Markets & Competition

- Market Disruption

- Fair Competition & Trade

- Regulatory Perimeter

- Actions

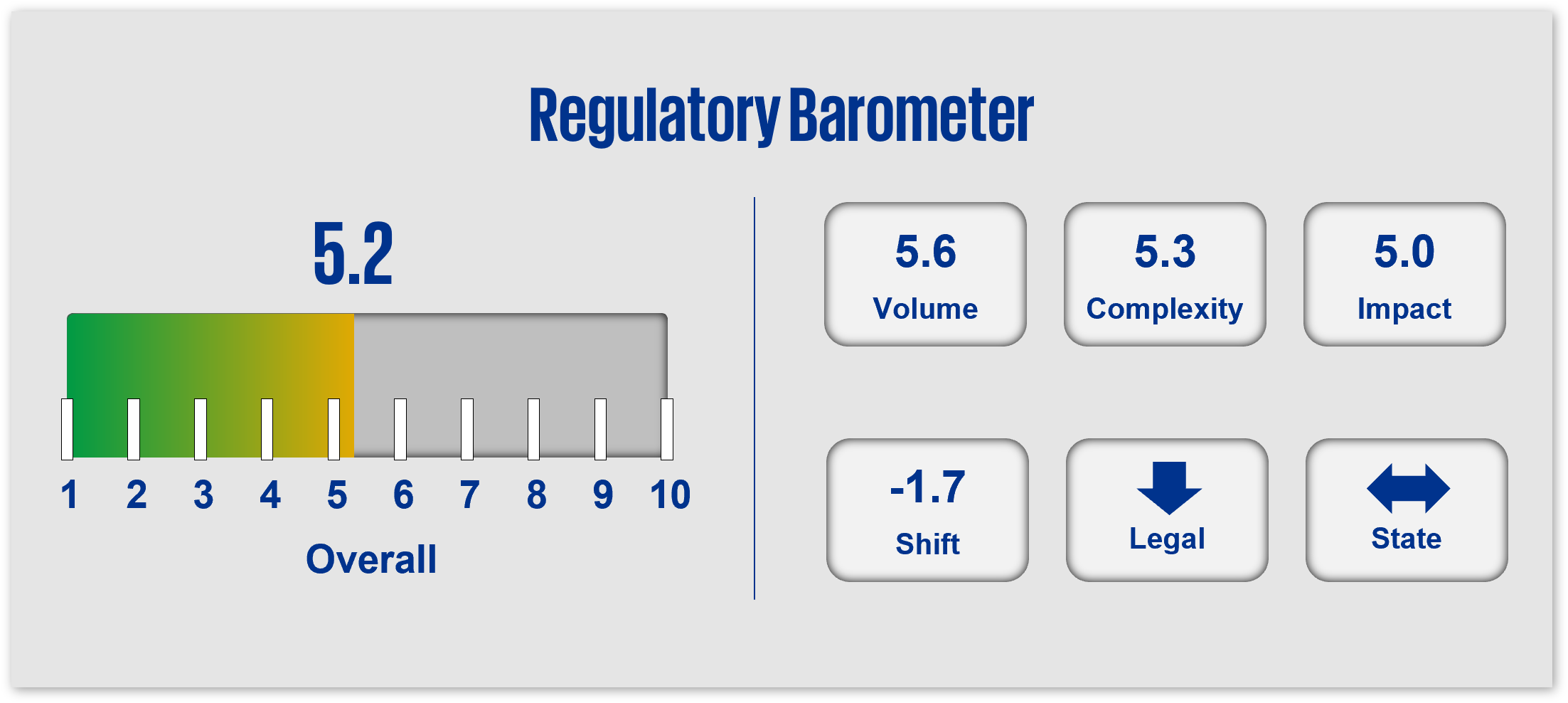

Regulators look to promote “fair” market competition and minimize “harmful” competitive impacts through antitrust/ anticompetitive laws. Federal regulators intensified their scrutiny of M&A activities using these laws, and looked to expand their existing authorities, risk standards, and frameworks to include “non-traditional” competitors. A rise in legal challenges disputing regulators’ jurisdictional authorities, coupled with the Loper Bright decision, has limited these efforts; this, in combination with the priorities of the new Administration, may alter the focus on, and pursuit of, antitrust/anti-competitive supervision and enforcement in some industries in 2025. State activity/ scrutiny, however, will likely continue; expect states to focus on managing risks associated with rapid innovation, consumer protection, transparency, and fairness.

1. Market Disruption

In today's dynamic business environment, the landscape of markets and competition is continuously evolving, shaped by a variety of forces such as legislation, regulatory change, M&A activity, new technologies, geopolitical events, and consumer demand. Regulators are concerned with addressing the challenges of market disruption, compliance with antitrust and anti-competition laws, and ensuring that novel market dynamics do not undermine fair competition or consumer interests.

Antitrust/Anticompetition

Market disruptions challenge the status quo of industries and market practices. Across industries, regulators, including enforcement agencies, assess proposed M&A transactions for potential anticompetitive/ adverse outcomes such as:

- Increased costs for consumers, making products and services less affordable/available.

- Limited choices for consumers, as fewer providers operate in the market.

- Suppression of competition or shift toward increased consolidation and/or monopolization, hindering healthy market dynamics.

- A reduction in innovation, as monopolistic entities have less incentive to innovate.

- Elimination of nascent competitors, which can stifle new and innovative market entrants.

- Harms to markets for workers, creators, suppliers, and other providers.

