22 May 2024

Global minimum tax: different strategies in the cantons

Cantons embrace different strategies to lessen impact of global minimum tax

- The introduction of the global minimum tax in Switzerland has already prompted a few cantons to revise their tax laws in an effort to remain attractive for businesses going forward.

- The restrictions on international tax competition offer incentives for more subsidies and other measures.

- The ordinary corporate tax rates for businesses in Switzerland remained stable compared to the previous year at an average of 14.6%.

- The tax rates levied for high-income private individuals in Switzerland fell from 33.5 to 32.7 percent year over year. The Canton of Schwyz has pulled ahead of Zug, which had previously topped the list.

- Only 10% of all taxpayers contribute almost 80% to direct federal tax. More than half of the tax revenue is paid by 1% of the highest earners, as the latest federal tax statistics show.

Working on the constitutional basis established through the popular referendum held on 18 June 2023, the Federal Council enacted the global minimum tax as a national top-up tax that entered into force on 1 January 2024. As part of the new tax regime, several cantons have already made changes to their tax rates or launched projects aimed at improving their attractiveness as a location. Some cantons, for example, already responded prior to the (foreseeable) introduction of the minimum tax by increasing their local tax burden.

Different strategies in the canton

As shown in the examples that follow, the tax policies initially in place in the various cantons are prompting them to embrace different approaches, especially with regard to the 15 percent global minimum tax rate.

The Canton of Schaffhausen, which had applied a corporate tax rate of less than 13.8 percent in 2023, introduced a progressive corporate tax rate from 2024 onward. Profits of between CHF 5 million and CHF 15 million and profits in excess of CHF 15 million are taxed at a higher rate. As a result, profits that are higher than around CHF 15 million will be subject to an effective tax rate (incl. federal taxes) of 15 percent from 2024 onward. The previous tax rate, which will be reduced as planned from 2025 onward, will continue to apply for profits of less than CHF 5 million.

The Canton of Geneva raised its effective corporate tax rate (including federal taxes) from 14 percent to 14.7 percent and eliminated the municipal business tax in exchange. The advantage of this approach is that, unlike the business tax, the tax expenses incurred now also qualify as eligible taxes. Since the effective corporate tax rate in Geneva is still lower than the minimum rate of 15 percent, this change is likely to reduce the top-up tax.

A somewhat different trend is being observed in the Canton of Zurich. Given that the effective corporate tax rate in Zurich is already higher than the minimum rate of 15 percent, it has no incentive to raise the tax burden. On the contrary, the government council of the Canton of Zurich intends to cut its cantonal corporate tax rate from 7 percent to 6 percent. This is not directly connected to the introduction of the minimum tax rate, however, but had already been announced at an earlier date in connection with the Federal Act on Tax Reform and AHV Financing (TRAF).

Subsidy-based competition will intensify

With the global minimum tax limiting their leeway regarding corporate tax rates, countries are working on finding a way to offset these through measures such as tax credits and subsidies. Under the international regulations regarding the global minimum tax, subsidies or qualifying/recognized tax credits are treated more favorably than tax breaks. International developments like the European Green Deal, the Inflation Reduction Act in the US and the Foreign Subsidies Regulation that was introduced in the EU in 2023 show that the importance of industrial policies and subsidies will grow in the context of location competition.

This development is also becoming apparent in Switzerland. According to the Swiss Federal Tax Administration, slightly more than half of the cantons are evaluating – or have already evaluated – subsidy-like instruments for companies (as of August 2023). Only a few cantons have announced specific measures, in particular:

In January 2024, the Canton of Grisons submitted a draft bill for consultation that seeks to reward companies whose activities (i) increase added value created within the canton, (ii) strengthen research, development and innovation or (iii) improve environmental sustainability.

The Canton of Zug announced its intention to support companies directly through a system of subsidies with extensive delegation powers afforded to the government council.

“Implementing specific projects to introduce tax credits or comparable subsidies makes sense, especially in cantons with an effective tax rate of less than 15 percent. In cantons with a higher tax burden, the situation is less urgent,” says Stefan Kuhn, Head of Tax and Legal at KPMG Switzerland. He points out, however, that reclassifying tax incentives as government subsidies results in higher, often irreversible government spending.

