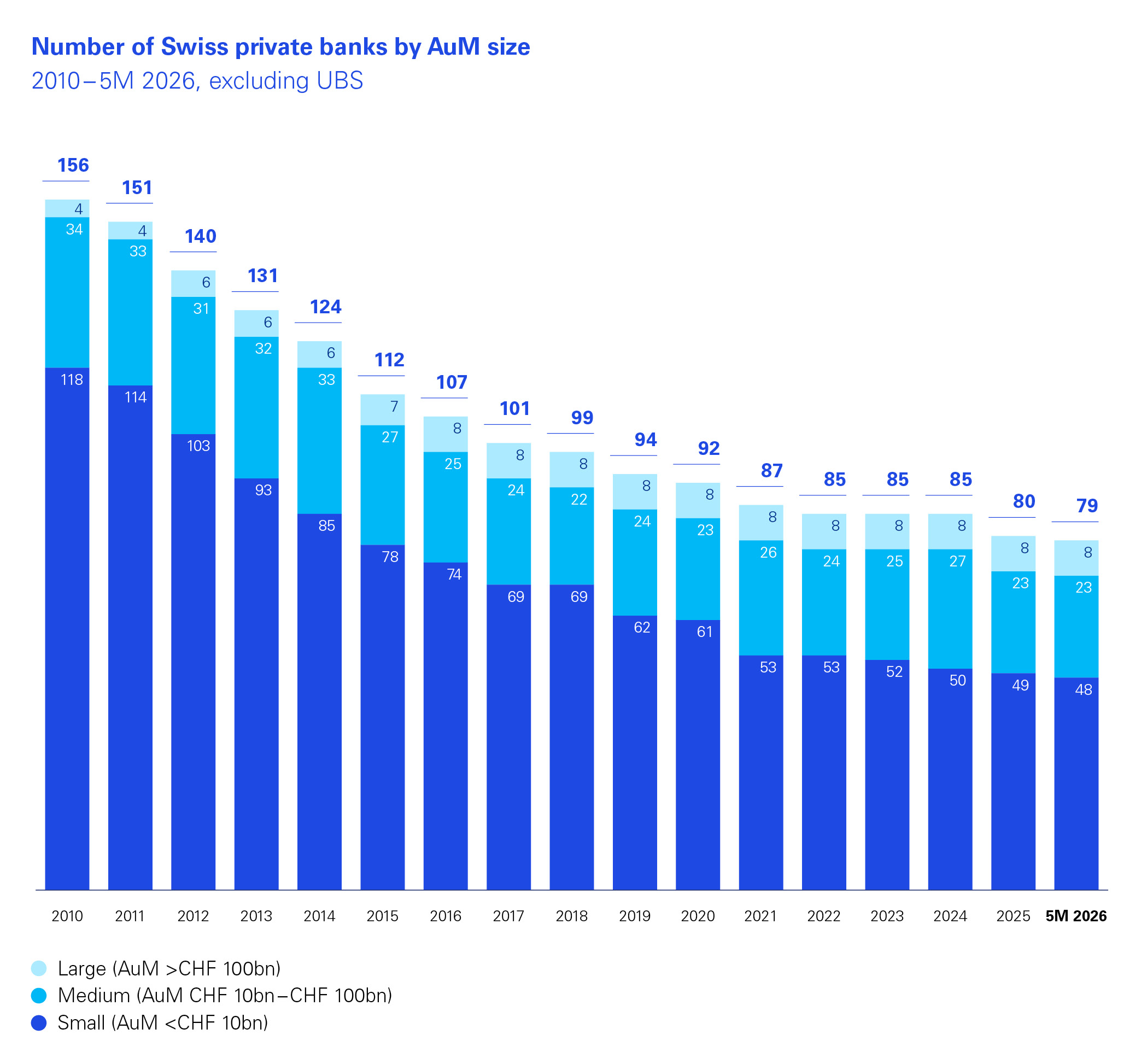

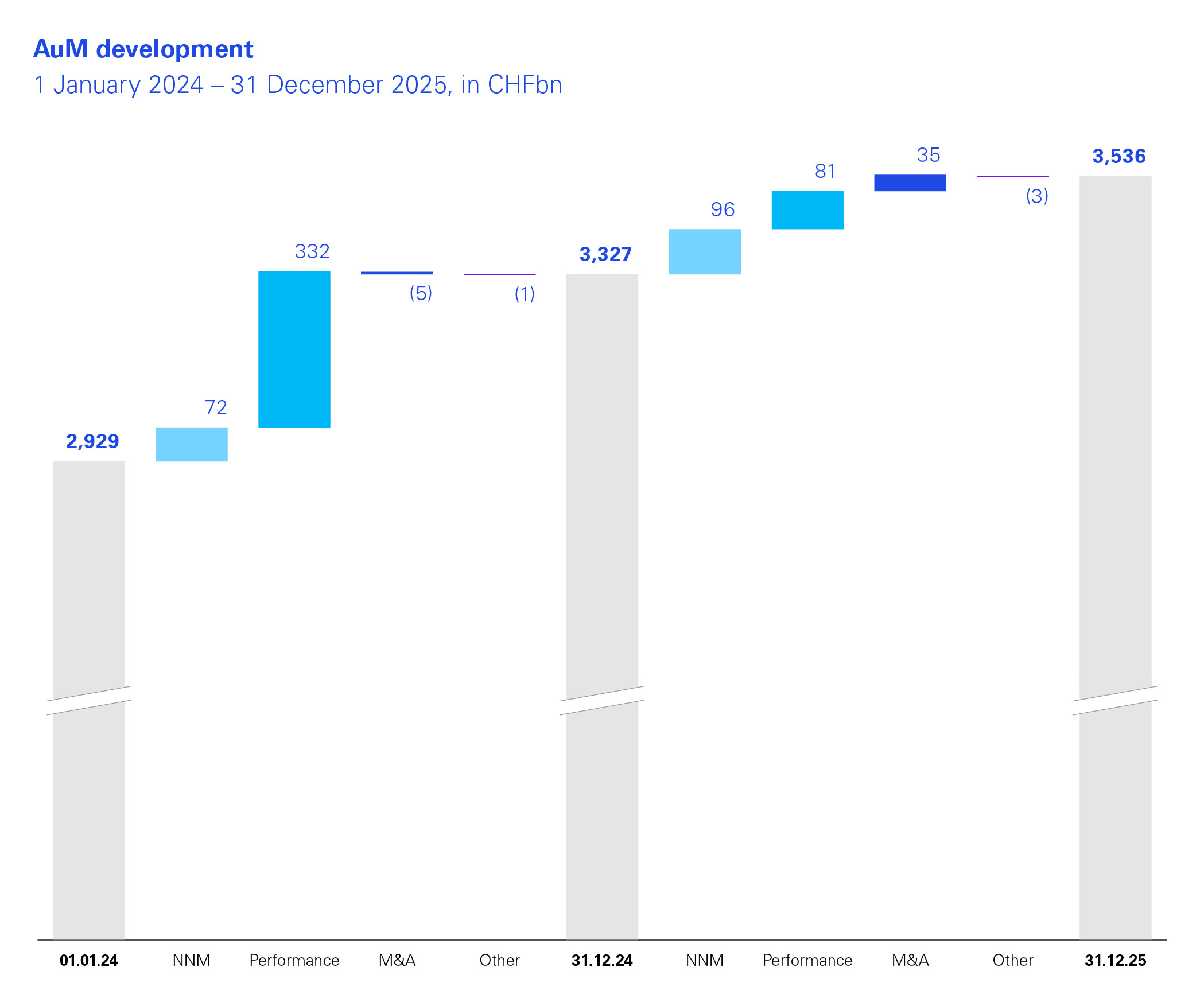

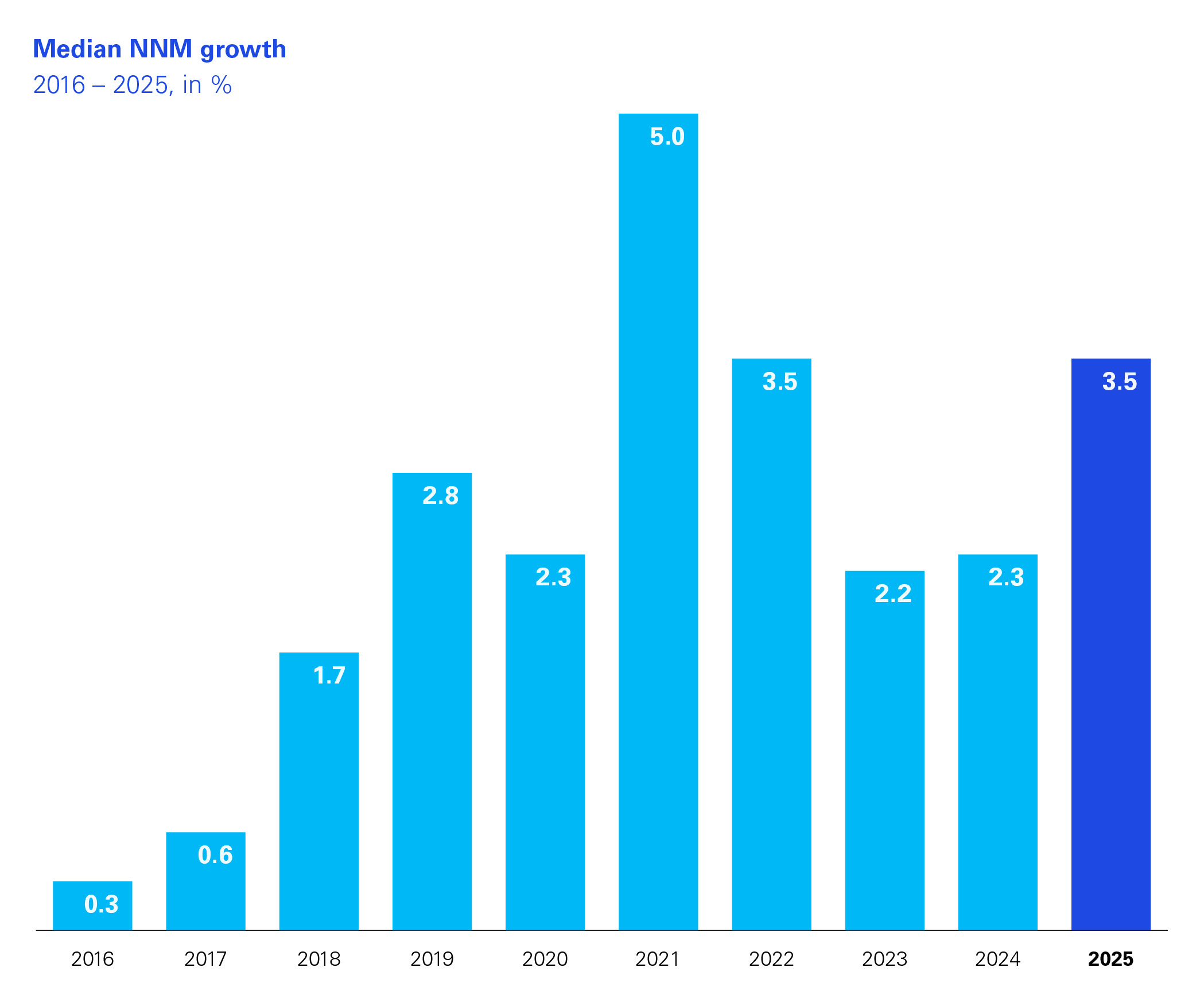

While banks may be struggling to maintain profitability and cost-income (C/I) ratios, they achieved a significant increase in net new money (NNM) last year, and assets under management (AuM) are at a record high. Consolidation also picked up pace, as the number of banks fell to 79 in 2026 – down from 156 in 2010.

