An analysis of ESG metrics published by institutional real estate investors in fiscal year 2022 reveals where the industry stands, what makes comparisons so difficult, and why the net-zero goal is at risk of failing due to misaligned incentives in ESG performance measurement.

Varying levels of ESG reporting across the institutional investor universe

The analysis of nearly 150 annual or sustainability reports of institutional real estate investors shows the significant impact of investor pressure on sustainability reporting.

While well over 80% of the real estate funds and real estate companies surveyed disclose metrics on energy intensity and greenhouse gas emissions intensity, only a quarter (energy intensity) and just under half (greenhouse gas emissions intensity) of the pension funds surveyed do so. However, almost three out of four investment foundations publish these environmental indicators.

Circulars 04/2022 and 06/2023 of the Asset Management Association Switzerland (AMAS) have set binding minimum standards for real estate funds as part of voluntary self-regulation. However, the self-regulation cannot be recognized as a minimum standard by FINMA due to the applicable legal provisions. The Conference of Managing Directors of Investment Foundations (KGAST) has decided to follow the environmental indicators developed by AMAS to ensure uniformity and comparability.

Although reporting on environmental indicators is not mandatory for investment foundations, the high number of publications shows that investor pressure is having an effect.

The same can be said for real estate companies and pension funds. Listed companies are under scrutiny from investors who not only want but also expect comprehensive ESG reporting. In contrast, the pressure on pension funds is significantly lower: the ESG reporting standard for pension funds published by the Swiss Pension Fund Association (ASIP) in December 2022 is only recommendatory in nature.

Although reporting on environmental indicators is not mandatory for investment foundations, the high number of publications shows that investor pressure is having an effect.

Comparability is not a priority

From a comparability perspective, it is unfortunate that ASIP chose not to explicitly follow the environmental metrics defined by AMAS and its guidelines for data collection. Even though the collection of AMAS KPIs already leaves considerable room for discretion, making comparisons difficult in practice, a uniform approach to harmonizing the collection of environmentally relevant data in the future would have been desirable.

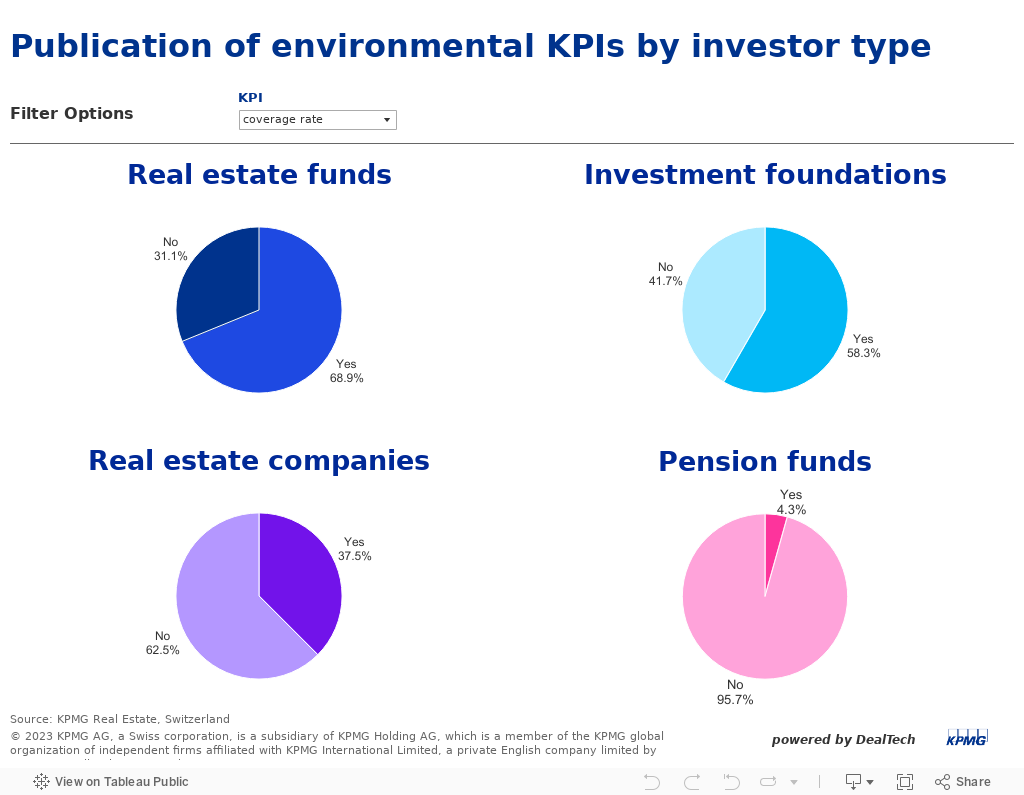

However, there does not seem to be much emphasis on transparency at present, as evidenced by the published figures on coverage rates of collected energy consumption data. While almost 70% of real estate funds disclose the coverage rate (mandatory starting from fiscal year 2024), the corresponding percentage in reporting drops rapidly for investment foundations (58%) and real estate companies (37%). Among pension funds, only 4% publish this ratio.

