Softer increases in starting pay...

September survey data pointed to a further easing of overall pay growth across the UK. Though sharp, the rate of starting salary inflation edged down to a two-and-a-half-year low, while temp wages increased at the slowest rate in 31 months. While competition for skilled workers and the higher cost of living continued to place upward pressure on pay, there were some reports of greater strain on clients' budgets.

...amid further improvement in candidate availability

The overall availability of candidates improved again in September. Although the pace of expansion softened further from July's recent high, both permanent and temporary labour supply increased at historically strong rates. Anecdotal evidence generally linked the latest upturn to redundancies and a slowdown in market conditions.

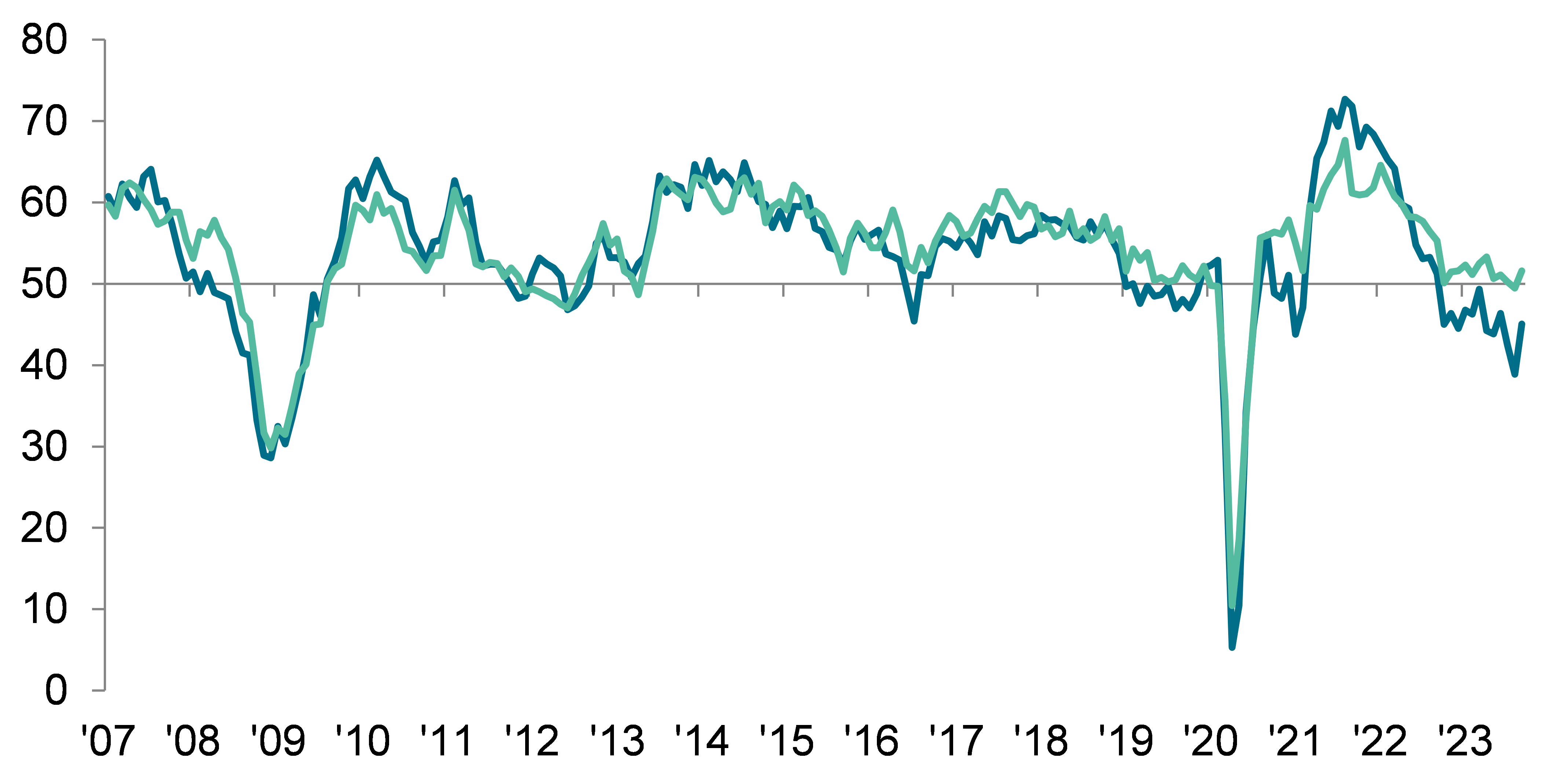

Overall vacancies fall slightly in September

Total vacancies slipped into contraction territory in September, marking the first fall in overall demand for staff since February 2021. The rate of contraction was only marginal, however. Underlying data revealed a fresh reduction in permanent vacancies, albeit one that was slight, while growth of demand for temp staff moderated to a four-month low.

Regional and Sector Variations

All four monitored English regions recorded declines in permanent placements, though in all cases rates of contraction slowed from August.

Temp billings increased in all four monitored English areas bar the South of England during September. The quickest expansion was recorded in the capital.

Demand for permanent staff fell across both the private and public sectors during September, with the latter noting by far the steeper rate of decline. Divergent trends were meanwhile seen for temporary vacancies. In the private sector, demand for short-term staff rose at a softer, but still solid pace, but decreased across the public sector.

Permanent staff vacancies increased in five of the ten broad employment categories during September, led by Hotel & Catering. The steepest reductions in permanent labour demand were meanwhile seen in the Retail and Construction sectors.

Demand for temp staff rose in five of the ten employment sectors covered by the survey. Nursing/Medical/Care registered the strongest rise in vacancies overall. Sharp deteriorations in demand were meanwhile signalled for Retail and Executive/Professional workers.

Comments

Commenting on the latest survey results, Claire Warnes, Partner, Skills and Productivity at KPMG UK, said:

