Highlights

The way companies account for their investments in associates and joint ventures impacts how they classify the related income and expenses in the statement of profit or loss. As companies prepare to transition to IFRS 18 Presentation and Disclosure in Financial Statements, questions have been raised about who can apply the fair value option in IAS 28 Investments in Associates and Joint Ventures.

Under targeted amendments issued by the International Accounting Standards Board (IASB), more companies may now be eligible to measure investments in associates and joint ventures at fair value through profit or loss (the ‘fair value option’). Eligible companies can take advantage of a one-time opportunity to elect this option on transition to IFRS 18.

Tara Smith

Partner

KPMG in South Africa

What’s changing in IAS 28?

The amendments are narrow in scope and revise paragraphs 18 and 19 of IAS 28. Specifically, they:

- extend the fair value option to companies with a main business activity of investing in particular types of assets (consistent with the concept of specified main business activities (SMBA) in paragraph 49(a) of IFRS 18); and

- remove the example of an investment-linked insurance fund.

More companies may now be eligible to elect the fair value option under the amendments because any company with an SMBA of investing in particular types of assets (referred to as ‘investing in assets’) is eligible.

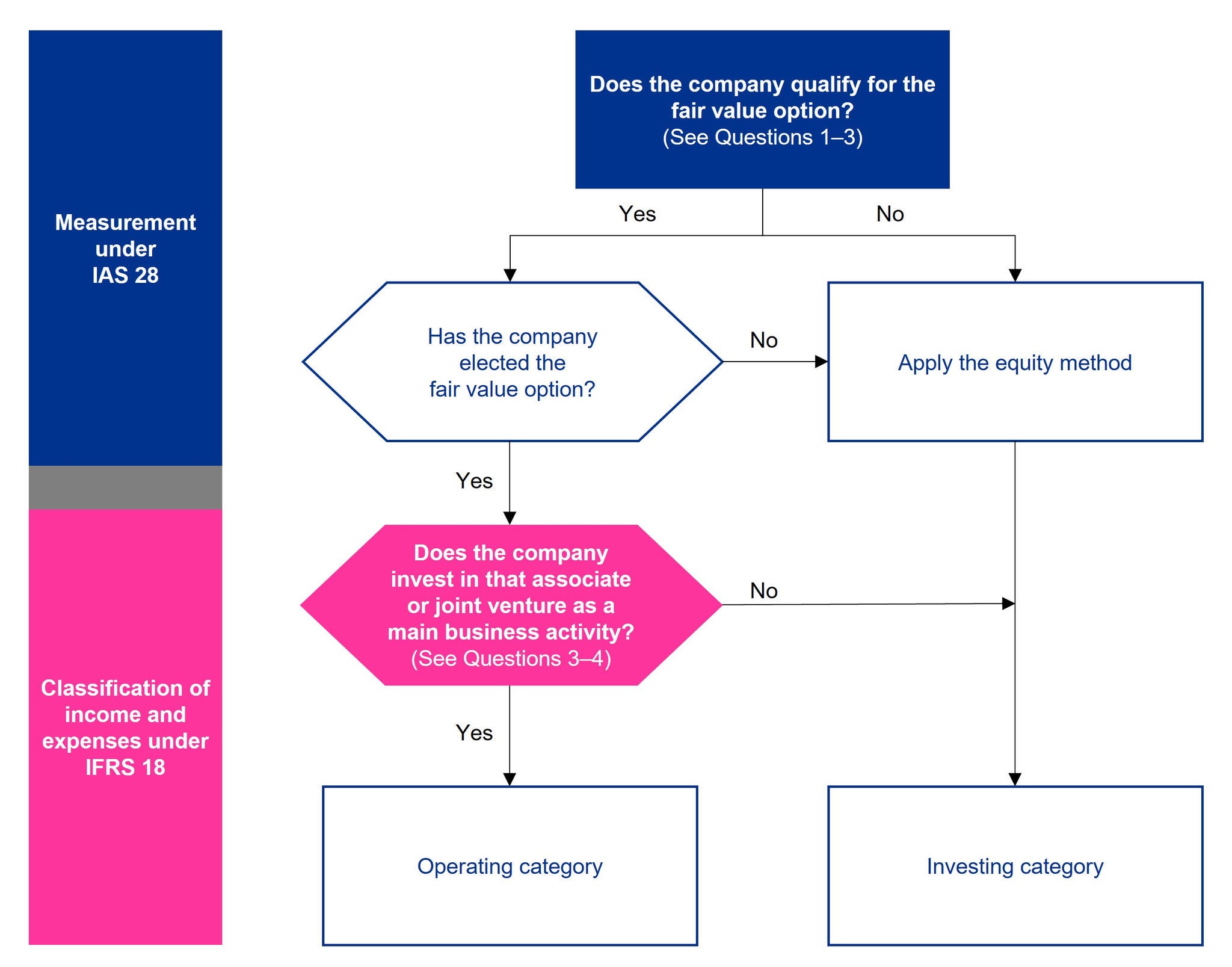

The IASB has only amended IAS 28; it has not amended IFRS 18. However, a company’s measurement elections under IAS 28 may impact presentation under IFRS 18.

