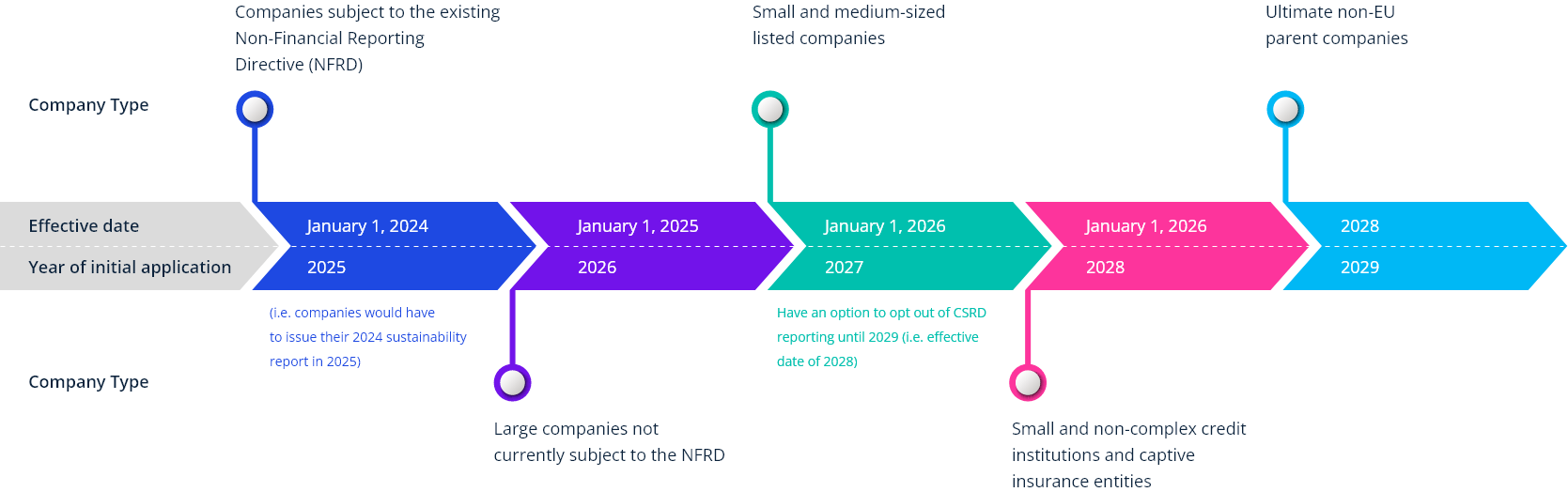

The EU’s Corporate Sustainability Reporting Directive (CSRD) – formally adopted by the European Council on 28 November 2022 – is transforming ESG reporting.

Starting from 2024, almost 50,000 companies are subject to mandatory sustainability reporting, including non-EU companies which have subsidiaries operating within the EU or are listed on EU regulated markets.

In January 2025, the Commission of the European Union published a ‘Compass for Competitiveness’ (EU Compass) to regain competitiveness and secure sustainable prosperity. In the Competitiveness Compass, the Commission stated that the first of a series of Simplification Omnibus packages will cover far-reaching simplification in the fields of sustainability reporting, sustainability due diligence and taxonomy.

On 26 February 2025, the Commission published its proposal for the first Omnibus package concerning amendments to the EU Accounting Directive (Directive 2013/34/EU), the EU Statutory Audit Directive (Directive 2006/43/EC), the CSRD (Directive (EU) 2022/2464), and the CSDDD (Directive (EU) 2024/1760).