Comparison of environmental indicators published in fiscal year 2022

The overall comparison of residential portfolios shows that the energy intensity threshold is met on average, even if only narrowly in the case of real estate funds. However, the analysis of greenhouse gas emission intensity shows a different picture: both real estate funds and investment foundations with residential portfolios exceed the threshold of 20.2 kg CO2e/m2 p.a. Residential portfolios of investment foundations show an average excess of approx. 4%, while the gap for residential real estate funds almost reaches 10%. It should be noted that residential portfolios may also contain small shares of commercial real estate.

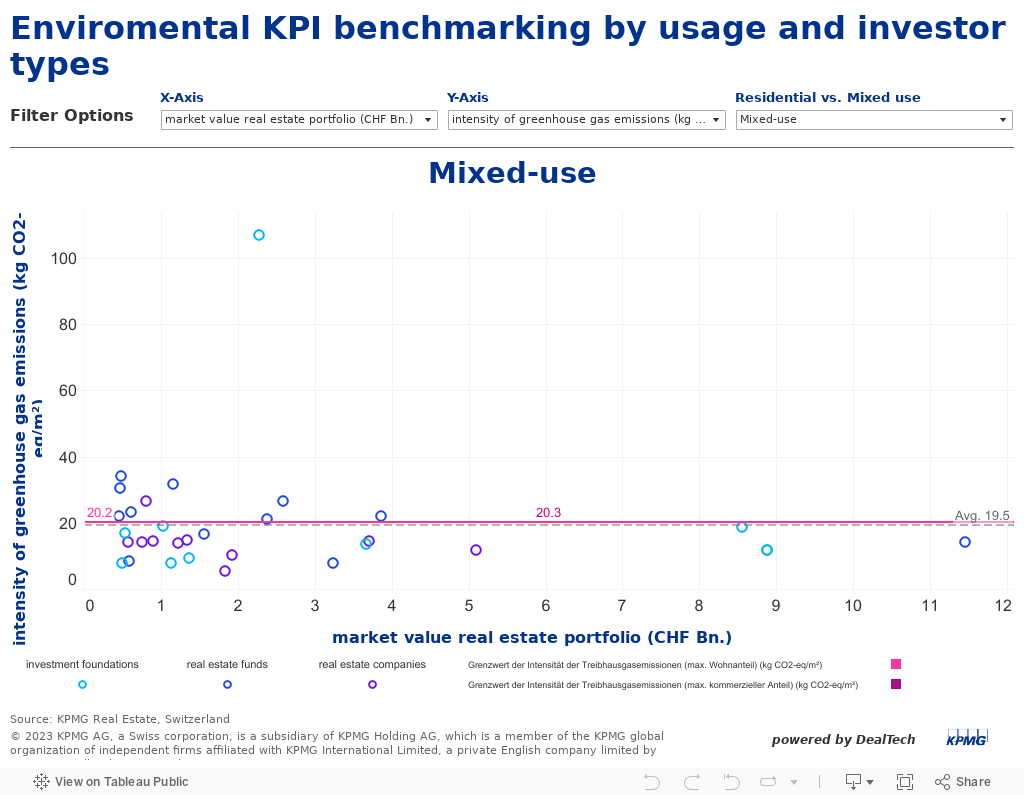

The analysis of mixed-use portfolios is subject to greater uncertainty, as the exact composition of the portfolios is not known. We predominantly assumed office and retail uses next to a primary residential component, and a corresponding threshold range was modeled.

The energy intensity of all direct real estate investments considered (real estate funds, investment foundations and real estate companies) with mixed-use portfolios is, on average, well below the thresholds in some cases. The intensity of greenhouse gas emissions, on the other hand, exceeds the thresholds by more than 10% on average, except for real estate companies.

Overall, significant differences between the highest and lowest intensity ratios can be observed, regardless of use.

Fossil heating meets energy efficiency?

How should these findings be interpreted? Is Switzerland characterized by generally energy-efficient buildings that are still too often heated with fossil fuels?