Discord/Instability

Constant flux in market conditions—be it geographic shifts, economic fluctuations, or the rapid adoption of new technologies like Generative AI—as well as increasing interconnectedness of business sectors/industries may place many companies in a reactive or responsive mode to market changes and potentially strain resource allocations and elevate risks.

2. Fair Competition & Trade

Regulatory efforts to increase transparency, promote fair competition, and ensure consumer and investor protections may ease in 2025, reflecting more favorable policies in some industries toward M&A transactions/reviews and related actions impacting market structure.

In particular:

Mergers & Acquisitions

Reviews of mergers and acquisitions transactions will continue to hinge largely on an evaluation of anticompetitive impacts, (informed by DOJ/FTC Merger Guidelines and Premerger Notification Rules, and FDIC and OCC Merger Policies) nuanced by the priorities of the administration, which may reflect a less stringent interpretation of those policies/positions, including:

- Concentration, measured from various perspectives such as geography, products/services, platforms, or supply chains.

- Competition, potentially including a broader definition of competitors (e.g., geographically relevant, other types of firms, markets for workers, creators, suppliers).

- Convenience and needs of the community, including assessment of impacts to different customer segments and continued availability of comparable products/services.

- Financial and market stability, especially in financial services where regulators may expect the resulting entity to be less financially risky than the individual merging companies and asset size will factor into the competitive analysis.

Anticipate the trajectory of M&A activities to continue to be shaped by macroeconomic conditions, such as interest rates, inflation, the administration’s priorities, and geopolitical events.

It is possible that as regulators review proposed M&A transactions, they may coordinate among themselves, aligned by industry (e.g., banking regulators) or with DOJ and/or FTC (e.g., under the 2023 Merger Guidelines), which could introduce some uncertainties to the review process (e.g., differing views on competitive effects, time to review).

Market Structure

Recent actions taken by regulators in an effort to maintain a fair, balanced, and competitive market environment, include:

- Federal/State Rulings: Actions to address antitrust/anticompetition issues related to monopoly power, market consolidation, limitations on consumer choice.

- SEC Market Structure Rules and Amendments: Rules and amendments to improve transparency in retail investment trading and provide retail investors with clear insights into the operations of the market (e.g., best execution, order competition, minimum tick size).

- FDIC and OCC Merger Policy Statements: Reiterating a principles-based standard for evaluating bank mergers, emphasizing a review process to safeguard against adverse impacts to competition and the financial system.

- FTC/DOJ Premerger Notification Rule: Amendments to provide greater insight into potential competitive effects of proposed M&A transactions both horizontally and vertically.

Notably, companies are rapidly innovating and reaching the market at a pace that exceeds regulators' abilities to monitor and manage many of these advancements, potentially leading to a company achieving a dominant position and stifling competition.

3. Regulatory Perimeter

As markets evolve and change, regulators must adapt. Examples that will likely continue into 2025 include:

Regulatory Expansion

In the financial services sector, banking regulators have looked to expand their supervisory and enforcement activities to encompasses new products/services/activities (e.g., credit, bank-nonbank BAAS agreements) and “non-traditional” competitors (e.g., technology providers, payments providers, fintech and Insurtech companies, and nonbank service providers along with the growing presence of private funds and “shadow banks”). In the short-term this trajectory is likely to continue (though may change in time).

Given the new Administration, expect evolving changes to regulatory contraction/expansion depending on industry and sector.

New Laws and Regulations

In addition to leveraging existing rules and risk standards, individual states are adopting new laws and regulations to address emerging challenges and expand jurisdictional authority in areas such as fair banking practices (e.g., Florida), AI (e.g., Colorado, Tennessee), cybersecurity (e.g., New York), and sustainability (e.g., California, Texas). Often provisions/standards adopted in one state will serve as a model for other states.

Complacency with Growth

Even amidst regulatory change, regulators will continue to focus attention on risk management (financial and non-financial), governance, and controls for companies exhibiting:

- “Persistent weaknesses” (e.g., multiple enforcement actions executed over successive years, failure to adhere to corrective actions).

- “Repeat offenses” (e.g., violations of terms or conditions in formal court or agency orders, “insufficient” progress toward correcting deficiencies or violations).

While innovation and change continue to outpace the regulators, companies should expect regulators to take a retrospective view of risk management and controls compliance.

4. Actions

- Regulatory Impact Assessment: Determine the direct and indirect risks/impacts of applicable regulations and emerging regulatory trends to lines of business, third-party strategy, products, services, and technology and system readiness; execute on changes, as appropriate.

- Compliance Management: Evolve risk and compliance programs (across lines) by revisiting the inputs and weights into risk assessments and new product and service reviews and approvals—all to consider inclusion, access, tangible benefit, and consistent and fair outcomes.

- Growth and Risk: Evaluate the relationship between growth and risk coverage to ensure efficient deployment of scarce resources (i.e., gearing ratio).

- Effects on Competition: When engaging in M&A activities, ensure preparedness through explainability of both the quantifiable and nonquantifiable effects on competition (e.g., access, product/ service availability, pricing, employment, supply chain resilience). Focus on access to money – through branch and ATM access post any M&A activity.

- Parties and Providers: Monitor risk profiles of parties, providers, and intermediaries on a regular basis, including assessment of changes in the business environment (e.g., concentration, interconnectedness via nth parties and supply chains, data ownership); expand party/ provider relationships to prevent over-dependence on one party/ provider or industry and promote market competition; focus on the growth of third party providers who in and of their own service provisions could provide concentration risk (e.g., cloud providers).

Dive into our thinking:

Get the latest from KPMG Regulatory Insights

KPMG Regulatory Insights is the thought leader hub for timely insight on risk and regulatory developments.

Explore more

Meet our team