(This article was published on 23 March 2022 and updated on 10 December 2025)

What’s the issue?

External events may trigger economic uncertainty. This may impact how companies evaluate and disclose events after the reporting date (‘subsequent events’). Depending on a company’s reporting date, the impacts of specific external events could be adjusting or non-adjusting.

Under IAS 10 Events After the Reporting Period, both favourable and unfavourable events that occur between the reporting date and the date when the financial statements are authorised for issue require disclosure, or possibly affect recognition and measurement, in the financial statements.

Companies need to disclose the date on which the financial statements were authorised for issue and who gave such authorisation. This disclosure informs users of the date to which events have been considered – i.e. any event that occurs after this date is not disclosed or reflected in the current period’s financial statements.

Companies need to exercise significant judgement in determining which events after the reporting date are adjusting events.

Getting into more detail

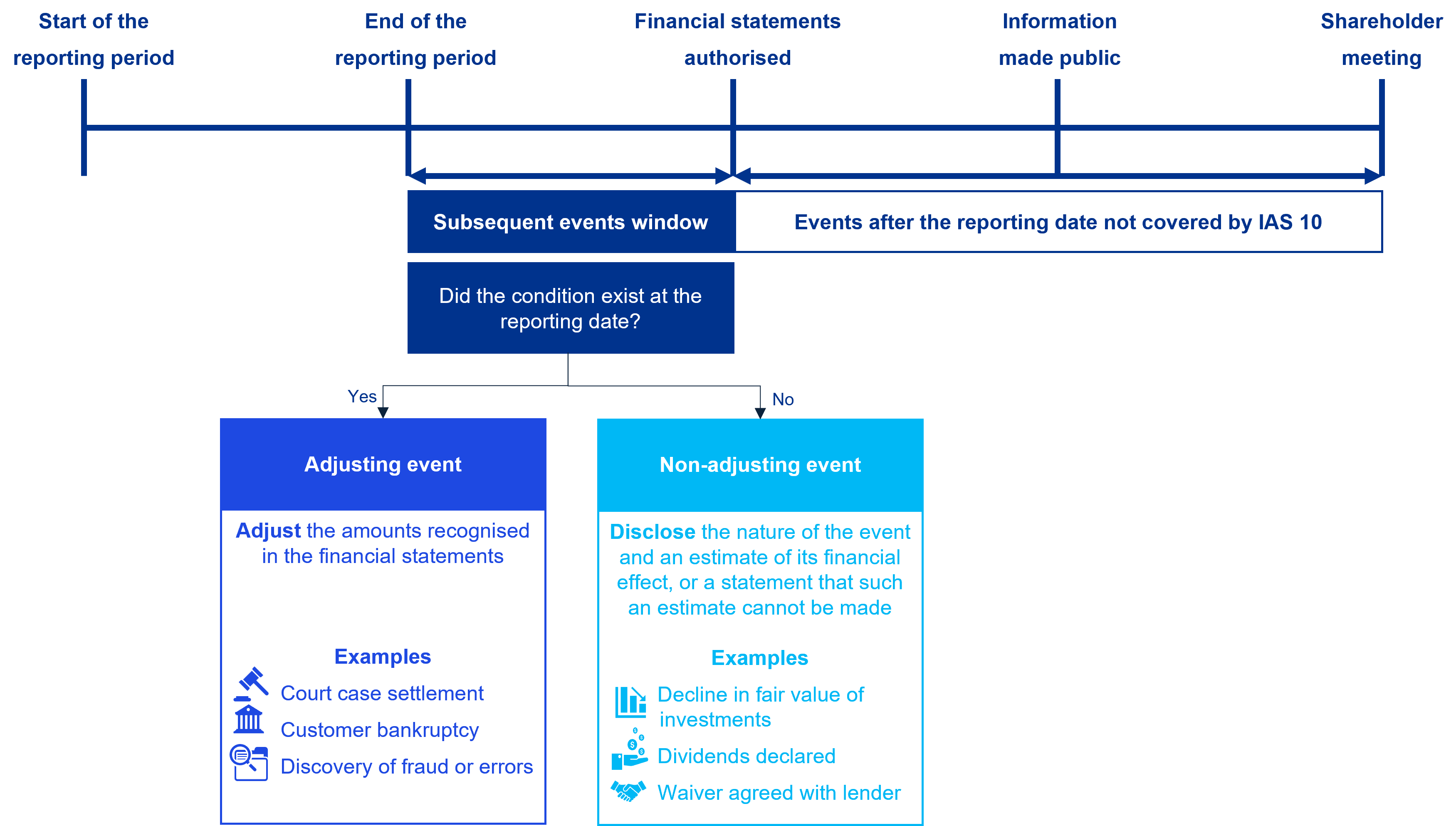

The following diagram illustrates the scope of IAS 10, which deals with events that occur after the reporting date but before the financial statements are authorised for issue. However, IAS 10 does not change recognition or measurement under the specific accounting standards.

Subsequent events

The financial statements are adjusted to reflect events that occur after the reporting date, but before the financial statements are authorised for issue, if they:

- provide evidence of conditions that existed at the reporting date (adjusting events); or

- indicate that the going concern basis of preparation is inappropriate.

In contrast, non-adjusting events are events that are a result of conditions that arose after the reporting date.

It may be challenging to determine whether an event occurring after the reporting date provides evidence of a condition that existed at the reporting date.

Some events after the reporting date are triggered by a pre-existing condition. In such cases, it is necessary to determine the underlying causes of the event and its timing to determine the appropriate accounting.

In other cases, multiple events may occur, some before and some after the reporting date, making it challenging to determine whether they affect the financial position and performance at the reporting date or they affect disclosures only. Companies would need to exercise judgement based on their specific facts and circumstances.

Disclosures

For material non-adjusting events, companies are required to disclose:

- the nature of the event and an estimate of its financial effect; or

- a statement that an estimate cannot be made.

A non-adjusting event is considered material if it is of such importance that non-disclosure would affect the ability of the financial statements’ users to make proper evaluations and decisions.

As the date of authorisation moves further from the reporting date, users might expect that a company would have more information available to disclose an estimate of the financial effects of a non-adjusting event.

Actions for management

When assessing the impact of events after the reporting date, management needs to do the following.

- Identify and consider all subsequent events until the date the financial statements are authorised for issue and determine whether these events are adjusting – i.e. provide evidence of conditions that existed as at the reporting date or indicate that the going concern assumption is inappropriate.

- Disclose the nature and financial effects of events that are considered to be material, even if they are non-adjusting.

© 2026 KPMG IFRG Limited, a UK company, limited by guarantee. All rights reserved.