Stablecoins are cryptoassets that are pegged against another asset – e.g. a fiat currency, such as the US dollar. They are often used as digital cash for cross-border payments and remittance, and for buying and selling other cryptoassets.

Like all types of cryptoassets, the rights and obligations vary between stablecoins. To determine the appropriate accounting, companies need to:

- identify their rights and obligations attached to the stablecoin;

- assess the main purpose of holding or transacting in the stablecoin; and

- apply judgement in identifying the relevant accounting standard and developing an accounting policy.

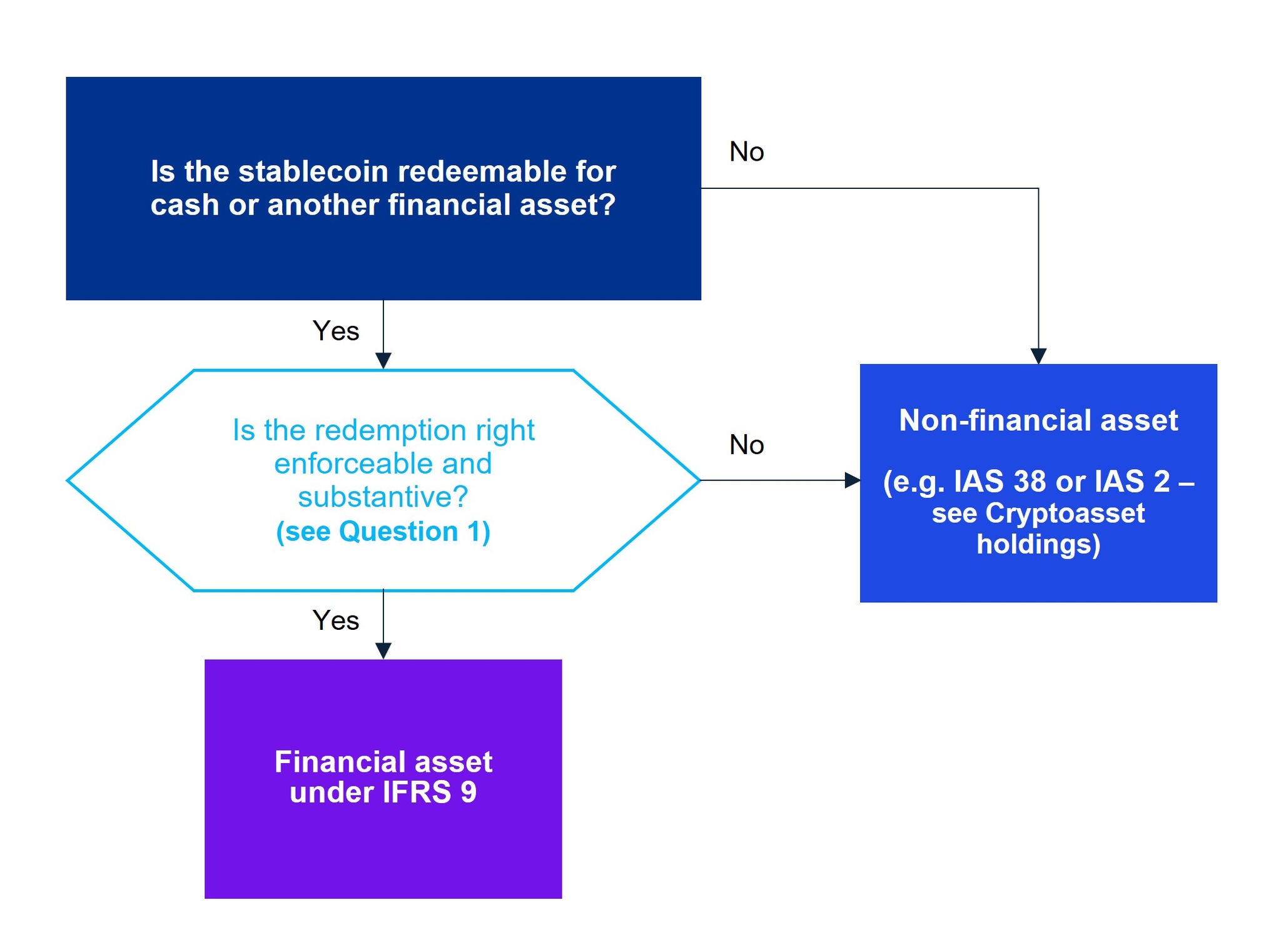

Stablecoins may also include redemption rights. These rights allow the holder to redeem the stablecoin from the issuer for an amount equivalent to the asset to which the stablecoin is pegged. For example, for a stablecoin pegged to the US dollar, a holder may request an equivalent amount in US dollars.

When a stablecoin includes a redemption right, a key question for the holder is whether the stablecoin is a financial asset in the scope of IFRS 9 Financial Instruments. The following diagram can help with this assessment.

Your questions answered

No.

In determining the accounting for a stablecoin, it is important to consider the underlying rights and obligations and whether these are substantive and enforceable.

Careful analysis is required to determine whether the holder has the contractual right to redeem the stablecoin for cash, including evaluating whether contractual restrictions over redemption, or any discretion of the issuer to avoid redemption, prevent the stablecoin from meeting the definition of a financial asset. If a stablecoin does not meet the definition of a financial asset, then it may be in the scope of IAS 38 Intangible Assets or IAS 2 Inventories.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.