2024 KPMG U.S. CEO Outlook Pulse Survey

Anticipating and outpacing compound volatility

Overview

CEOs today are continuing to manage through the age of compound volatility, the combination of near-term risks and structural changes to the U.S. economy that raise business costs with little margin for error on strategy development and execution.

This year’s KPMG U.S. CEO Outlook Pulse Survey analyzed insights from 100 CEOs at large companies in the United States on the key challenges and opportunities in driving business growth with a lens into managing compound volatility.

CEOs are applying a strategic lens to tackle both near-term risks to growth they see such as geopolitics and cyber, and structural changes like new regulations including climate disclosure rules and tax policy, making adjustments to investments, supply chains and operations as needed – with many turning to generative AI (GenAI) to help do so.

They see GenAI as central to overcoming challenges resulting from compound volatility and gaining a competitive advantage and are working to rapidly advance its deployment across their enterprises in a responsible way to deliver productivity gains, re-shape business models and create new revenue streams. The implementation of initiatives to promote the responsible and ethical use of AI such as the use of watermarks/disclosures of AI use, data privacy measures, ethical frameworks and third-party reviews is a focus – and security is top of mind.

Business leaders are investing in GenAI training and capability building to upskill their people. They recognize workforce adoption will ultimately drive success with GenAI.

CEOs also are addressing another structural change – tight labor markets. With demographic shifts only beginning to take hold, the impact of tight labor markets on strategy will increase exponentially in the years to come. CEOs report they are addressing this challenge today by upskilling employees, using GenAI to fill talent gaps and dropping college degree requirements for certain jobs.

The mental well-being of the workforce and preventing burnout remain priorities. In the ongoing future of work debate, the pendulum is swinging back to hybrid work as CEO expectations for a full return to office decline.

When it comes to driving growth, CEOs are still interested in transformative M&A. But the majority say their organizations will wait until later this year or 2025 to seriously pursue new deal making.

In this era of compound volatility, it’s clear that many CEOs are anticipating and outpacing the resulting risks by living their values, acting with purpose and pairing long-term investments with a focus on GenAI and the agility it can create for an organization to take advantage of new opportunities and overcome challenges.

| Paul Knopp |

Download the report

KPMG 2024 U.S. CEO Outlook Pulse Survey

Economic Outlook & Business Environment: CEOs remain confident in the growth prospects of the U.S. economy but are making strategic adjustments to address a combination of near-term risks and structural changes.

