Let’s start by looking at what happened in 2023:

- Funding costs continued to increase dramatically – driven by higher benchmark rates (reflecting the base rate increase from 3.5% to 5.25%, the highest since 2008) whilst credit spreads reduced slightly over the year.

- Despite inflationary pressures and the rising interest rate environment, listed securitisation deal volumes remained strong in 2023, peaking in Q2 following a slower start to the year. Issuance remained concentrated on mortgage-backed deals, with a significant increase in prime RMBS deals compared to 2022.

- The appetite for private market funding remained robust.

- Subordinated debt issuance was stable, albeit more costly.

- Asset performance in securitisation transactions was stable and better than expected given inflationary pressures on borrowers.

- Issuer credit rating changes were on average positive, but UK banking sector 2024 outlooks were a mix of stable to deteriorating, reflecting the impact of wider macroeconomic factors.

The outlook for 2024

So, what might we see in 2024?

We expect funding costs to remain high in 2024 due to higher for longer interest rates, which may begin to fall as the year progresses amid slower GDP growth and lower inflation.

Asset performance amongst RMBS and auto, consumer and SME ABS is expected to weaken in 2024 which may widen credit spreads.

Issuance across all asset types is expected to be stable, with the exceptions of prime RMBS issuance which is expected to grow and BTL and nonconforming issuance which are expected to decline amid reduced mortgage origination for those assets. Issuance in retirement interest only RMBS is expected to grow in the UK in response to increasing life expectancy.

As the Bank of England’s TFSME lending becomes repayable by banks during early 2024, we expect to continue seeing banks increasing their deposit rates to attract savers to replace this funding, alongside increased securitisation issuance.

Funding in charts

Deposit funding

We’re seeing the emergence of a three-speed market:

- Banks that provide current accounts. These banks are reaping the benefits of cost of funding arbitrage, as associated interest rates appear relatively inelastic.

- Banks dependent on best-buy savings rates. There’s a mixed picture, with banks having different abilities to pass increases on to customer lending.

- Non-banks heavily dependent on wholesale funding. There’s a mixed picture here too. For some banks, obtaining affordable wholesale funding will prove challenging. This might result in some players either consolidating or exiting certain lending segments. Banks may start to use retail deposit funding to attack niche segments (e.g., Barclays + Kensington).

