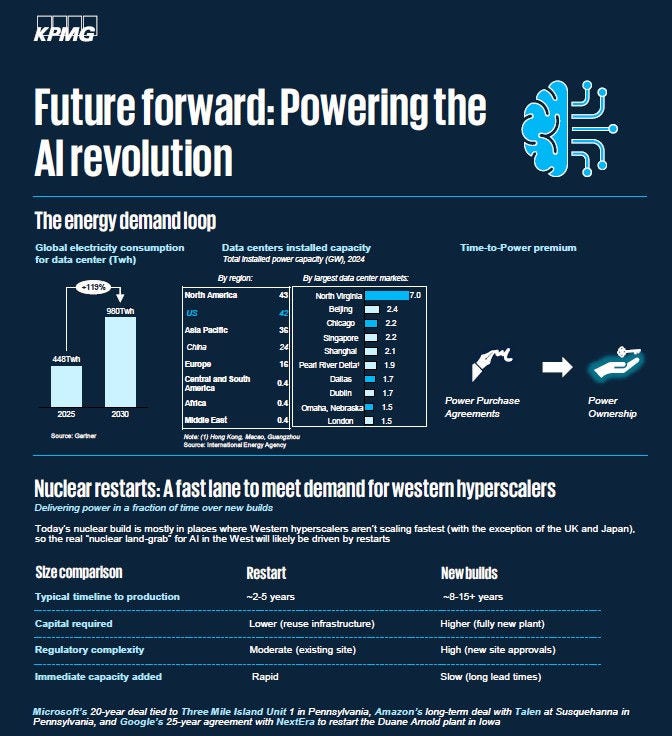

Today’s nuclear build is mostly in places where Western hyperscalers aren’t scaling fastest (with the exception of the UK and Japan, and pockets of India and Korea), so the real “nuclear land‑grab” for AI in the West will likely be largely driven by restarts.

Restarts can be materially faster than new construction. Teams refurbish turbines, generators, and control systems, reload fuel, complete safety and environmental reviews, and reconnect to the grid. This approach is often faster than greenfield development because the site, grid tie, and much of the plant already exist. Recent examples include Microsoft’s 20 year deal tied to Three Mile Island Unit 1 in Pennsylvania,3Amazon’s long term deal with Talen at Susquehanna in Pennsylvania,4 and Google’s 25 year agreement with NextEra to restart the Duane Arnold plant in Iowa.5

Countries that actively allow private nuclear investment will likely gain an edge. The United States, Canada, France, the United Kingdom, Sweden, and Japan have frameworks for private participation and for advanced projects such as small modular reactors (SMRs). These markets are already attracting hyperscale commitments and partnerships. By contrast, countries where nuclear is banned by law or constitution, such as Germany, Austria, Denmark and Ireland may need to reassess if they want a fair shot at hosting the largest AI campuses.