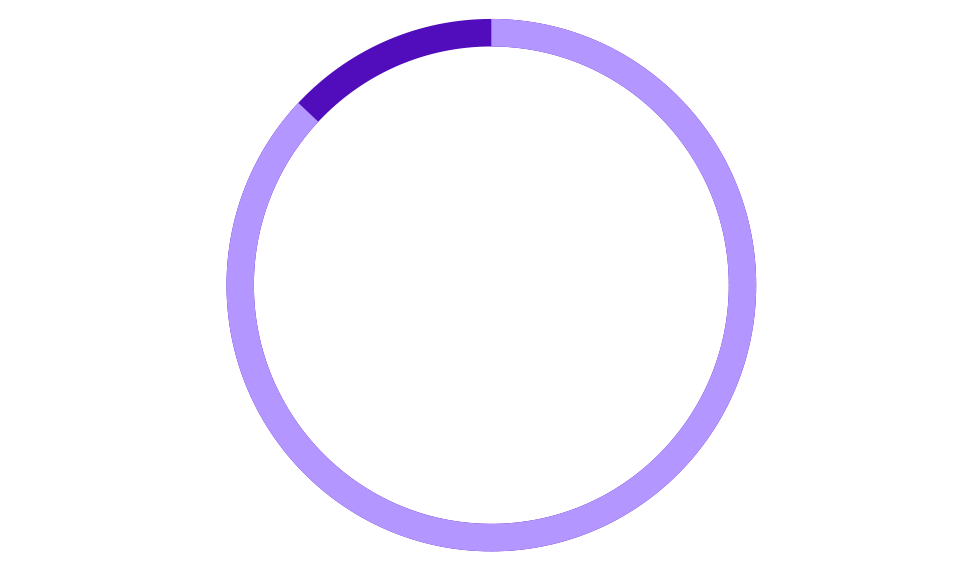

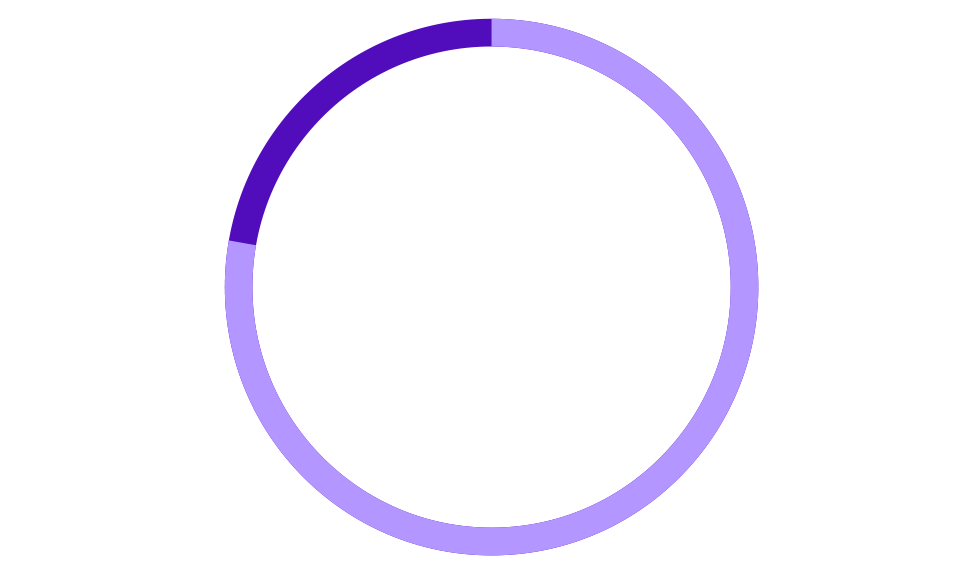

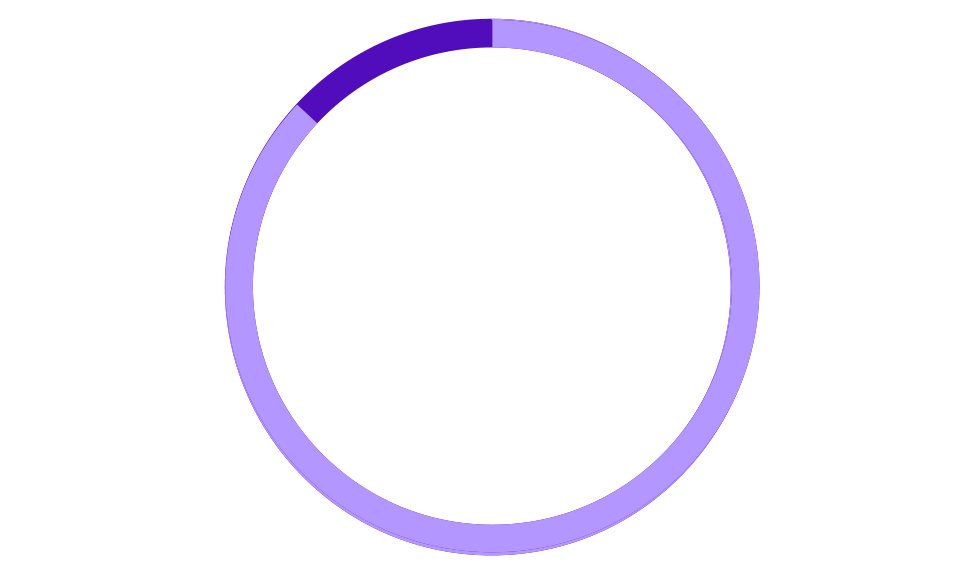

CEO confidence in economy and company growth prospects

87%

are confident in the growth prospects of the U.S. economy

78%

are confident in the growth prospects of the global economy

78%

are confident in the growth prospects of their companies

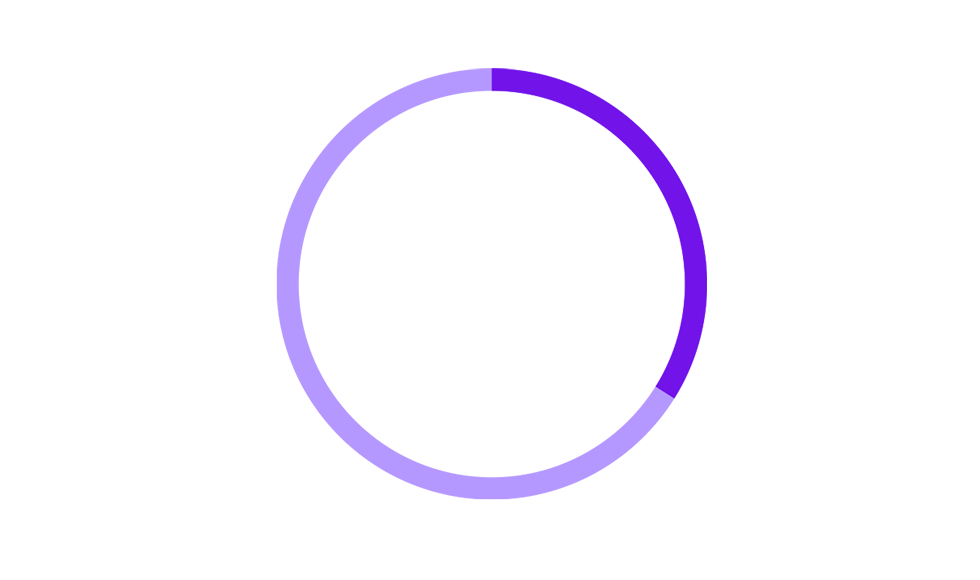

Geopolitics: CEOs actively making strategic adjustments

67%

are currently making significant strategic adjustments in response to geopolitical uncertainty, wars, conflicts and major elections happening around the world

When asked to identify the risks posing the greatest threat to their organization’s growth over the next year, CEOs cited regulatory concerns, operational issues, cyber security and tax.