Wholesale funding costs

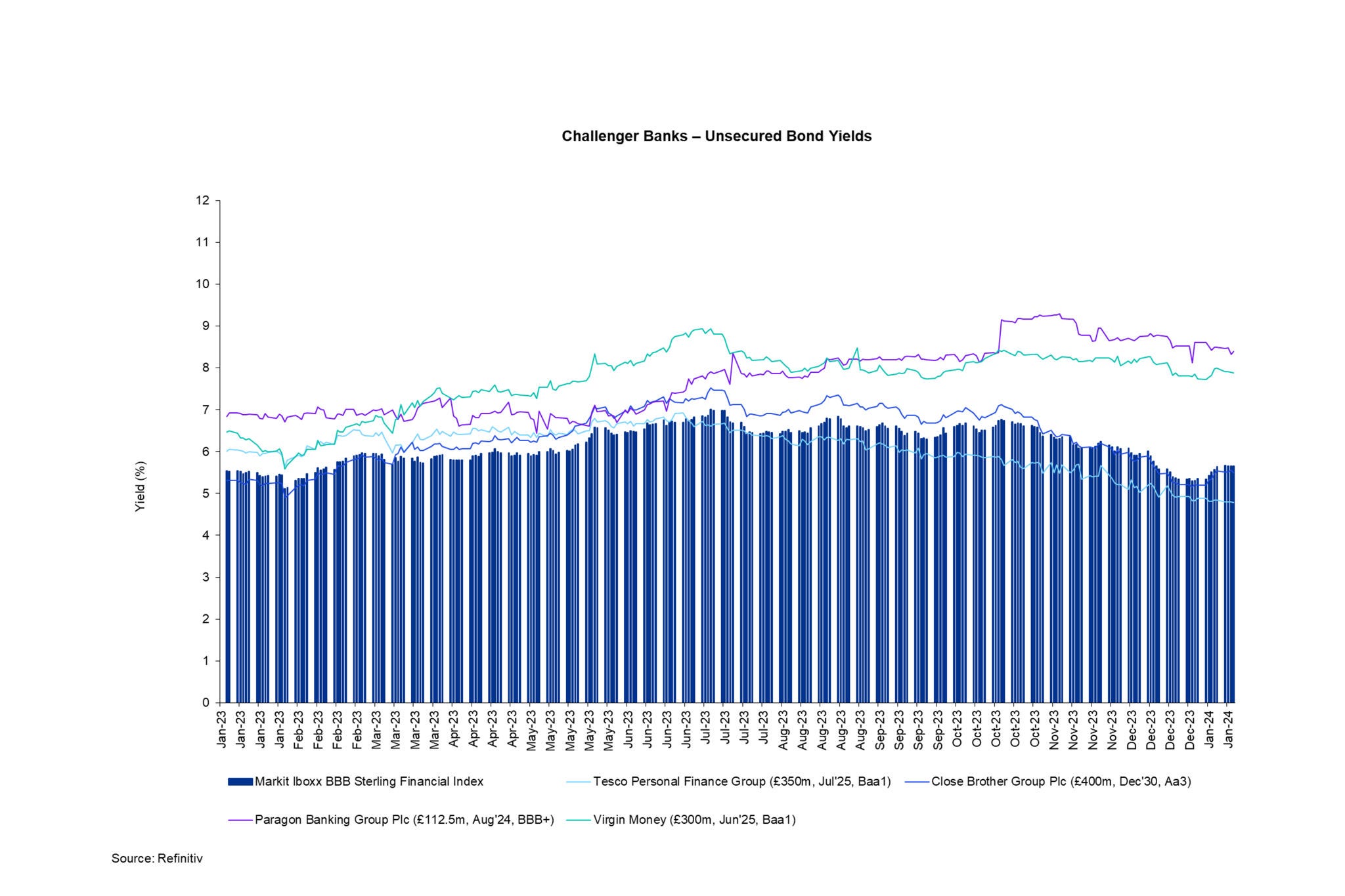

Unsecured bond yields remained relatively stable or increased as the reduction in credit spreads largely offset the volatility in the underlying benchmark rate.