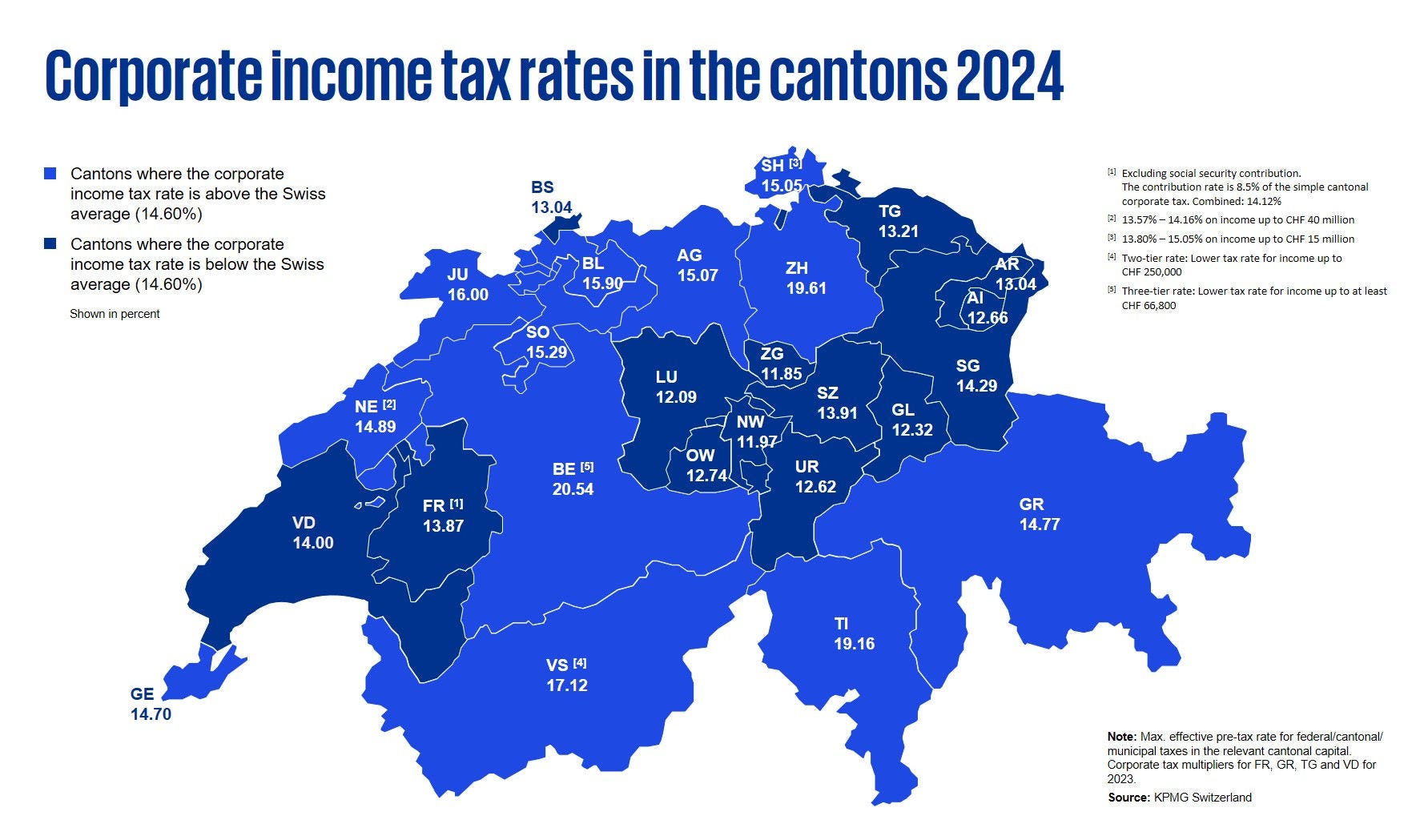

Swiss Tax Report 2024: No significant changes in the cantonal corporate tax rate comparison

The ordinary corporate tax rates for businesses in Switzerland remained stable compared to the previous year at an average of 14.6%. Changes in corporate tax rates were only seen in eight cantons. Those are some of the findings presented in KPMG’s Swiss Tax Report 2024, which compares corporate and income tax rates from more than 50 countries and all 26 Swiss cantons.

The biggest cuts were made by the cantons of Aargau (-1.19 percentage points) and Bern (-0.5 percentage points), while Schaffhausen and Geneva made the largest increases to their corporate tax rates (+1.25 and +0.7 percentage points).

The cantons of Zug, Nidwalden and Lucerne remain the most attractive in terms of their corporate tax rates, although their rates have converged a little compared to the previous year. The Canton of Zug still has the lowest tax rates and has raised its corporate tax rates somewhat (from 11.80 to 11.85 percent), while Lucerne made another slight reduction to its rates (from 12.15 to 12.09 percent), as it did in the previous year. The Canton of Nidwalden, which remains in second place, left its rate unchanged at 11.97 percent.

With a corporate tax rate of 20.54 percent, the Canton of Bern still ranks last in a cantonal comparison. A tax cut of 0.5 percentage points, however, helped it narrow the gap to the other cantons slightly.

Compared with other countries around the world, Switzerland’s taxes for companies are low – especially in the cantons of Central Switzerland. In Europe, only Guernsey (0.0 percent), Hungary (9.0 percent) and Bulgaria (10.0 percent) still offer even lower ordinary corporate tax rates. With a tax rate similar to Switzerland’s, Ireland (12.5 percent) remains the country’s most important competitor in Europe. Outside Europe, the Bahamas (0.0 percent), Bermuda (0.0 percent) and Bahrain (0.0 percent) stand out as low-tax domiciles. Hong Kong (16.5 percent) and Singapore (17.0 percent) also have attractive corporate tax rates. Large economies like the US (27.0 percent), China (25.0 percent), India (30.0 percent) and Brazil (34.0 percent) apply considerably higher tax rates than Switzerland.

