Fairness & Protection

- Access

- Clarity & Accuracy

- “Harm”

- Actions

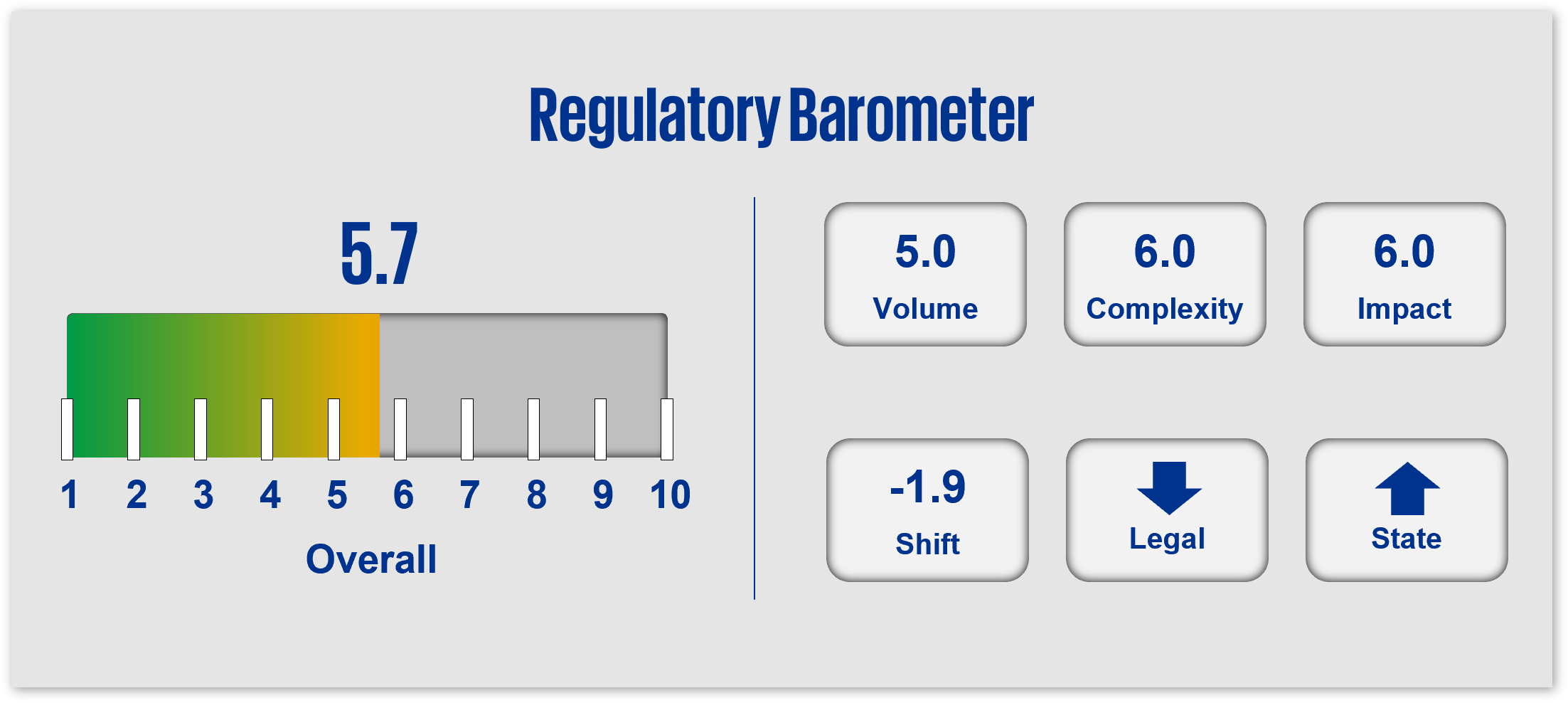

Agency leadership mission changes as well as the successful legal challenges to jurisdictional authorities have delayed and/or limited the effect of certain consumer/investor protection regulations. Existing regulations will still necessitate effective risk and compliance involvement and controls inclusive of product development, marketing, sales, servicing, complaints/claims management, and pricing/fees. The new Administration may look to redefine "fairness" and decrease “net new” federal regulatory activity in this area. Companies should anticipate an increase in state activity relative to individual consumer protections to fill perceived “gaps.”

1. Access

The growing number and kinds of companies offering customers similar products and services, and the fact that these companies may operate under different legal authorities that may not be obvious to consumers/investors, raises potential risks and concerns. As innovative and new product/service offerings expand (e.g., crypto and digital assets) it will be key for regulators to both allow for access and do so in a way that keeps sound the guardrails around national security and data protections.

Regulatory Perimeter

Applying existing rules, standards, and frameworks to a broader range of new and novel entities, business combinations/arrangements, and products and to both “close the gap” in regulatory coverage and facilitate/promote access to innovations/developments Examples anticipated in the financial services industry include actions (e.g., rulemaking, enforcement) related to:

- Models/systems, including content limitations, claims/statements, data quality/protections

- Crypto and digital assets

- Expansion of coverage given potential for change in areas such as sanctions, trade compliance, etc.