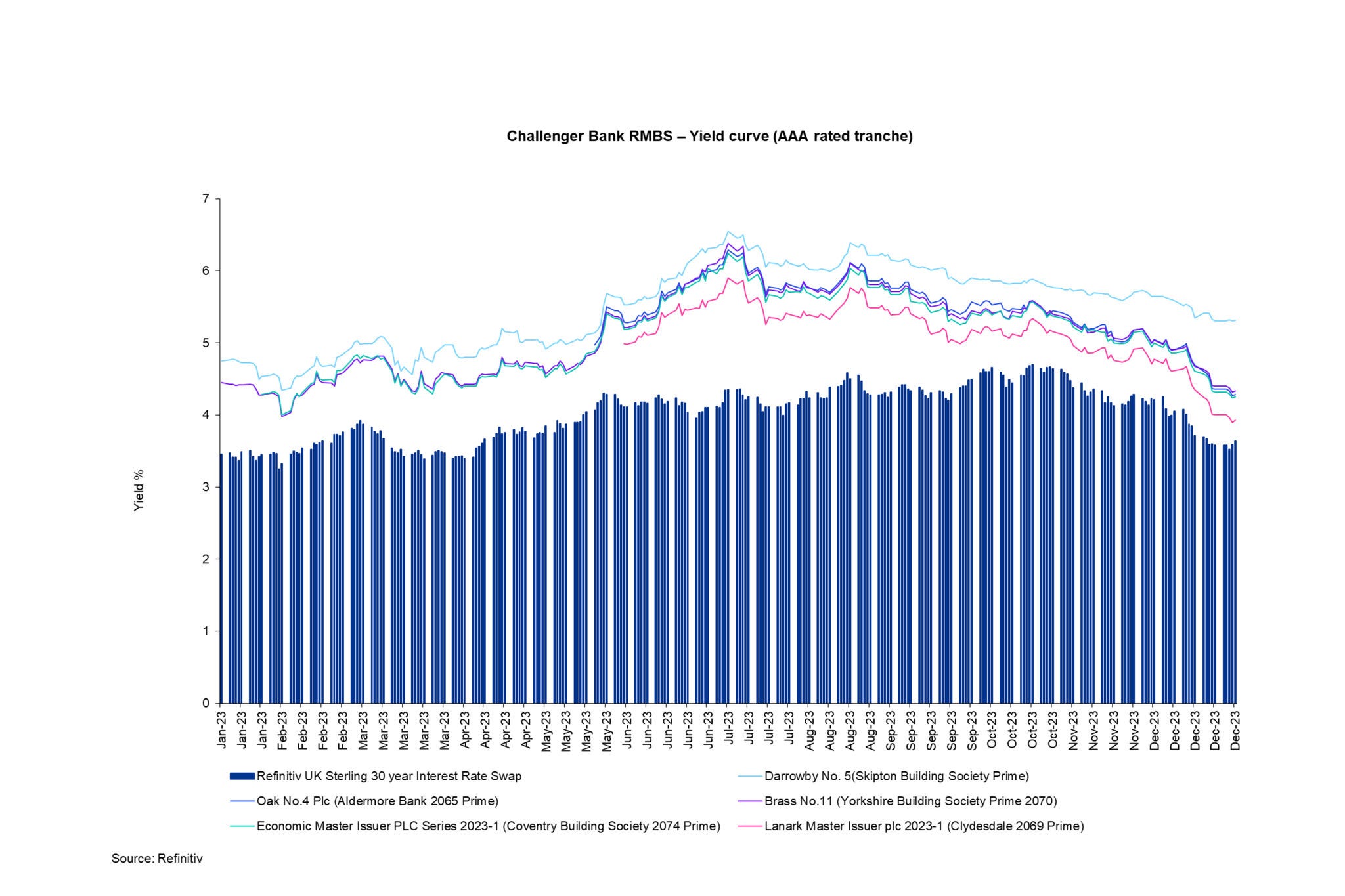

Securitisation yields during the first half of the year driven by benchmark rates and spreads remaining relatively flat, before subsequently reducing through H2 as spreads reduced.

