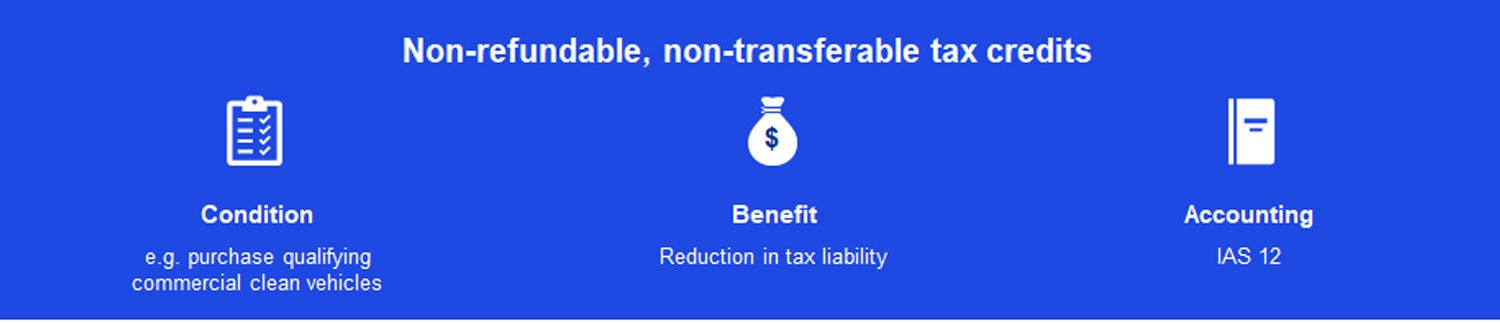

Typically, companies use non-refundable, non-transferable tax credits to reduce the tax liability and can realise their benefits only if they have sufficient taxable income.

Your questions answered

In our view, these tax credits are akin to tax allowances and therefore it is generally appropriate to account for them applying IAS 12 Income Taxes by analogy1. Although the amount of the tax credits received is independent of a company’s taxable profit, the economic benefit a company can realise by using these tax credits is limited to its income tax liability – i.e. a company needs to have sufficient taxable income to offset the tax credit amount.

Following IAS 12 by analogy, the tax credits are recognised and presented in the income statement as a deduction in current tax expense to the extent that a company is entitled to claim the credit in the current reporting period.

Any unused tax credit is recognised as a deferred tax asset (DTA) and income if it meets the DTA recognition criteria in IAS 12.

1 For detailed guidance on how to determine which accounting standard to apply, see Insights into IFRS® 3.13.700.10–720.20.

Answering your questions

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.