Impacts of IFRS 18

Under IFRS 18, income and expenses from investments in associates and joint ventures accounted for under the equity method are classified in the investing category of the statement of profit or loss, even if they arise from the company’s main business activities. However, income and expenses from investments measured at fair value are classified in the operating category if a company invests in them as a main business activity.

The diagram below provides an overview of the approach for measuring investments in associates and joint ventures under IAS 28 and classifying the related income and expenses from those investments under IFRS 18.

For further guidance on IFRS 18, see our publications First Impressions: Presentation and disclosure and Insights into IFRS®.

Effective date and transition

A company applies the amendments to IAS 28 at the same time as it applies IFRS 18, which is effective for annual reporting periods beginning on or after 1 January 2027 (earlier application is permitted). IFRS 18 transitional requirements allow eligible companies (as defined in paragraph 18 of IAS 28) to change their election for measuring an investment in an associate or joint venture from the equity method to fair value through profit or loss on initial application. If a company makes this change, then it applies the change retrospectively under IAS 8 Basis of Preparation of Financial Statements1.

Companies should act now to assess their eligibility under the amended fair value option. Eligible companies should also assess the related presentation impacts when deciding whether to change their existing measurement elections on initial application of IFRS 18.

Speak to your usual KPMG contact to find out more about the IAS 28 amendments and visit kpmg.com/ifrs to keep up to date with the latest news.

Your questions answered

Companies with an SMBA of investing in assets under paragraph 49(a) in IFRS 18 are now eligible to apply the fair value option in IAS 28 to any of their investments in associates and joint ventures. Although IFRS 18 provides examples of companies that might invest in assets as a main business activity (e.g. investment property companies, insurance companies), the IAS 28 amendments are not industry-specific. [IAS 28.18, IFRS 18.B31]

For further guidance on SMBA, see our IFRS 18 publication First Impressions: Presentation and disclosure.

No. The amendments do not affect companies that already use the fair value option in IAS 28 on the basis that they are a “venture capital organisation, mutual fund, unit trust or similar entity”. [IAS 28.18, BC19L]

