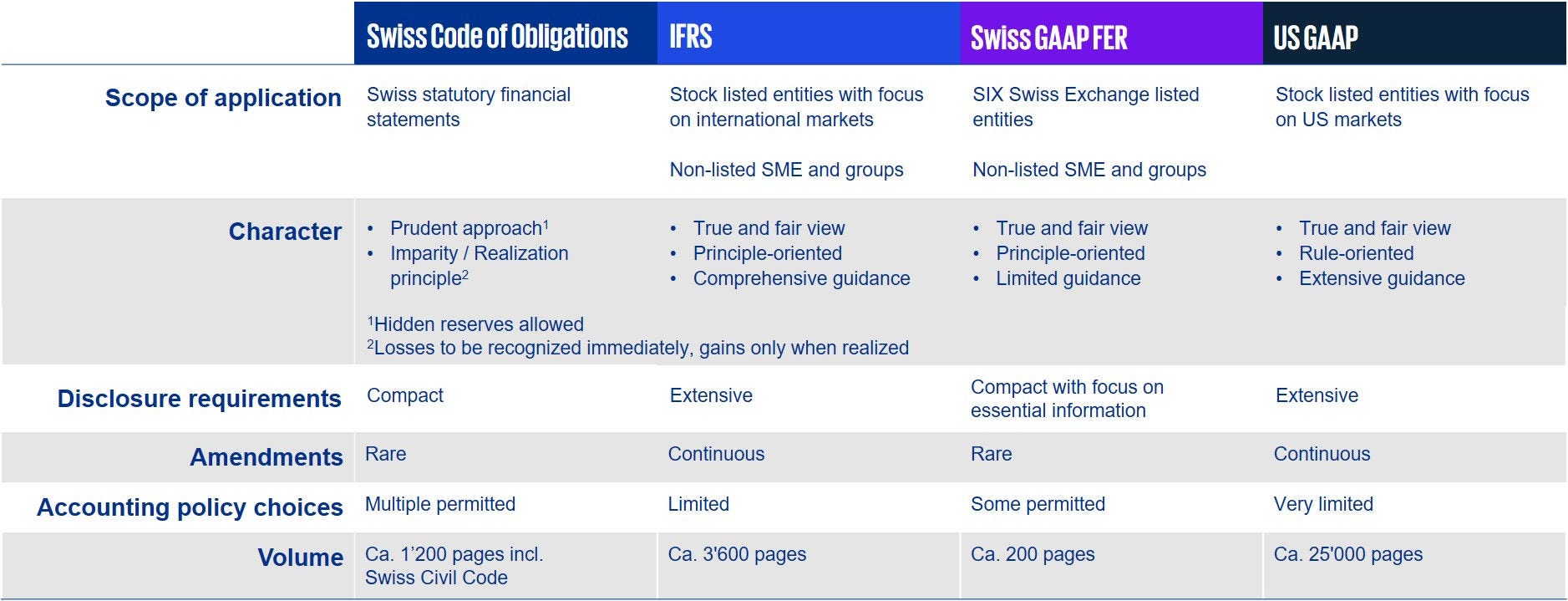

The requirements of the Swiss Code of Obligation do not provide for a fair presentation as a common practice due to its interpretation of the principle of prudence and its orientation towards creditor protection.

For companies aspiring to greater transparency in their financial reports or pursuing a listing on the SIX Swiss Exchange, other stock exchange or for an exit of investors, a financial statement conversion becomes thus inevitable.

Consequently, those corporations must contemplate which accounting and valuation principles they want to apply along with the level of transparency they intend to provide to the readers of their financial statements.

Currently, nearly half of the companies listed on the SIX Swiss Exchange publish IFRS-compliant consolidated financial statements. Comparatively, Swiss GAAP FER is in use by another third of the listed companies. The remaining companies apply US GAAP or special legal regulations (e.g. banks).