Securitisation market access

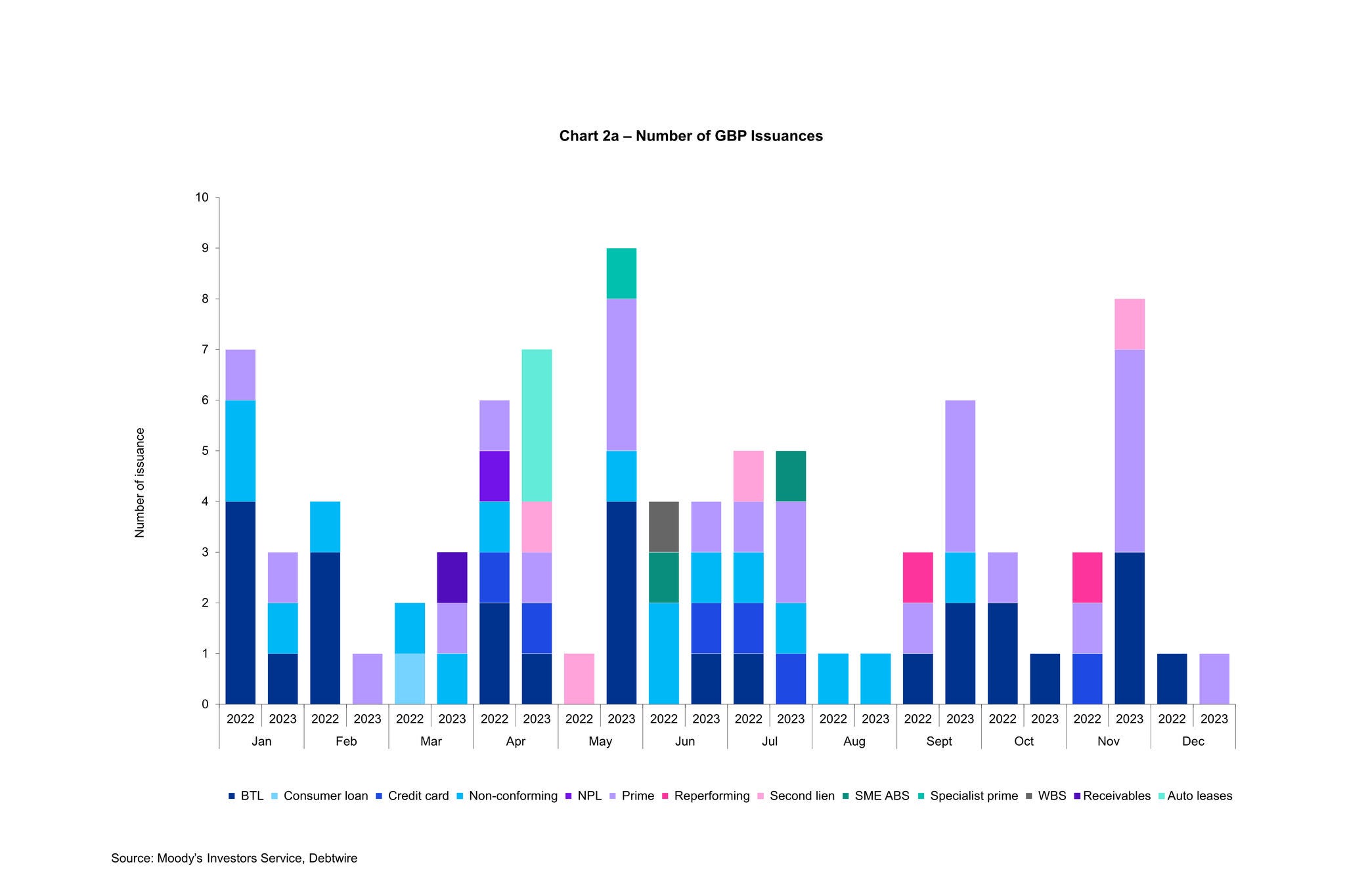

Securitisation issuance across UK RMBS and Asset-Backed Security (ABS) markets increased significantly compared to 2022 with 50 deals completed vs 40 in 2022.