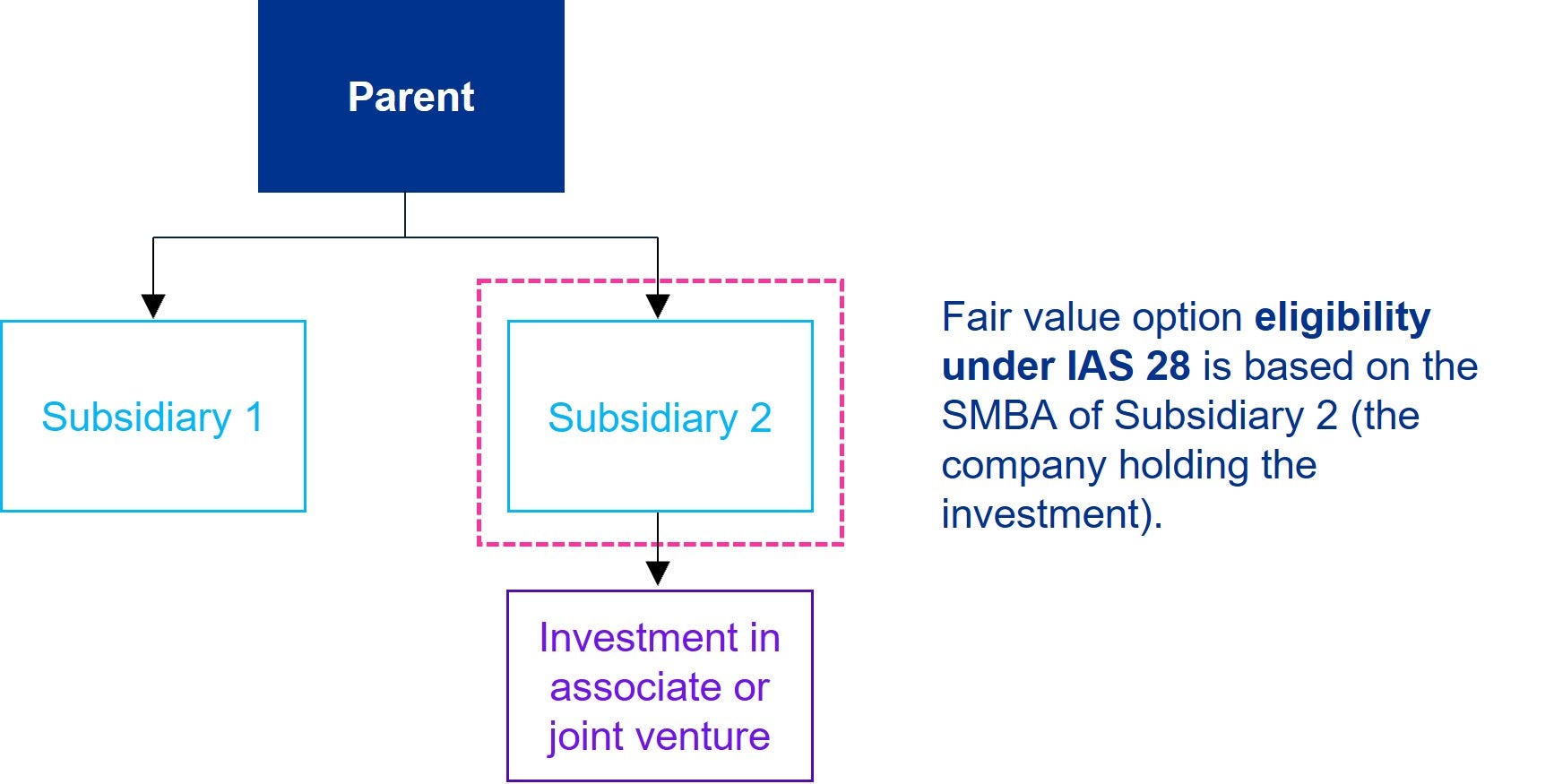

Consistent with current IAS 28 requirements, if a parent holds an investment through a subsidiary (i.e. indirectly), then eligibility for the fair value option depends on the nature of the subsidiary that holds the investment. Therefore, eligibility for the fair value option under the amendments is driven by the SMBA of the subsidiary, which may differ from the SMBA of the group as a whole. [IAS 28.18–19, BC19Q, IFRS 18.B37]