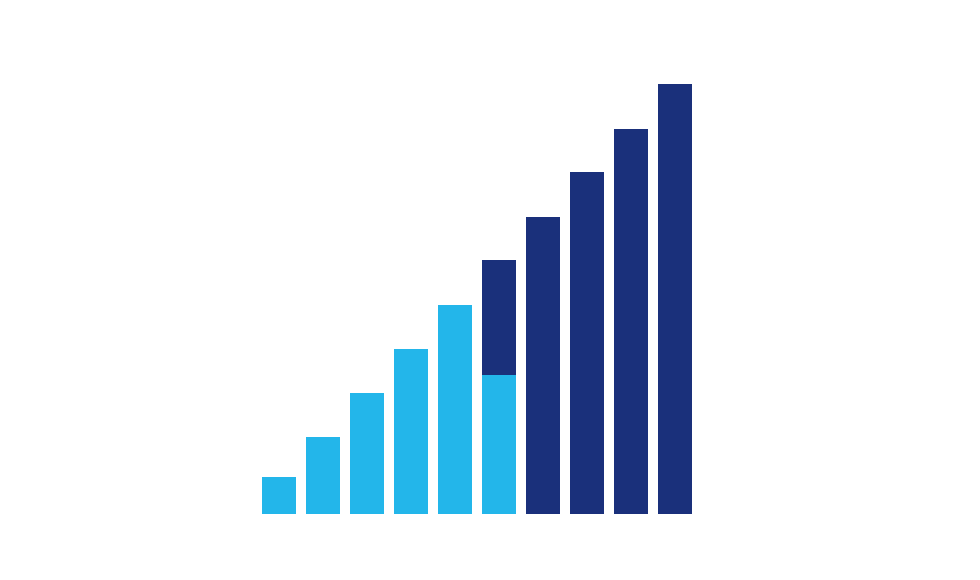

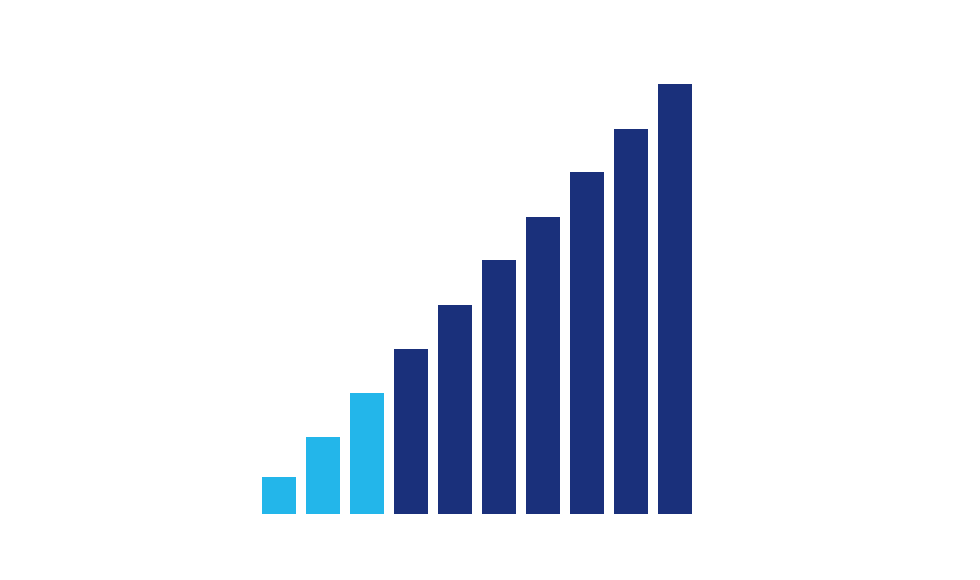

Generative AI: CEOs see GenAI as central to gaining a competitive advantage and are working to rapidly advance deployment of the technology across their enterprises in a responsible way.

Many CEOs plan to increase GenAI investments over next year

41%

plan to increase their investment in GenAI next year

56%

anticipate their overall investment in GenAI will stay flat

CEOs rapidly advancing GenAI deployment in next 12-18 months

39%

are scaling - moving from pilots to industrialization across multiple functions or business units

29%

are focusing on discrete use cases in specific functions or teams

15%

are broadening adoption of GenAI tools across their workforce with the training and skill building needed to do so

CEOs report their organizations already have a number of initiatives in place to promote responsible use of AI, including ongoing education and training (95%), regular audits and monitoring (82%), human oversight (71%) and collaboration and regulatory adherence (67%).

In 2024, CEOs plan to implement the use of watermarks or disclosures of AI use (81% vs. 19% today – the most significant jump), data privacy measures (63%), ethical frameworks (49%) and third-party reviews (47%).