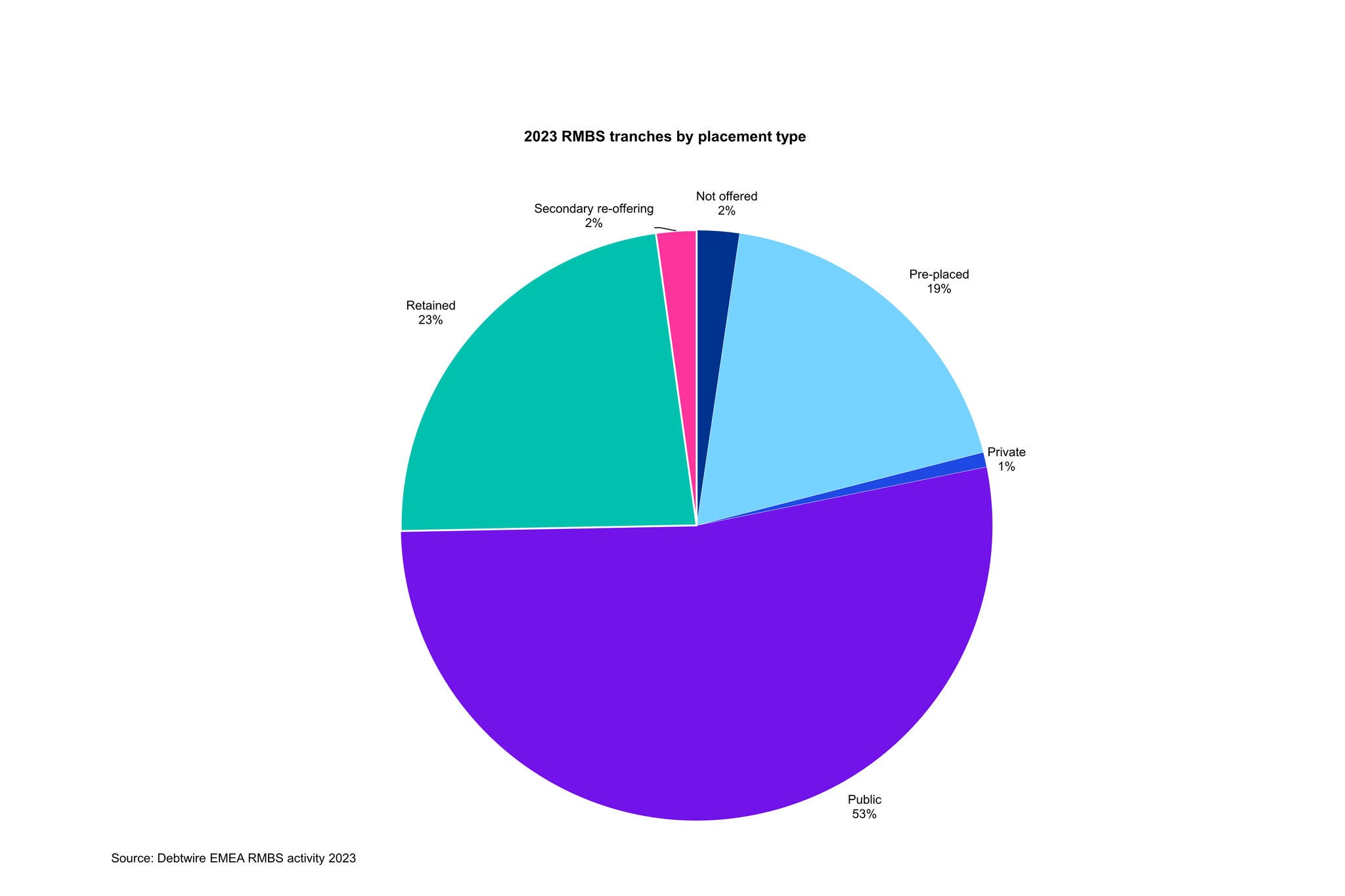

The number of securitisation issuers that had to pre-place or retain securitisation tranches reduced vs 2022 signalling a reduction in the public market disfunction evidenced last year.

[Note: Data for retained tranches excludes unrated junior rates]

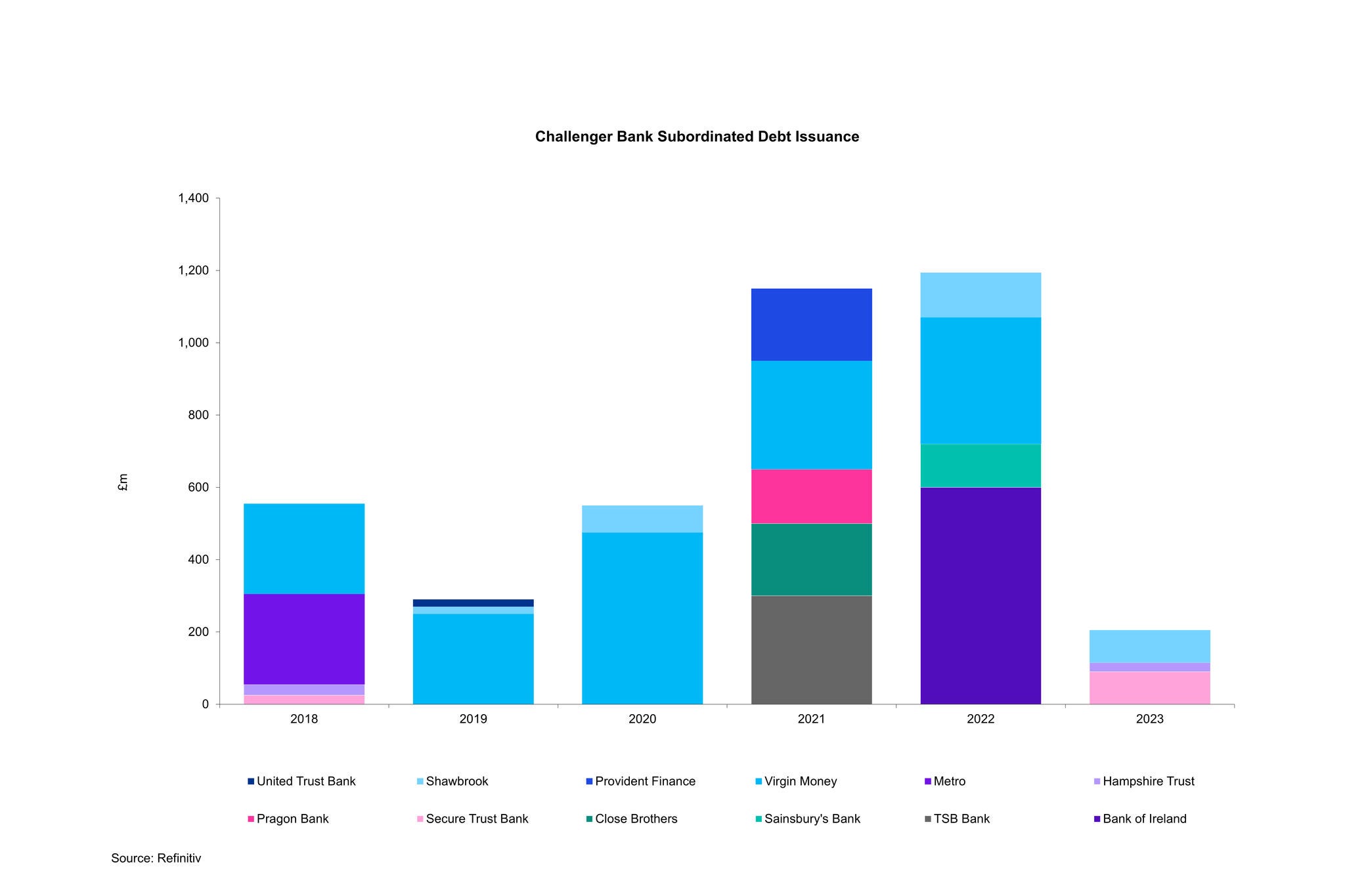

Challenger bank sub-debt issuance reduced significantly in 2023 as issuers continued to pay a premium in an environment of rapidly rising benchmark rates and bond yields.

