The Iran conflict has evolved from a geopolitical event into a source of material operational risk, with developments in the Persian Gulf affecting trade routes, energy markets, and business planning assumptions. Ceasefire pauses have created limited political space but have not translated into commercial normalization, with persistent security, insurance, policy and supply-chain frictions likely to shape short, medium and long-term operating performance, risk premia and valuations.

The Iran conflict: From geopolitical event to valuation risk

> Click on the image to enlarge it

> Click on the image to enlarge it

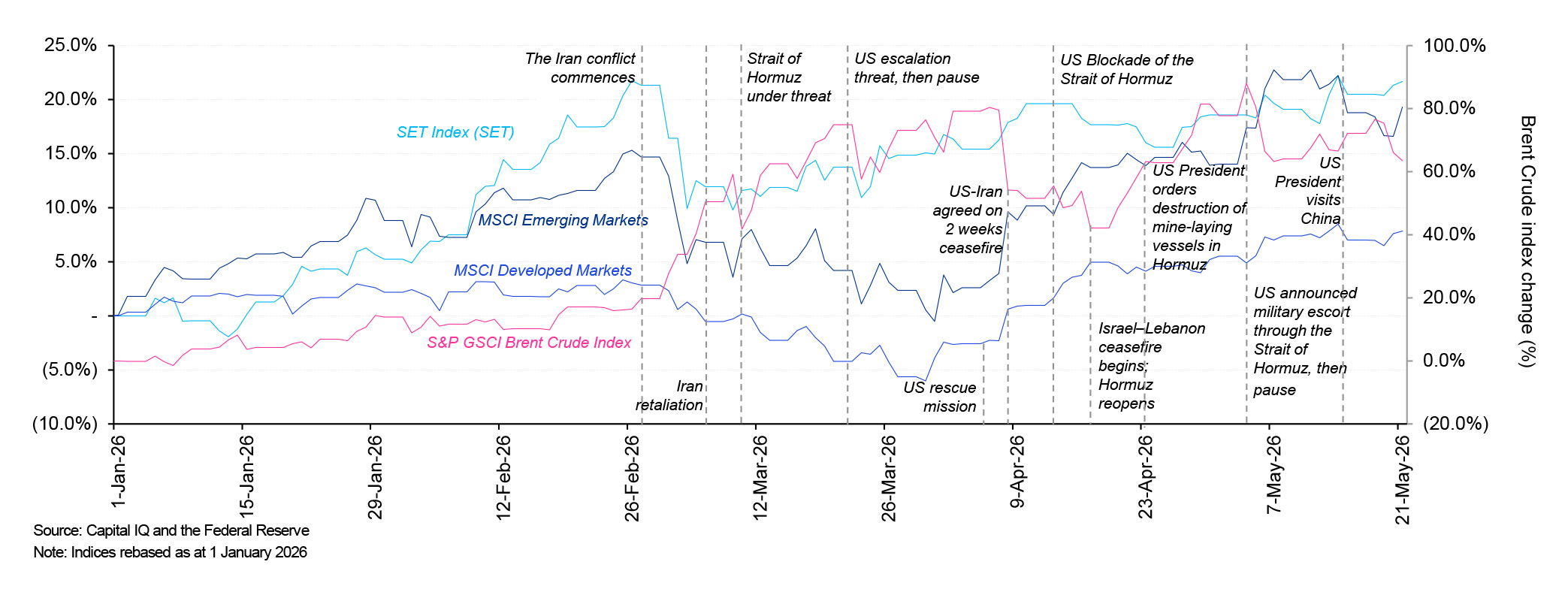

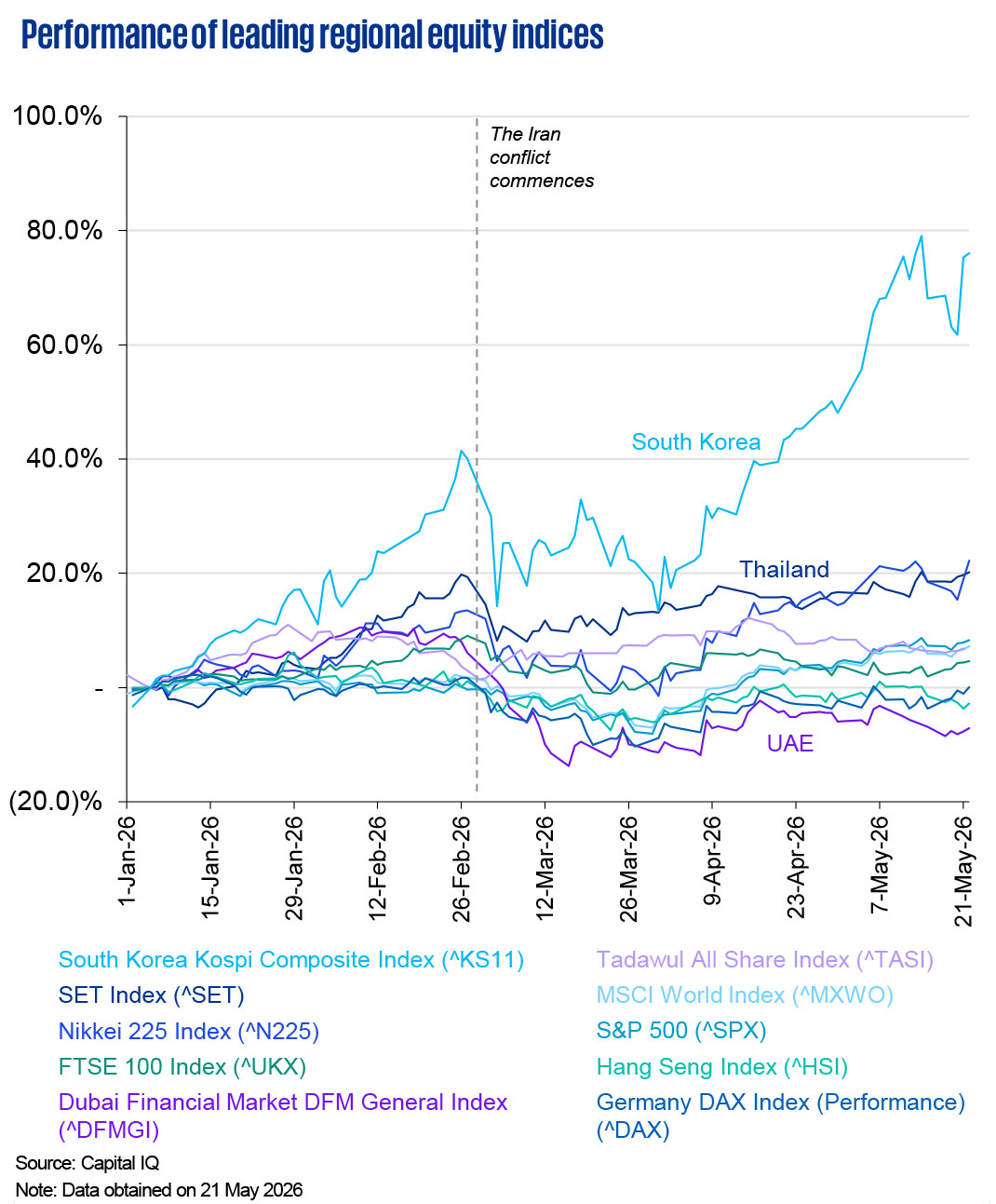

Current status: There is no defined ceasefire or resolution timeline. Commercial shipping through the Persian Gulf and Strait of Hormuz remains restricted. Insurance premia, freight costs and security surcharges remain elevated across affected trade corridors, which in turn put downward pressure on equities across most regions.