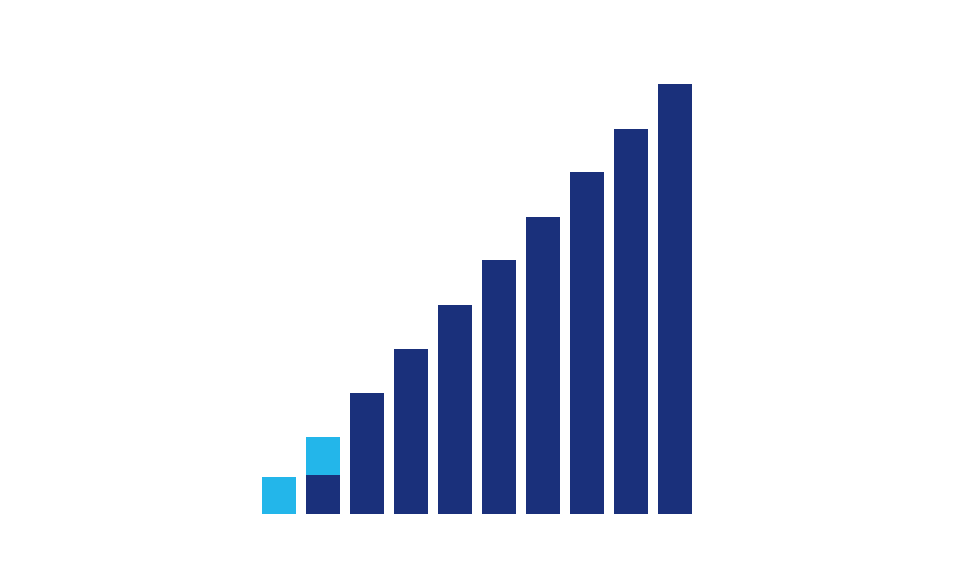

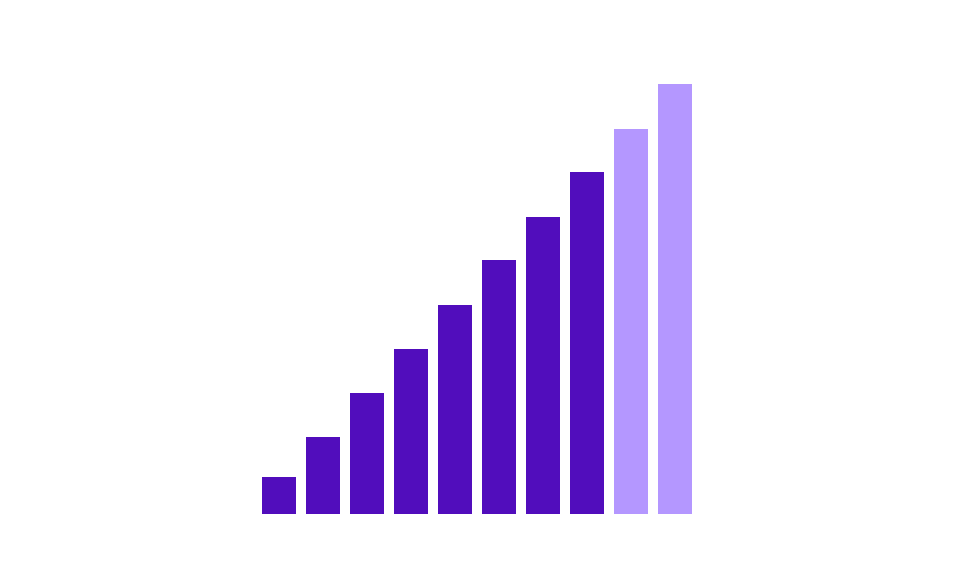

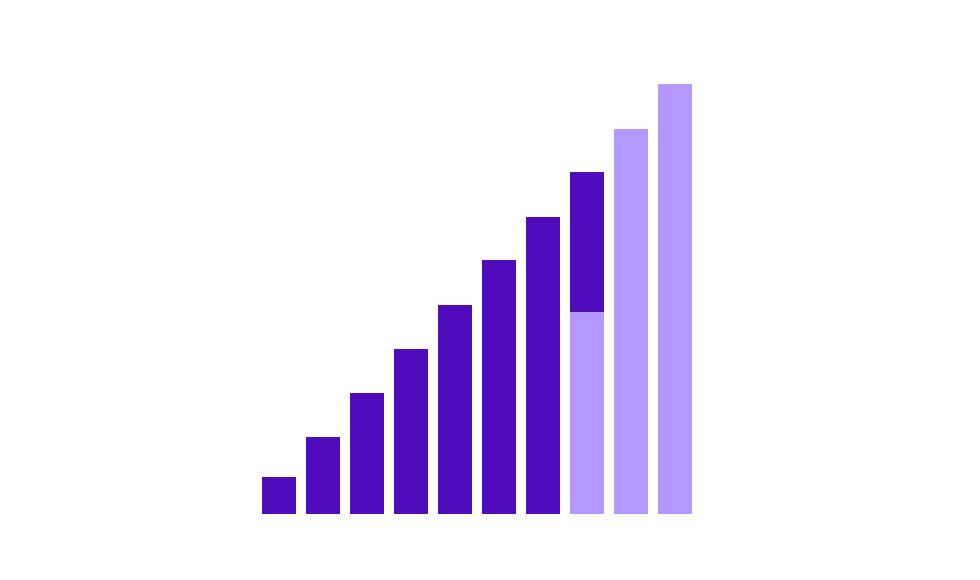

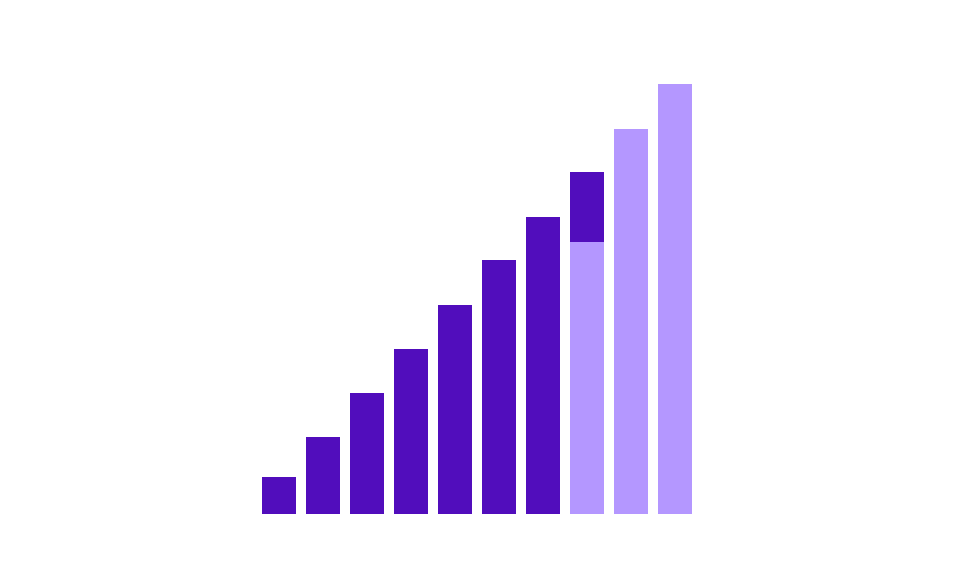

Mergers & Acquisitions: CEOs are waiting for the opportune moment to pursue M&A activity - most likely later this year or in 2025.

CEO deal-making activity timeline

48%

of CEOs say their organization will wait until 2025 to seriously pursue new deal making

34%

say they are waiting until the second half of 2024.

Talent & Culture: CEOs are proactively managing a tight labor market and focusing on initiatives to promote mental well-being and prevent burnout as acceptance of hybrid work models grows.

Solving for a tight labor market

78%

of U.S. CEOs are prioritizing upskilling current employees

69%

are leveraging GenAI when it comes to filling any gaps in their organization’s talent base

70%

of CEOs said their company will be dropping or have already dropped college degree requirements for certain jobs

Future of work debate - pendulum swings back to hybrid work

34% of CEOs envision the working environment for corporate employees whose roles were traditionally based in-office to be back in the physical workplace in the next three years – a notable decrease from 2023 (62%).