Private markets

In private structured finance markets, we observed:

- stable credit spreads;

- a renewed appetite for consumer and esoteric assets;

- a continued general appetite for lending more generally;

- a continued cautious approach to credit analysis;

- total return requirements flat from last year, pricing in a significant risk and illiquidity premium to public benchmarks.

Asset performance

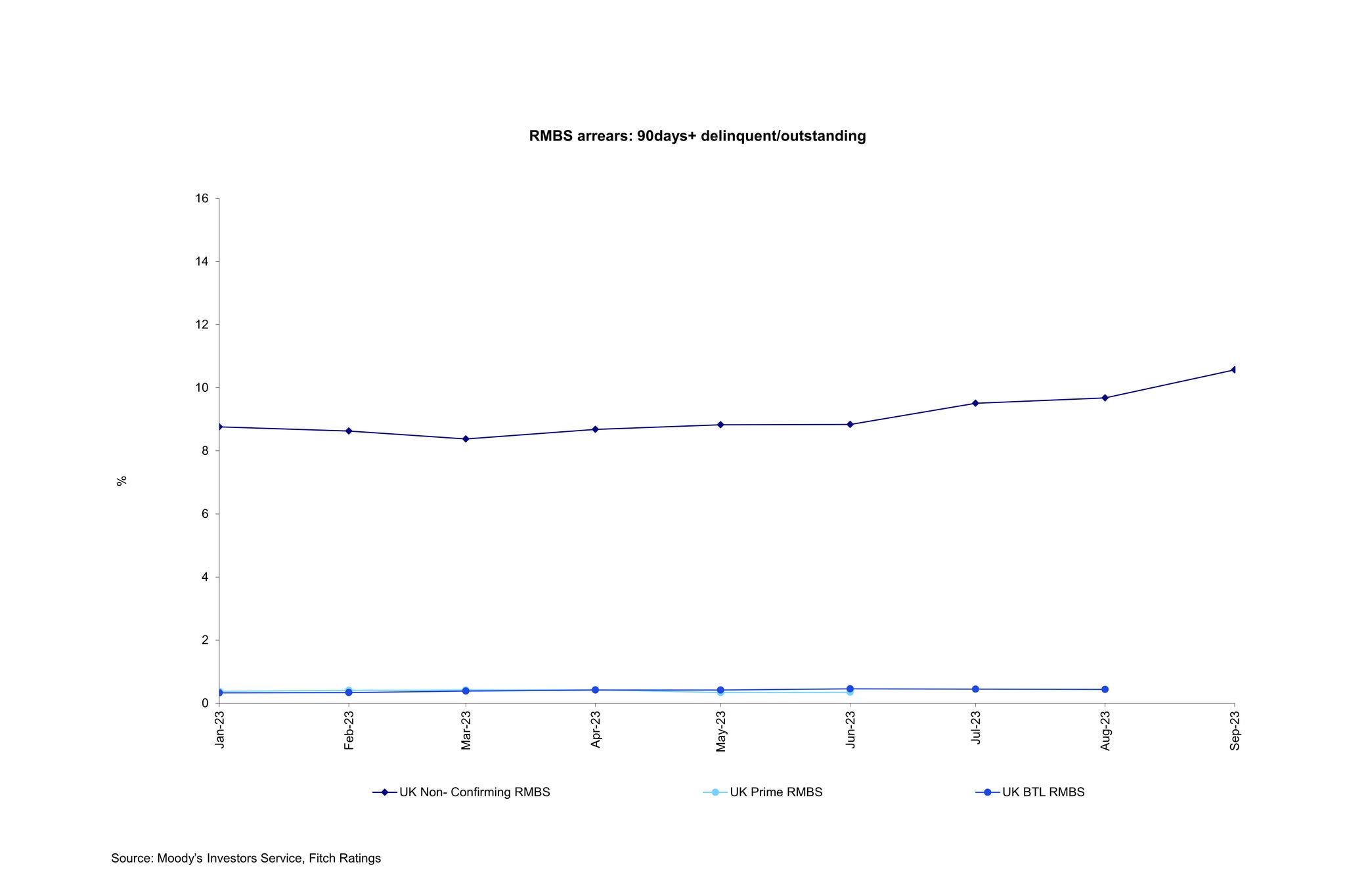

Prime and BTL RMBS arrears were flat through 2023 whilst non-conforming RMBS arrears ticked up throughout the year.