“A concerning feature of this month’s data is that demand for staff is losing momentum, with total vacancies falling for the first time since February 2021 amid a fresh reduction in permanent vacancies. While both reductions are slight, employers are clearly nervous due to the long-term economic uncertainty and budget constraints that are impacting businesses everywhere. This in turn is leading to a continued reliance on temporary staff.

“For several months, strong pay growth has been a consequence of a tight labour market. But strains on employers’ budgets are now affecting the rate of starting salary inflation which is at a two-and-a-half-year low, while temporary wages increased at the slowest rate in 31 months.

“Skill shortages across a range of sectors – from permanent IT staff to temporary nursing roles – also continue to be an area of long-term concern for the economy.

“The labour market is starting to look slightly precarious again and recruiters will be wondering and hoping that the recent slight calming of inflation rates positively impacts the outlook for both employers and jobseekers.”

Neil Carberry, REC Chief Executive, said:

“Employers tell us they are feeling better about themselves as the year moves on, and today’s data does suggest the possibility of a turnaround in hiring over the next few months. Permanent placements have been falling for a year now from abnormal post-pandemic highs. While permanent hiring activity continues to slow, fewer firms reported a slowdown last month, leading to a much shallower rate of decline than most months recently. Likewise, temporary hiring remains robust with billings growing marginally in September – as they have most months this year.

“This feels like a market that is finding the bottom of a year-long slowdown. And the relative buoyancy of the private sector is likely to be driving this more positive outlook – while vacancies are now dropping they remain robust in the private sector by comparison to the public. Some sectors such as hospitality, engineering, logistics and healthcare continue to experience very strong and growing demand. Along with high inflation, this is likely to be contributing to the growth of pay for temps and perms alike.

“As we move towards the Autumn Statement, action to help people find high quality roles is essential as the picture varies so widely from sector to sector. The REC would like to see a focus on skills, finally reforming the system to deliver a mix of high-quality courses within the levy framework, and action to tackle inactivity – like extending the Restart programme which has helped recruiters place thousands of long-term unemployed people into work. Both of these could form part of a long-overdue people and growth strategy. From reforming government procurement to better and more effective regulation, there is a lot government could do in partnership with recruiters to drive growth and prosperity.”