46% envision these roles to be hybrid (34% in 2023) and only 3% envision them being fully remote (4% in 2023).

Ethical culture drives growth

88% say their organization's financial success, including profitability and growth, depends on their company having a strong ethical culture.

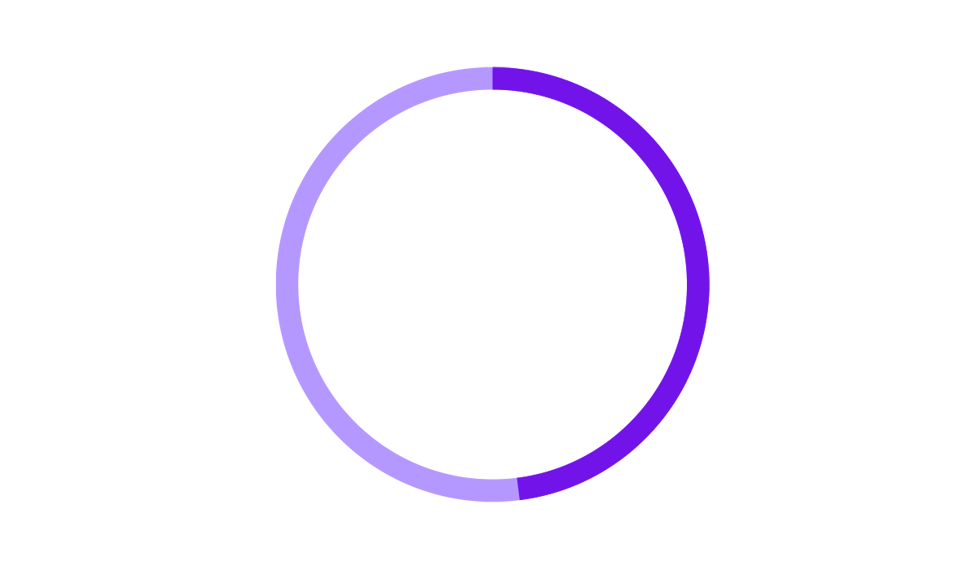

Sustainability Initiatives / ESG: The execution of ESG initiatives edged out other areas as CEOs' top operational priority. The majority expect to see significant returns from their sustainability investments in three to five years.

CEOs' top operational priority over the next year

17%

Execution of ESG initiatives

14%

Prioritize inflation proofing capital and input costs

11%

Advancing digitization and connectivity across the business

11%

Improving supply chain agility and resilience

11%

Improving the customer experience

Rate of return for sustainability investments

55%

of CEOs expect to see significant returns from their sustainability investments in the next three-to-five years

25%

are predicting five to-seven years

19%

are predicting one to three years.

About KPMG’s CEO Outlook Pulse Survey

The KPMG U.S. CEO Outlook Pulse Survey encompassed 100 CEOs from large companies. All respondents have annual revenues over U.S.$500 million and more than one-third of the companies surveyed have more than U.S.$10 billion in annual revenue. The survey was conducted between February 21 and March 14.

About KPMG LLP

KPMG LLP is the U.S. firm of the KPMG global organization of independent professional services firms providing audit, tax and advisory services. The KPMG global organization operates in 143 countries and territories and has more than 273,000 people working in member firms around the world. Each KPMG firm is a legally distinct and separate entity and describes itself as such. KPMG International Limited is a private English company limited by guarantee. KPMG International Limited and its related entities do not provide services to clients.

KPMG is widely recognized for being a great place to work and build a career. Our people share a sense of purpose in the work we do, and a strong commitment to community service, inclusion and diversity and eradicating childhood illiteracy. Learn more at www.kpmg.com/us.