Climate scenario analysis for banks and financial institutions

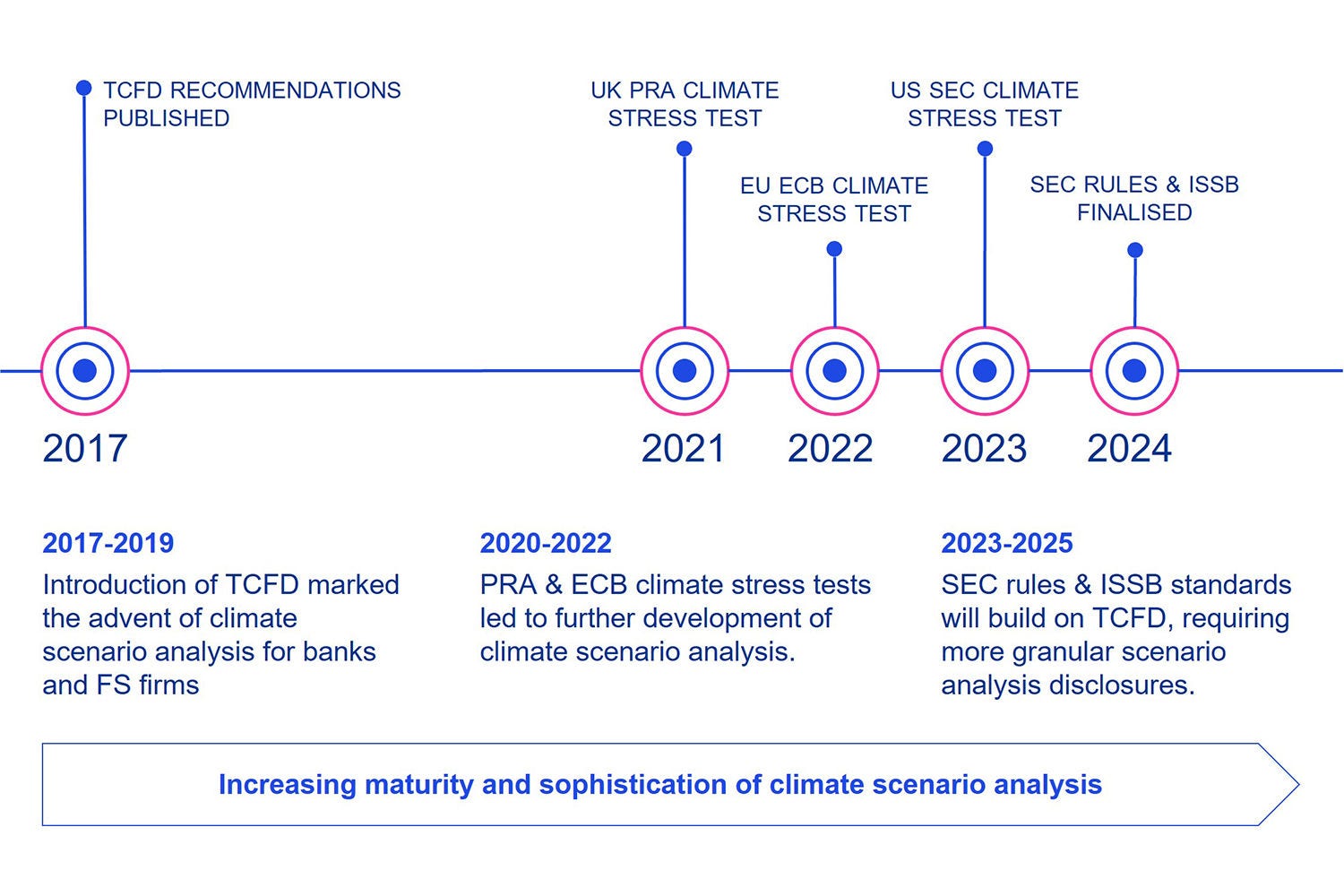

Significant progress has been made over the last five years in the field of climate scenario analysis for banks and financial institutions, from early TCFD disclosures to developments by the PRA and ECB climate stress tests. In this three-part series on climate scenario analysis, we examine the key focus areas where firms and supervisors expect further enhancements to banks and other financial institutions’ end-to-end climate risk scenario analysis models.

Climate scenario analysis has been a key area of capability development by banks, driven by increasing global regulations (see Figure 1) and its value as a climate risk management tool. As recognised by TCFD and other climate-related disclosure regulations, it can help firms to better understand and manage their physical and transition risks, identify opportunities, inform strategy and build resilience on the journey to net zero.

There are three main stages to climate scenario analysis, which we will explore as part of a trilogy of articles on this topic:

- Part 1: Scenario generation

- Part 2: Impact quantification

- Part 3: Response evaluation

This first article shines a spotlight on scenario generation.