Our latest UK Tech Monitor report covering Q1 2021, found that tech companies are more optimistic about the near-term growth than any time since the second quarter of 2014.

Survey respondents reported increased confidence levels in business activity rebounding, following a challenging start to the year due to a third national lockdown and new trading relationship arrangements with the EU, which created uncertainty among clients in the opening months of the year. As a result of increased confidence, tech sector firms added to their payroll numbers in Q1, signalling the fastest pace for recruitment in the sector for nearly two years.

The fastest growth in jobs in almost two years provides a clear signal that tech companies are confident about future workloads and expect to receive a boost from improving UK economic prospects. The successful vaccine rollout and optimism about corporate technology investment were key factors helping to drive up business expectations to a seven-year high in the first quarter of the year.

Job creation heats up as UK tech sector outlook improves in Q1

In the survey data from the UK Tech Monitor Index we found that the technology sector remained in expansion mode during Q1 2021, despite a jolt to activity at the start of the national lockdown in January. In February and March this output picked up, leaving the tech sector recovery on a healthy trajectory by the end of the first quarter. Resilient demand conditions also led to the fastest rise in employment since Q2 2019 and the strongest output growth projections for nearly seven years.

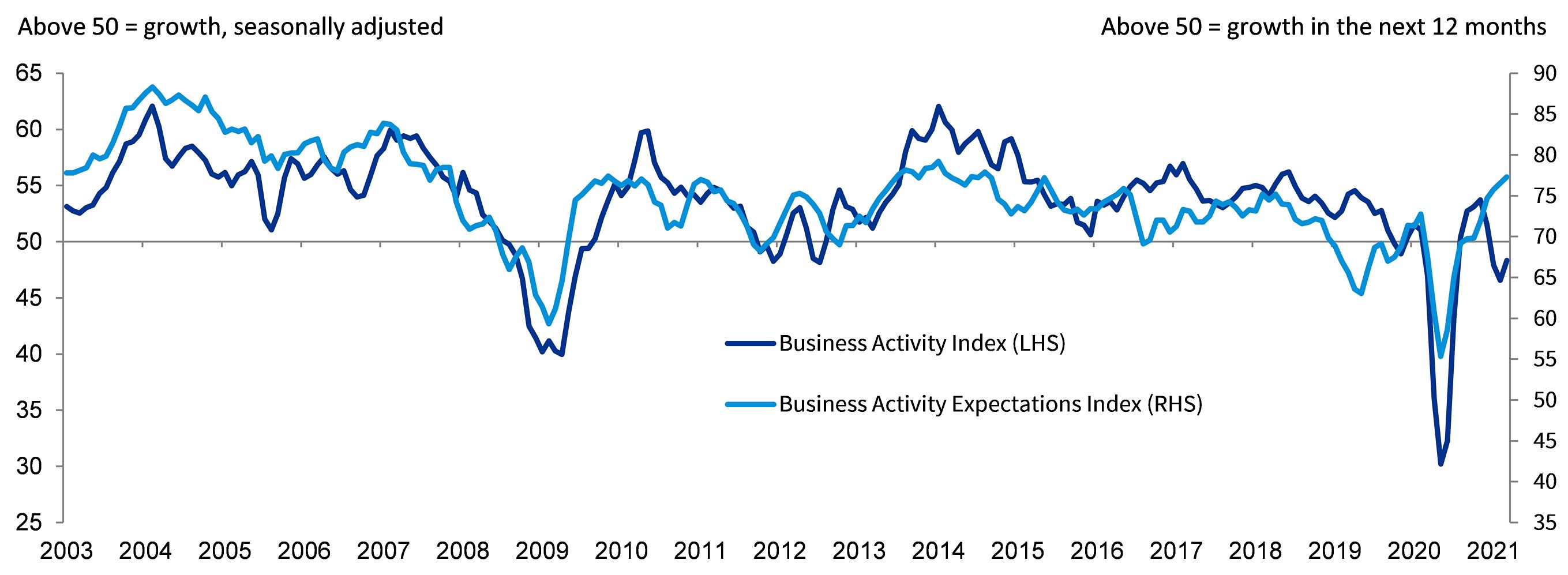

KPMG UK Tech Monitor Index

As well as this, the index measuring UK tech employment rose from 51.5 in Q4 2020 to 51.8 in Q1, which indicated the strongest rate of job creation since Q2 2019. These sustained efforts to boost staffing numbers contrasted with another slight drop in the rest of the UK’s private sector employment throughout Q1.

Confidence highest since Q2 2014

One of the key factors driving employment growth across the tech sector was stronger optimism towards the 12-month business outlook. At 77.3 in Q1, the index measuring growth expectations rose from 74.7 in Q4 and hit its highest level since Q2 2014. Optimism was stronger than in all other parts of the UK private sector, except for hotels and restaurants – many of which have not been trading for 9 of the last 12 months.

Vaccine progress was frequently linked to these upbeat forecasts, and the prospect of rapid economic growth once restrictions are eased. There were also mentions of previously delayed product launches and greater investment in areas such as cloud technology, e-commerce platforms and AI software.

Business activity falls modestly

At 48.3 in Q1, the headline Business Activity Index dropped from the 51.5 it had previously scored in Q4 2020, and signalled an overall loss of recovery momentum since the end of last year. The third national lockdown, combined with Brexit disruption, drove a substantial drop in business activity during January. Although growth emerged in February and March, the initial decline weighed heavily on the index reading for Q1.

Business activity also fell across the UK private sector as a whole during the opening quarter, largely reflecting a slump in consumer services. However, the economic downturn was much softer than seen at the start of the coronavirus disease 2019 (COVID-19) pandemic.

Slight drop in new orders

The stricter government stringency measures and subsequent disruption to clients’ business operations drove a slight reduction in new order intakes at tech firms during Q1.

Some survey respondents mentioned that export sales to European clients were adversely impacted by uncertainly after the end of the Brexit transition period. Encouragingly, monthly data showed that total new orders returned to growth in March as the vaccine rollout and roadmap for reopening the economy helped to boost demand.

Inflationary pressures pick up

Encouragingly, we also found that the rising costs for staff, transportation and electronic components led to the sharpest increase in tech sector input prices for nearly four years in Q1. As a result of this, technology firms sought to alleviate the squeeze on margins from higher costs, with prices charged raised at the fastest pace since Q2 2019.

About the UK Tech Monitor report

KPMG releases a quarterly report highlighting the key trends, opportunities, and challenges facing the technology sector.

KPMG uses IHS Markit as the provider of the UK Tech Monitor Index data for the UK Tech Monitor Report.

Please note, these figures are accurate as of 19th April 2021.