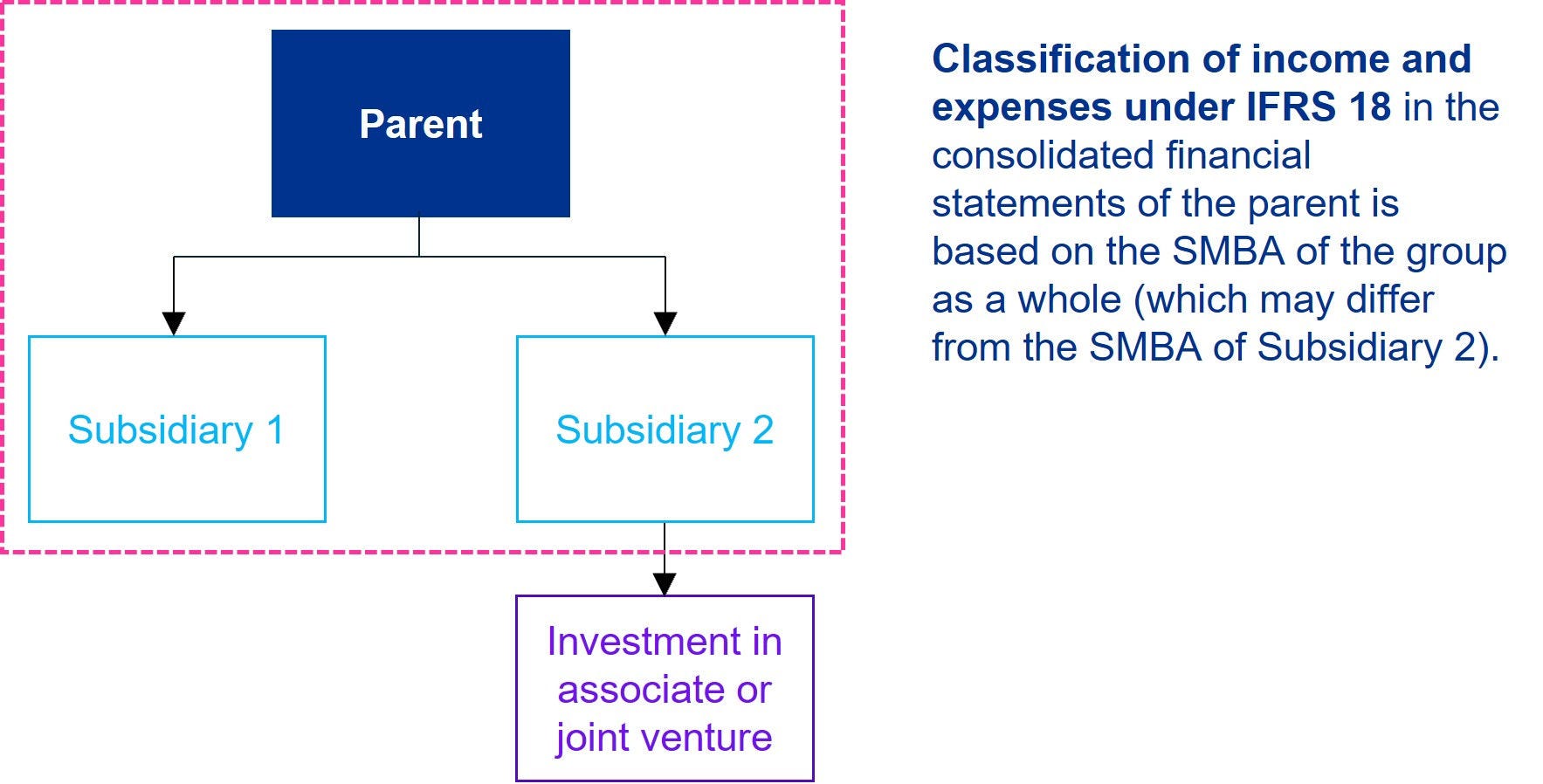

However, in the consolidated financial statements of the group, classification of income and expenses under IFRS 18 is based on the SMBA of the group as a whole (see Question 4). [IAS 28.BC19R, IFRS 18.B37, BC98]

No. Under IFRS 18, a company (the reporting entity preparing financial statements) only classifies income and expenses from investments in associates and joint ventures measured at fair value through profit or loss in the operating category if it:

- has an SMBA of investing in assets under paragraph 49(a) of IFRS 18. For consolidated financial statements, this assessment is based on the SMBA of the group as a whole, which may differ from the SMBA of a subsidiary within the group holding the investments (see Question 3); and

- invests in those associates and joint ventures as a main business activity (applying paragraphs 53 and 55 of IFRS 18). A company performs this assessment by individual asset or using a group of assets with shared characteristics. [IAS 28.BC19P–BC19R, IFRS 18.49, 53, 55, B37–B38, BC98]

For further guidance, see our IFRS 18 publication First Impressions: Presentation and disclosure.

Generally, no. Consistent with current IAS 28 requirements, the fair value option is elected at initial recognition of the investment. [IAS 28.18]

However, eligible companies (as defined in paragraph 18 of IAS 28) have a one-time opportunity to change their current measurement from the equity method to fair value through profit or loss on transition to IFRS 18. [IAS 28.45M, IFRS 18.C7]

When an eligible company using the equity method elects to use the fair value option on transition to IFRS 18, this change is applied retrospectively under IAS 8. Therefore, the requirements of IAS 8, including the relevant disclosure requirements, apply. [IAS 8.28, IAS 28.45M, IFRS 18.C7]

In addition, IFRS 12 Disclosure of Interests in Other Entities sets out the disclosure requirements for investments in associates and joint ventures, including whether each material investment is measured under the equity method or at fair value through profit or loss. [IFRS 12.21(b)]

Yes. However, the IASB decided to continue restricting the fair value option to certain companies. It may explore an unrestricted fair value option as part of its future work plan priorities. [IAS 28.BC19K]

If an eligible parent company elects to apply the fair value option in its consolidated financial statements, then it accounts for its investments in associates and joint ventures in the same way in its separate financial statements. If it changes to the fair value option on initial application of IFRS 18, then it makes the same change in its separate financial statements. [IAS 27.11, IFRS 18.C7]

However, the classification of income and expenses from investments in associates and joint ventures measured at fair value may differ in the parent’s separate financial statements compared to the consolidated financial statements. This is because they are different reporting entities that may have different SMBAs. [IFRS 18.B37, BC98]

1 Previously IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.