July 2026 update: The European Commission has now adopted the revised ESRS and the Voluntary sustainability reporting standard (VS) for smaller companies based on the VSME.

Highlights

Companies now have certainty on whether and how they will need to comply with the CSRD1 and CSDDD2, following the publication of agreed changes in the EU Official Journal.

These changes significantly reduce the number of companies required to report. They are part of the Omnibus initiative to reduce sustainability reporting and due diligence requirements for preparers while maintaining the spirit of the EU Green Deal.

The key changes to the CSRD are summarised below.

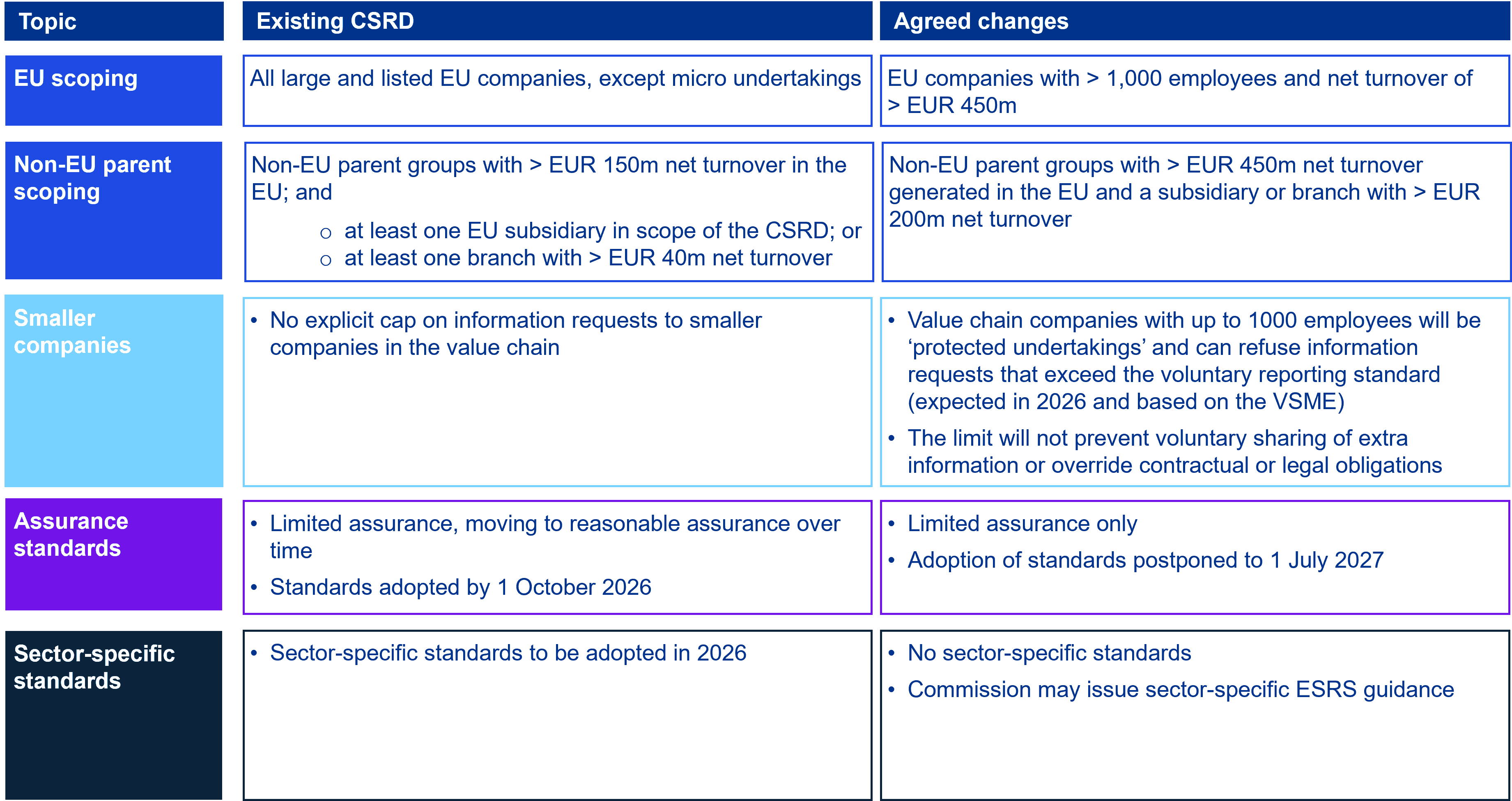

CSRD: Which companies remain in scope?