The consistently better performance of the portfolios considered in terms of the ESG indicator energy intensity compared to greenhouse gas emission intensity suggests that this is the case.

According to data from the Swiss Federal Statistical Office, almost 60% of all residential buildings were still heated with fossil fuels in 2022, although the share of buildings heated with heat pumps has increased significantly to almost 20%.

Limited comparability

It is important to emphasize that these comparisons completely disregard how "old" the respective real estate portfolios are and what investments are planned for future ESG measures. Unlike the as-is environmental metrics, most of this information is not publicly available or is only partially available.

This information would be critical for a holistic comparison. An older building portfolio would indicate that the cost of implementing sustainable measures is higher than for newer properties.

In addition, real estate funds tend to have smaller assets on average than investment foundations and real estate companies. Therefore, reducing the carbon footprint at the level of the overall portfolio is more difficult and time-consuming.

Wrong incentives in ESG performance measurement

Should we congratulate investment foundations for their overall better performance and put real estate funds on notice? Such a categorical conclusion would not be reasonable, despite the better performance of investment foundations on published environmental metrics. What is important is to look at year-to-year comparisons to track progress and a consideration of the total existing building stock.

Should investors be applauded for making their lives easier by acquiring only new properties that already meet sustainability criteria? While this approach may provide good ESG KPIs, it does not help the building stock (and therefore the climate). Investing in the existing stock is just as important.

Focusing on current energy and environmental metrics without a portfolio context (age of properties, total planned investment volume for ESG measures) contributes to older existing properties being relatively unattractive to institutional investors.

There is a risk of misaligned incentives if (short-term) ESG performance takes precedence, which could jeopardize long-term climate goals.

There is a risk of misaligned incentives if (short-term) ESG performance takes precedence, which could jeopardize long-term climate goals.

A more comprehensive approach to measuring sustainability performance, including baseline data on existing properties, current performance and planned actions is desirable and necessary to ensure comparability and to not discourage investment in currently unsustainable properties.

It is worth noting that the current focus on emissions during property operation excludes the concept of embodied carbon. Whether the greater energy efficiency of new buildings compared to renovated existing buildings offsets the newly created embodied energy over the life cycle is difficult to determine due to a lack of data, but certainly debatable.

Net-zero target unattainable if existing buildings are neglected

A common pitfall is to forget that the entire real estate stock is taken into account when calculating annual energy consumption and emission thresholds. The reduction path is not static but reflects the total remaining emissions budget to meet the goals of the Paris Climate Agreement.

Exceeding the limits today leads to a steeper reduction path tomorrow, i.e. to lower thresholds.

Long-term climate goals will be unattainable if currently unsustainable buildings are treated as pariah. In other words, today’s selfishness undermines tomorrow's goals.

Exceeding the limits today leads to a steeper reduction path tomorrow, i.e. to lower thresholds.

Annual monitoring of ESG key performance indicators

For the first time, the published key performance indicators of a large number of institutional real estate investors are collected and aggregated in this analysis. The challenges of comparing these absolute figures become apparent, and it must be noted that the data basis for a comprehensive assessment of sustainability performance is still inadequate.

An ongoing comparison of published energy and emissions data in the coming years is expected to provide better insight into sustainability performance.

Scope and methodology of the analysis

Scope

The analysis covers 61 real estate funds, 48 investment foundations, 16 real estate companies and 23 pension funds. The information on energy intensity, greenhouse gas emission intensity and coverage ratio were taken from the respective annual reports for the year 2022.

Classification

The classification of the portfolios into residential, mixed and commercial use was made on the basis of the available information in the respective annual reports and in accordance with the definitions of Art. 86 of the Swiss Financial Market Supervisory Authority (FINMA). The usage breakdown of the portfolios under review is as follows: approximately 37% residential, approximately 40% mixed, approximately 23% commercial.

Thresholds for energy intensity and greenhouse gas emissions

The basis for the 2022 thresholds was taken from the Carbon Risk Real Estate Monitor (CRREM) decarbonization tool (V2.03) for Switzerland, considering the net zero target of the Paris Climate Agreement for the respective uses. For mixed-use portfolios, a mix of residential, office and retail use and a corresponding range of thresholds based on the proportion of residential use was assumed. A general analysis of commercial portfolios was not conducted, as it is likely to be of little value due to the heterogeneity of portfolios and the wide variation in thresholds for different commercial uses (office, retail, industrial, hotel, logistics).

All analyses were performed at the portfolio level based on publicly available information in the annual reports.

Contact our experts for more information