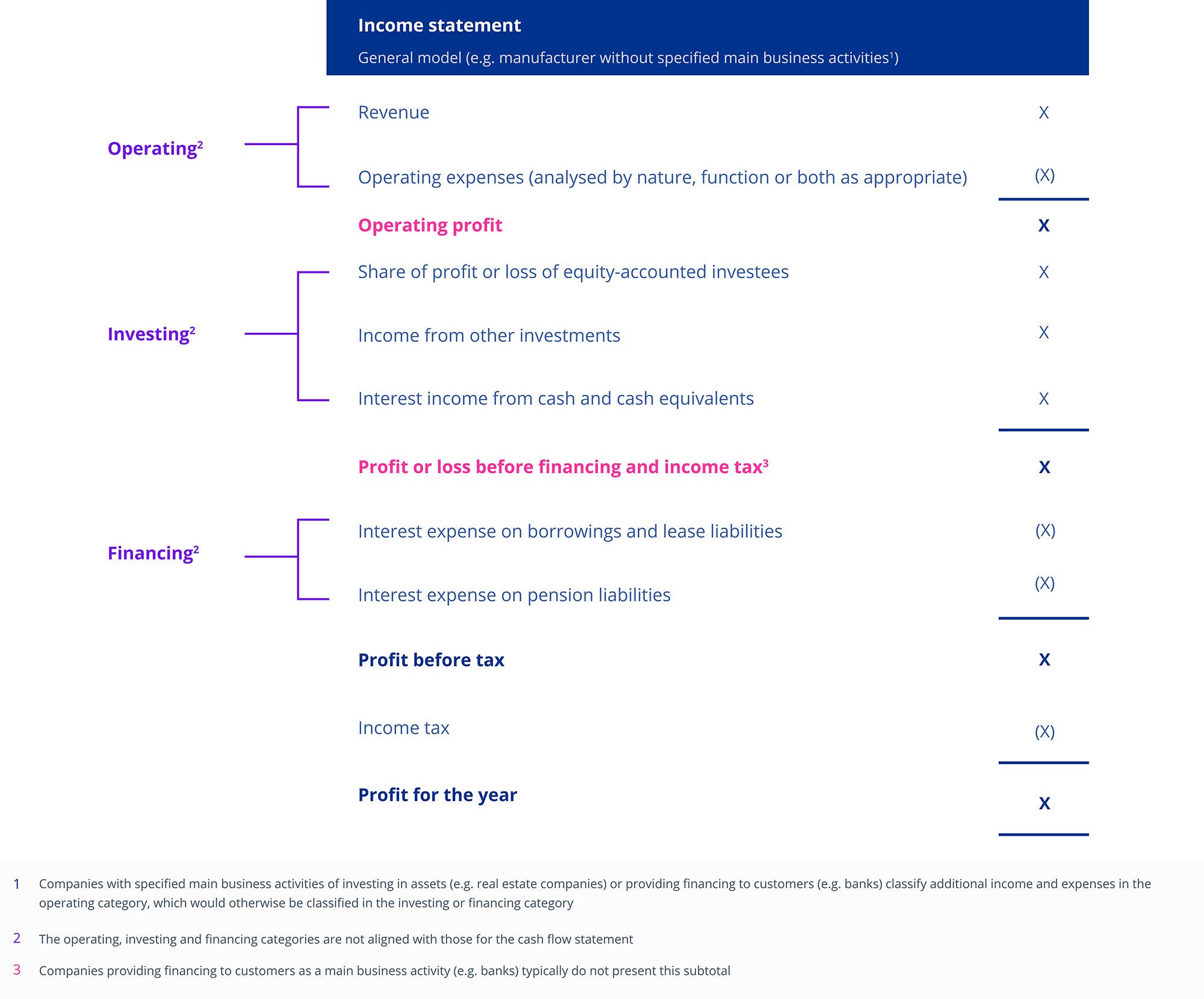

Companies will need to prepare new or update disclosure within the notes to the financial statements for the analysis of operating expenses by nature (if presentation by function or mixed presentation is used in the income statement) and MPMs (if they communicate using measures that are MPMs). In addition, companies may need to further disaggregate the information disclosed in existing notes.

Companies will need to understand how the underlying data needed to provide or update the relevant disclosures will be sourced, and if any data collection processes and controls need to be updated to facilitate this.

Some companies may need to adapt their financial reporting systems to track and collate the more disaggregated information and classify income and expenses into the new categories.

The system implications may be more significant for companies presenting an analysis of operating expenses by function or mixed presentation on the face of income statement.

System implications may also arise, for example, where:

- the output of one group company is the input of another group company and the nature of expense is lost or not tracked at the consolidated level. This may be more significant where the standard costing method for inventories is used.

- there is more than one set of business activities in the group, and the classification of items of income and expenses will be different at the consolidated level as compared to the operating company level.

- IFRS 18 includes specific classification requirements—for items such as foreign exchange differences, fair value gains and losses on derivatives and income and expenses from hybrid contracts. Such income and expenses may therefore need to be classified into different income statement categories. Some companies may also utilise separate treasury management systems to record information on financial instruments at a more granular level compared with the ERP systems, which may also require updates.

Companies may need to review charts of accounts, update transaction recording systems, revise consolidation processes, add new data points for disclosures or design revised control procedures to ensure compliance.