ABS arrears deteriorated through the first half of 2023 before turning a corner and improving through the second half.

Credit ratings

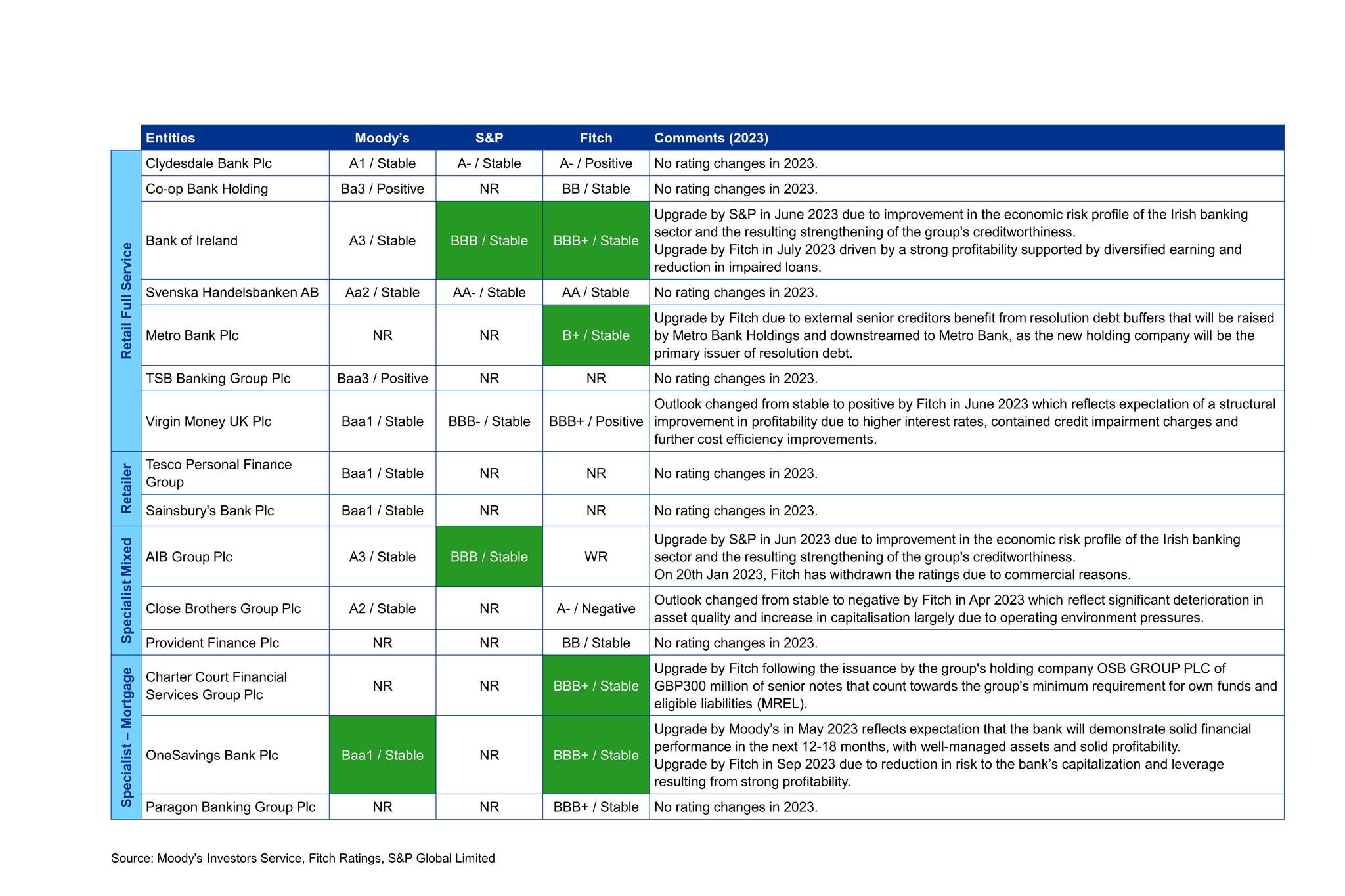

In 2023, most challenger bank credit rating actions were positive.

