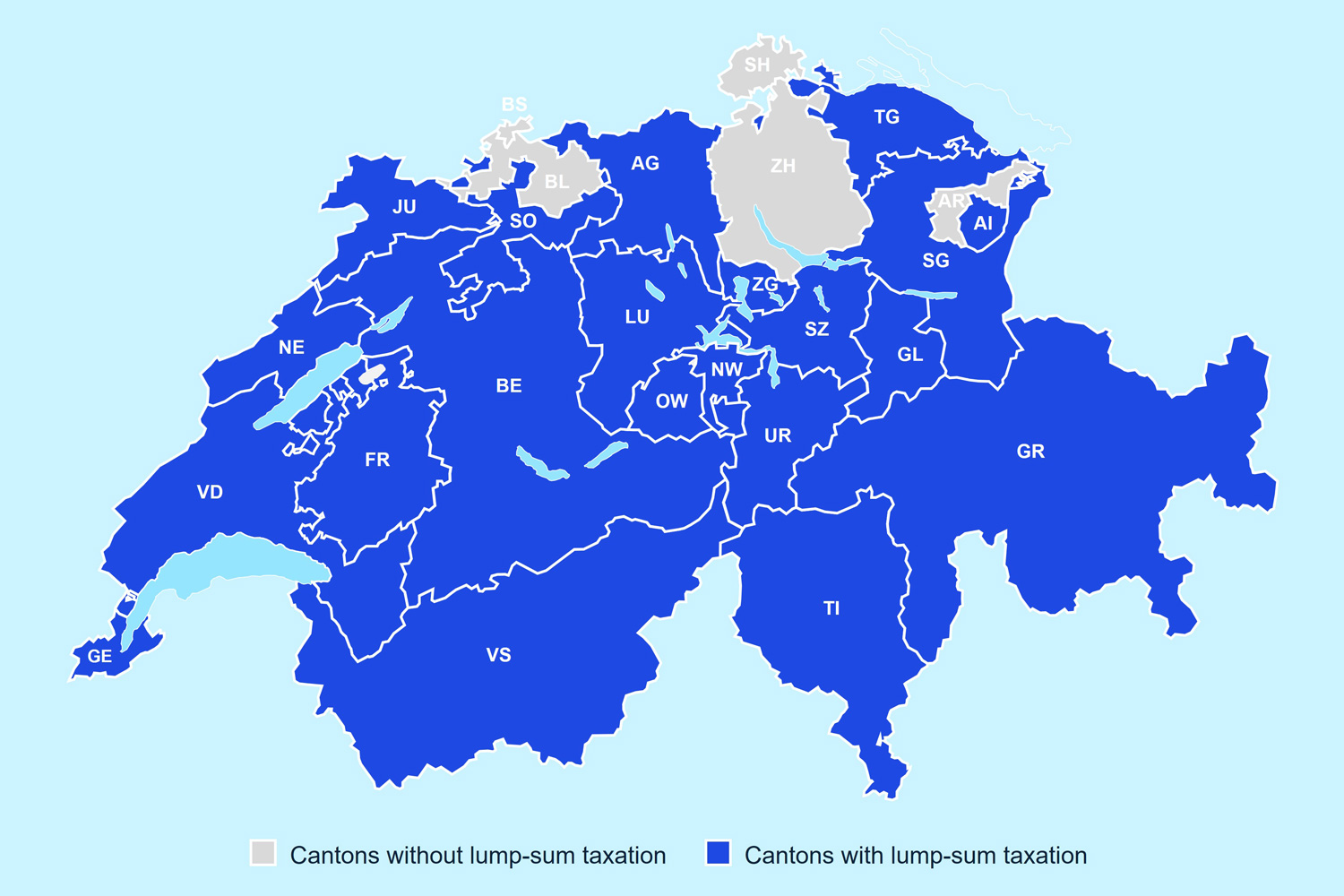

What is lump-sum taxation in Switzerland?

In international tax competition, the special tax regime of Swiss lump-sum taxation is an attractive tax model that attracts wealthy individuals to move to Switzerland.

Instead of basing taxes on global income and wealth, it uses the taxpayer’s living expenses as a surrogate tax base. This means that it is not necessary to report actual global earnings and assets. Once the tax base has been determined as explained below, it is then subject to ordinary tax rates. The resulting tax planning opportunities can offer very attractive outcomes.

Unlike ordinary income taxation, which requires full disclosure of global income and wealth, this system offers simplicity and confidentiality, with no need to report actual earnings or assets.