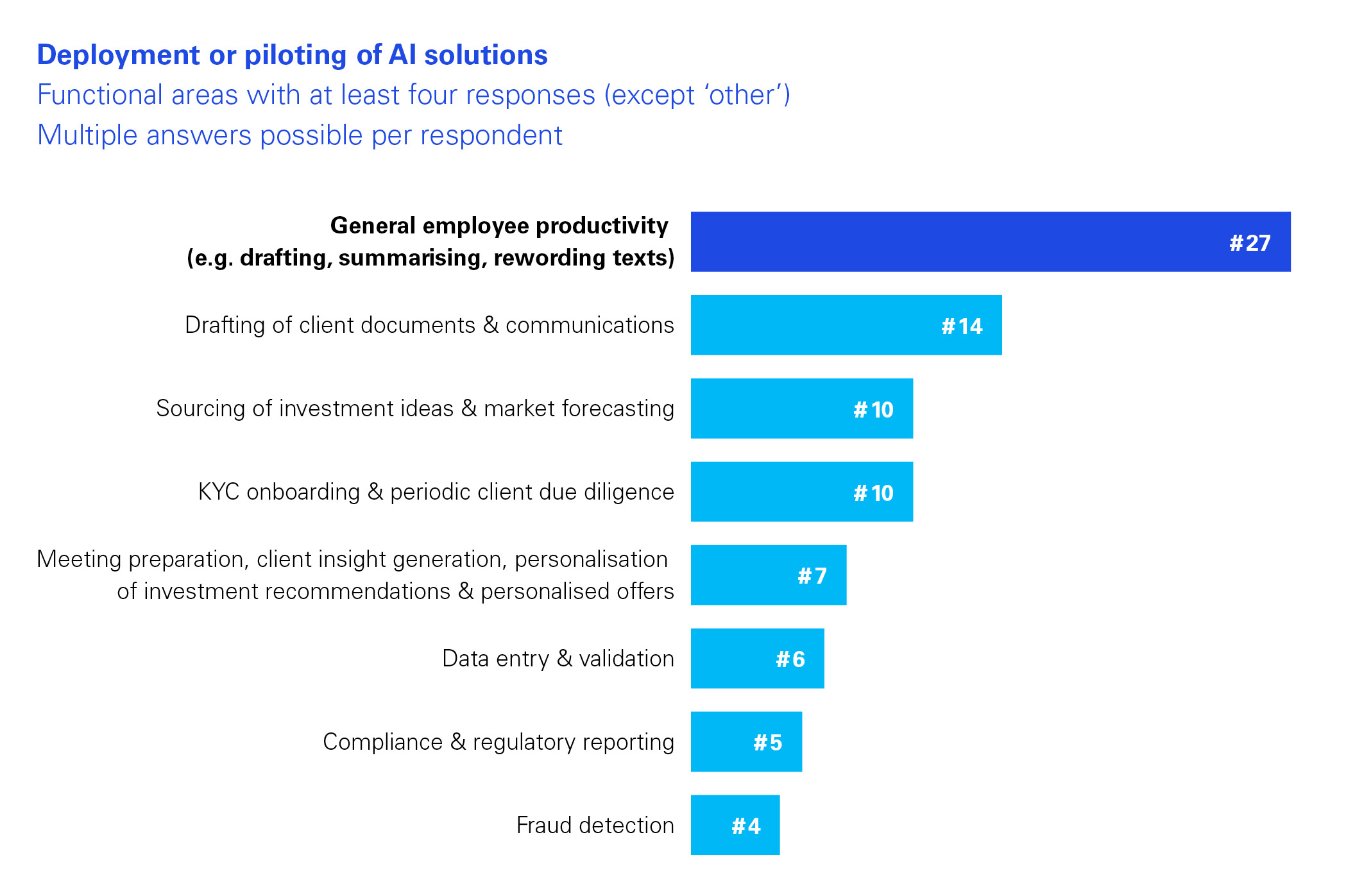

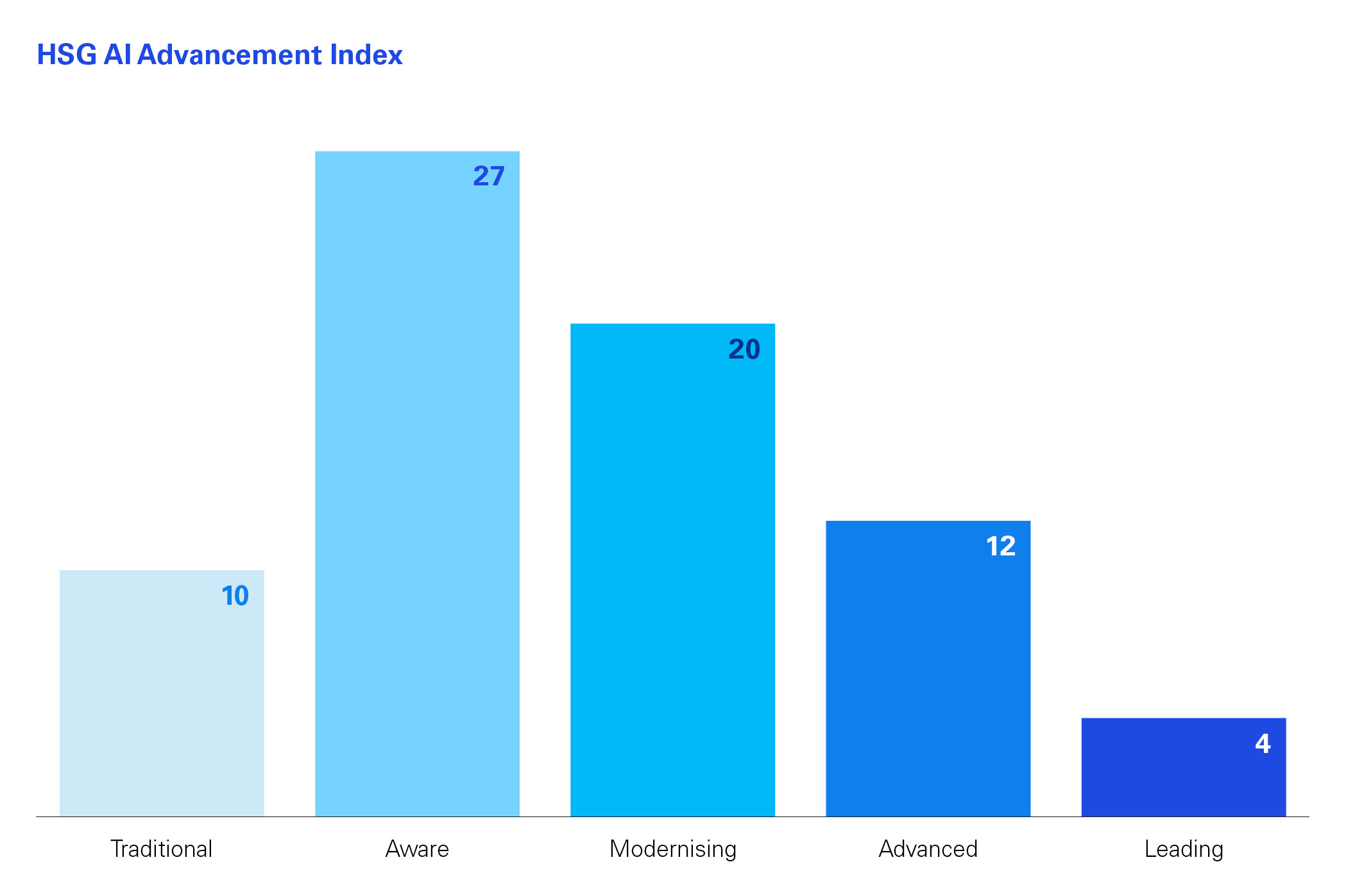

AI is one of the hottest topics around, and we wanted to provide analysis based on fact rather than speculation. We therefore surveyed a number of private banks on their use of AI, and the HSG Institute of Management and Strategy performed a deep dive as part of this study.

Their new AI Advancement Index categorizes Swiss private banks based on their AI maturity and finds that only a handful are advanced or leading.