Fig. 1: Overview of cantonal corporate tax rates for companies

Fig. 1: Overview of cantonal corporate tax rates for companies

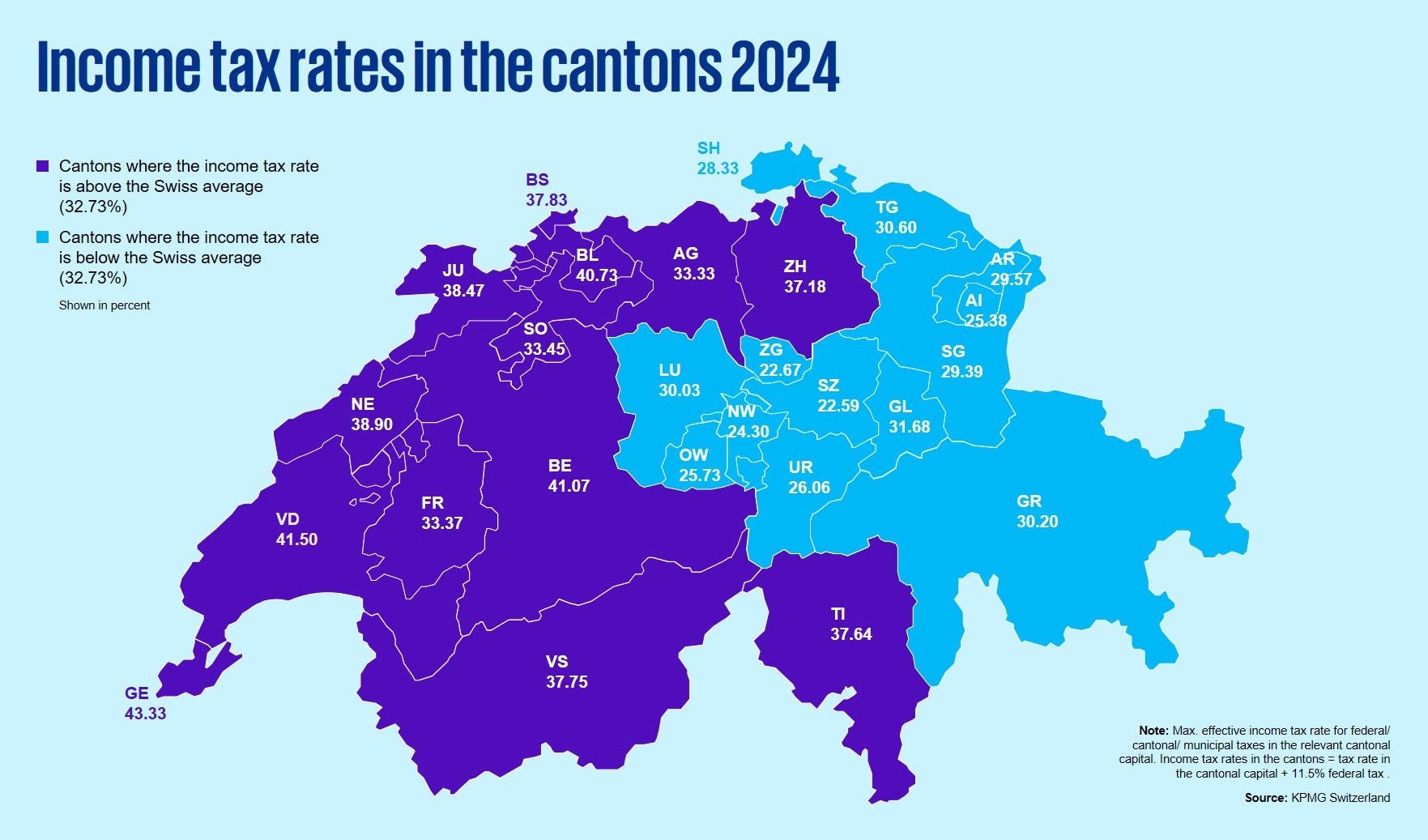

Income taxes: Schwyz pulls ahead of Zug

At 32.73 percent, the highest incomes in Switzerland are taxed at a slightly lower rate than in the previous year (33.45 percent). Some two-thirds of cantons have reduced their tax rates for top incomes, with the largest cuts seen in St. Gallen (-3.44 percentage points) and Basel-Stadt (-2.51 percentage points).

The Canton of Schwyz advanced to first place in the cantonal comparison thanks to its substantial reduction of 2.39 percentage points. With a peak tax rate of 22.59 percent, it is now slightly ahead of the cantons of Zug (22.67 percent) and Nidwalden (24.30 percent).

A few cantons have raised their tax rates for top incomes, such as Appenzell Innerrhoden (+1.56 percentage points) and Obwalden (+1.43 percentage points).

The cantons of Western Switzerland are still ranked lowest, especially Geneva (43.33 percent) and Vaud (41.5 percent), followed by Bern (41.07 percent) and Basel-Landschaft (40.73 percent).

Fig. 2: Income tax rates of Swiss cantons at a glance

Fig. 2: Income tax rates of Swiss cantons at a glance

For more information and the detailed study, please go to: www.kpmg.ch/swisstaxes