Examinations Scope

Changes in agency leadership and impacts to agency priorities (e.g., CFPB, FTC, DOJ) may impact examination priorities and/or intensity over time. Regulators will examine for demonstrable evidence of compliance with changes to regulatory expectations and rules in areas such as:

- New market structure rules (e.g., T+1 settlement cycle, Regulation NMS (order execution, minimum pricing increments, order competition)), including required disclosures and reporting.

- Product, service, and data/ information access (e.g., consumer opportunity to correct false/ fraudulent information, drug/ healthcare access and related “fair pricing”).

- Testing and monitoring of AI, models, algorithms, and other decision-making processes used in connection with consumer/investor products and services.

- Merger applications – though influenced by the priorities of the Administration, proposed transactions may be subject to the DOJ/FTC 2023 Merger Guidelines.

2. Clarity & Accuracy

Expect that regulators will continue to hold companies to the standard of “say what you do, do what you say” – and for that standard to be applicable over the full consumer lifecycle (e.g., design/development of new products/services, marketing, sales, servicing).

These efforts will be seen in 2025 around:

Transparency

Ongoing focus on the clarity, completeness, accuracy, and consistency of statements and claims made regarding products and services in related marketing, advertising, disclosures, and communications directed toward the consumer.

Enforcement

Evaluation of whether:

- Products and services are offered on substantially the same terms to all consumers/investors.

- Products/ services are fulfilled consistently as claimed/ marketed and terms/features are clear, prominent, “fair and balanced,” and not misleading to a “reasonable” consumer (e.g., use and capabilities of models and automated systems, deposit insurance claims and FDIC logo usage).

- Testimonials, endorsements, and third-party ratings in product/ service advertisements, marketing materials, and/or digital communications (e.g., websites, social media platforms) contain necessary/required disclosures (e.g., payment, affiliation).

- Fees are transparent and meet the requirements of existing laws, nor result in the potential for fraud, waste or abuse (e.g., particularly those in conjunction with government entities)

Consumer Reporting

Information reporting practices, including assessing processes and controls to:

- Ensure information accuracy and integrity and to mitigate against risk of loss of financial access (e.g., credit/debt collection practices.) due to errors or inconsistencies in reports.

- Provide consumers the opportunity to correct false or fraudulent information.

- Ensure timely investigations into issues (e.g., consumer complaints, unauthorized inquiries).

- Safeguard consumers against fraud, identity theft, and other scams/ risks.

3. “Harm”

Regulators expect companies to proactively and actively assess and mitigate the risk of harm to consumers/investors – both financial and non-financial - through their conduct, products, and services from a variety of perspectives including through design, terms, communications/ marketing, and support/ complaints management.

“Harmed Parties”

Regulators may ascertain potential and actual consumer harms through:

- Identification of potentially "harmed parties."

- Efforts to gauge the size/scale of potential impacts.

- Timeliness with which issues are identified, escalated, and resolved.

- Clarity of communications with “harmed parties.”

- Remediation and/or restitution.

- Analysis of root causes and related accountability.

Notably, as AI systems develop, the Administration and regulators are expected to focus more on trusted systems and potential security risks (e.g., cyber, privacy and national security) and less on “AI harms”.

Divergence

Regulators will continue to focus on complaints, claims, and disputes as a measure of “fair treatment,” evaluating the timeliness, substance, and completeness of responses, as well as the consistency of responses between consumer groups and the level of responsiveness/ fair remediation in disputes.

With regard to fraud-related disputes and investigations, regulators continue to focus on areas such as data sharing (e.g., large data models, data sharing with third parties and affiliates, customer permissioned sharing), payments authentication procedures, model development and validation, account holds and freezes, and ongoing oversight and monitoring of synthetic identity fraud.

4. Actions

- Access and Consumer Impact: Consider the impact of services at large and enhance access to a broader range of consumers in line with existing regulations and regulatory changes, and areas of focus anticipated under the new Administration.

- Appropriate Sales Practices: Confirm marketing and promotions are not misleading.

- Organization Disclosure: Ensure consumer commitments are upheld and that disclosures are clear, accurate, and transparent.

- The Consumer Lifecycle: Assess the consumer journey (i.e., marketing, originations, services, default), as well as use/dependencies of third parties/nth parties in the provision of goods and services to the consumer.

- Use of AI and Machine Learning: Develop standard principles that support the deployment of thoughtful, unbiased, and explainable AI.

Dive into our thinking:

Get the latest from KPMG Regulatory Insights

KPMG Regulatory Insights is the thought leader hub for timely insight on risk and regulatory developments.

Explore more

Meet our team