- EU companies with over EUR 450m net turnover and more than 1,000 employees will remain in scope of the CSRD. Wave one companies that fall out of scope may be exempted from reporting from as early as FY25, but these exemptions can only be provided by member states via national laws after the EU has adopted the changes.

- Financial holding companies3 will be exempt, but their subsidiaries or subgroups may still need to report if they meet the scoping threshold.

- All companies, including listed public-interest entities (PIEs) will be eligible for the group exemption if they are included in a consolidated sustainability statement.

- Non-EU groups will only need to report if they exceed EUR 450m net turnover generated in the EU and have at least one EU subsidiary or branch with over EUR 200m net turnover, beginning in FY28 (reporting in 2029). Reporting standards for non-EU companies are not expected before October 2027 at the earliest.

Other key changes to CSRD

- Value chain companies with up to 1,000 employees will be protected from excessive information requests from in-scope companies. They can refuse requests that exceed the content of a voluntary reporting standard, to be adopted by the European Commission in 2026. This standard will be based on the existing VSME standard.

- The Commission may develop sector-specific reporting guidance with support for double materiality assessment to identify sustainability matters most relevant to specific sectors. The guidance would be developed through stakeholder consultation and aligned, where appropriate, with international standards.

- The Commission will adopt assurance standards, but later than previously planned with a new deadline of 1 July 2027.

CSDDD: scope and requirements reduced

- Only companies with more than 5,000 employees and EUR 1.5bn net turnover will need to comply with the CSDDD starting in 2029, a delay of a further year. Other key changes are as follows.

- Companies will use a simpler process to identify actual and potential adverse impacts with a scoping process focused on the areas where impacts are likely to occur.

- Companies will not be required to adopt transition plans for climate change mitigation

- The proposed harmonised EU-wide civil liability regime will not be introduced. Penalties imposed on companies at national level will be capped at three percent of net worldwide turnover.

Changes to ESRS and the EU Taxonomy

Companies also now have greater clarity on how they would report under simplified ESRS with reduced disclosures after EFRAG4 submitted its technical advice to the Commission. The Commission intends to adopt the revised standards by mid-2026. Read our guide to understand the proposed changes.

Companies in scope of the CSRD will also be required to report under the EU Taxonomy which is being amended by the Commission. Read more in our article.

The European Financial Reporting advisory Group – the EU’s advisory body on corporate reporting.

What’s next?

The changes to the CSRD and CSDDD enter into force on 18 March 2026. Member states will then have 12 months to transpose them into national law.

Former Wave two and three companies5 will no longer need to report under CSRD due to the ‘Stop the Clock’ directive, unless they meet the revised thresholds. Those that do will start reporting from FY27 (reporting in 2028).

Actions for management to take

- Review the threshold changes to CSRD and CSDDD to understand how they affect your company’s reporting obligations and strategy.

- Monitor ongoing developments in the ESRS simplification process.

- Follow us on LinkedIn and bookmark our page Sustainability reporting in the EU for latest insights.

1 Corporate Sustainability Reporting Directive.

2 Corporate Sustainability Due Diligence Directive.

3 Financial holding companies are defined in the directive as “undertakings the sole object of which is to acquire holdings in other undertakings and to manage such holdings and turn them to profit, without involving themselves directly or indirectly in the management of those undertakings, without prejudice to their rights as shareholders.”

4 The European Financial Reporting Advisory Group – the EU’s advisory body on corporate reporting.

5 Other large companies and listed SMEs.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.