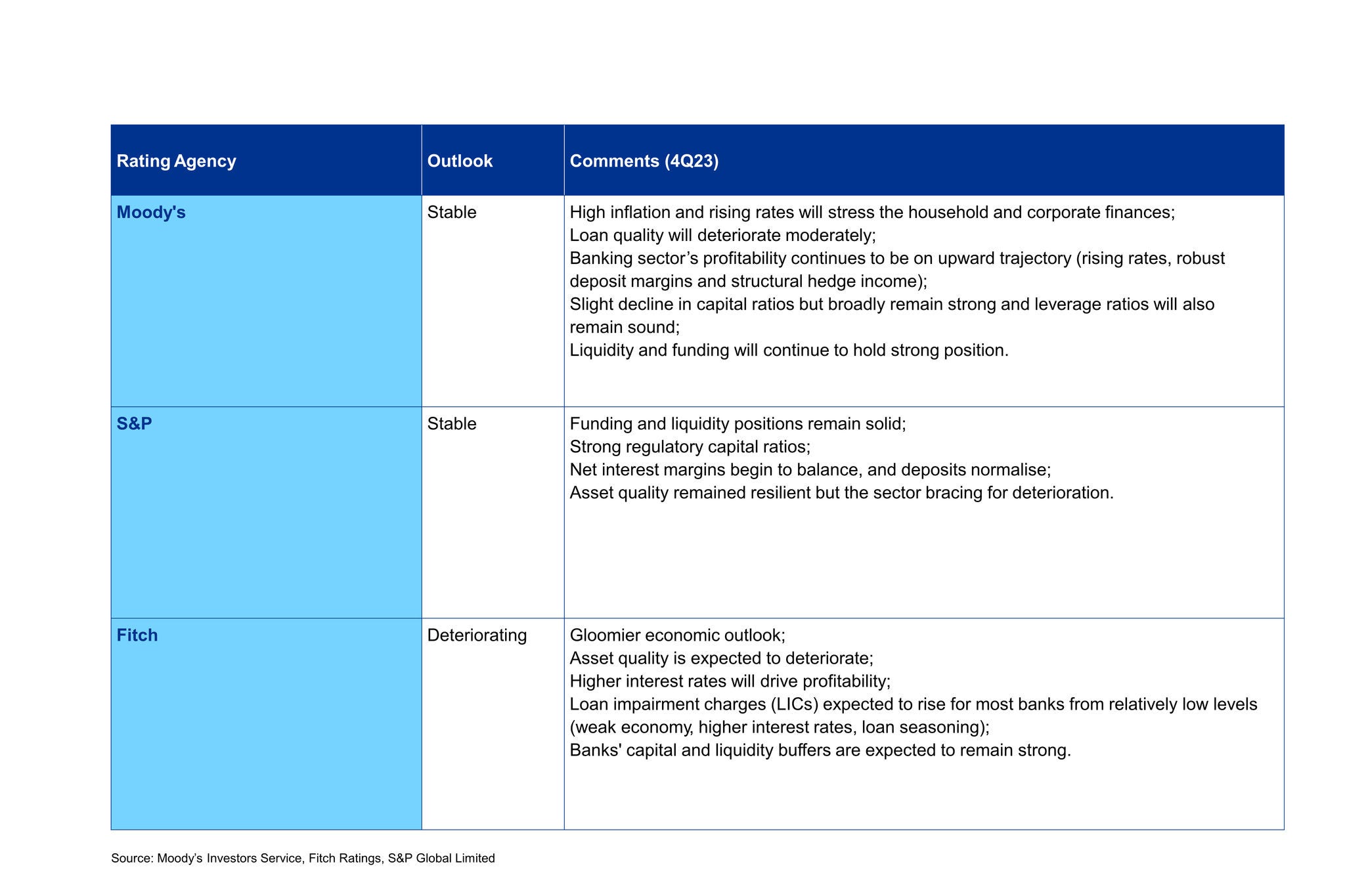

Banking sector 2024 outlooks were a mix of stable and deteriorating sentiment resulting from:

- reducing loan quality;

- stable to reducing profitability from higher funding costs and lower lending volumes; and

- decelerating deposit growth.

- However it is expected that capital will remain stable as banks maintain ample buffers above regulatory minimums.

Our data and analytics insights

Something went wrong

Oops!! Something went wrong, please try again

Our people

Peter Westlake

Partner, Strategy & Performance Transformation, & Head of Challenger Banks and Building Societies

KPMG in the UK