Thai markets weathering the Iranconflict

> Click on the image to enlarge it

> Click on the image to enlarge it

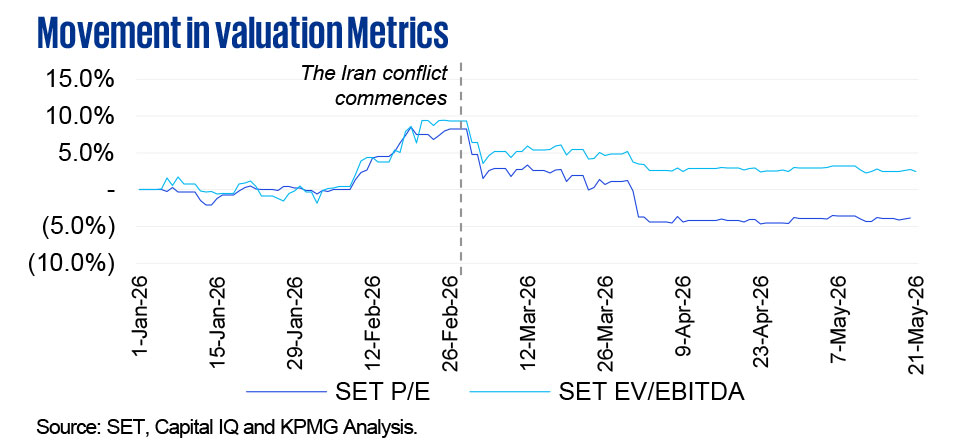

SET remained resilient with stable valuations and index performance driven mainly by tech and energy stocks and portfolio inflows.

> Click on the image to enlarge it

> Click on the image to enlarge it

> Click on the image to enlarge it

> Click on the image to enlarge it

> Click on the image to enlarge it

> Click on the image to enlarge it

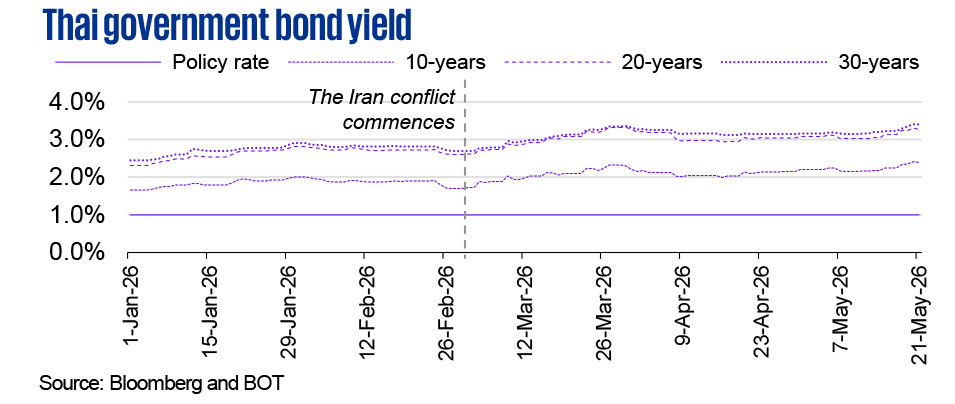

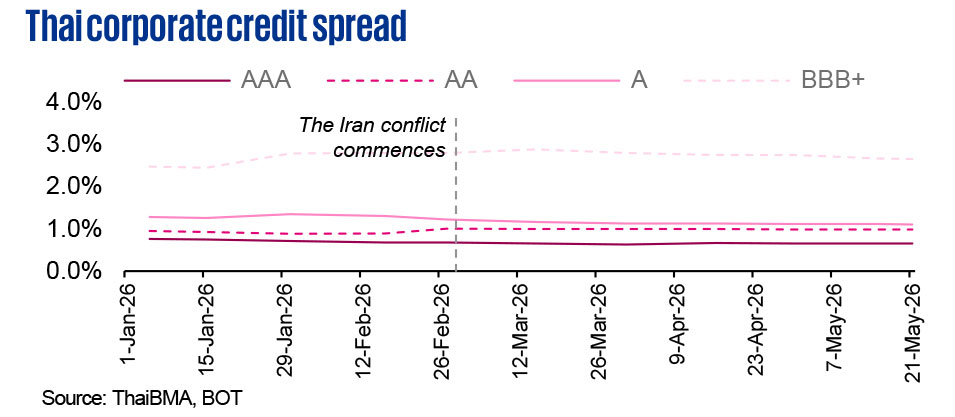

Since the conflict began, market valuation multiples have contracted while Thai government bond yields have increased. However, credit spreads across investment-grade bonds have remained broadly stable, aside from a modest widening in the BBB+ segment, indicating that the repricing is largely systemic rather than credit-specific.

Thailand perspective

Valuation considerations

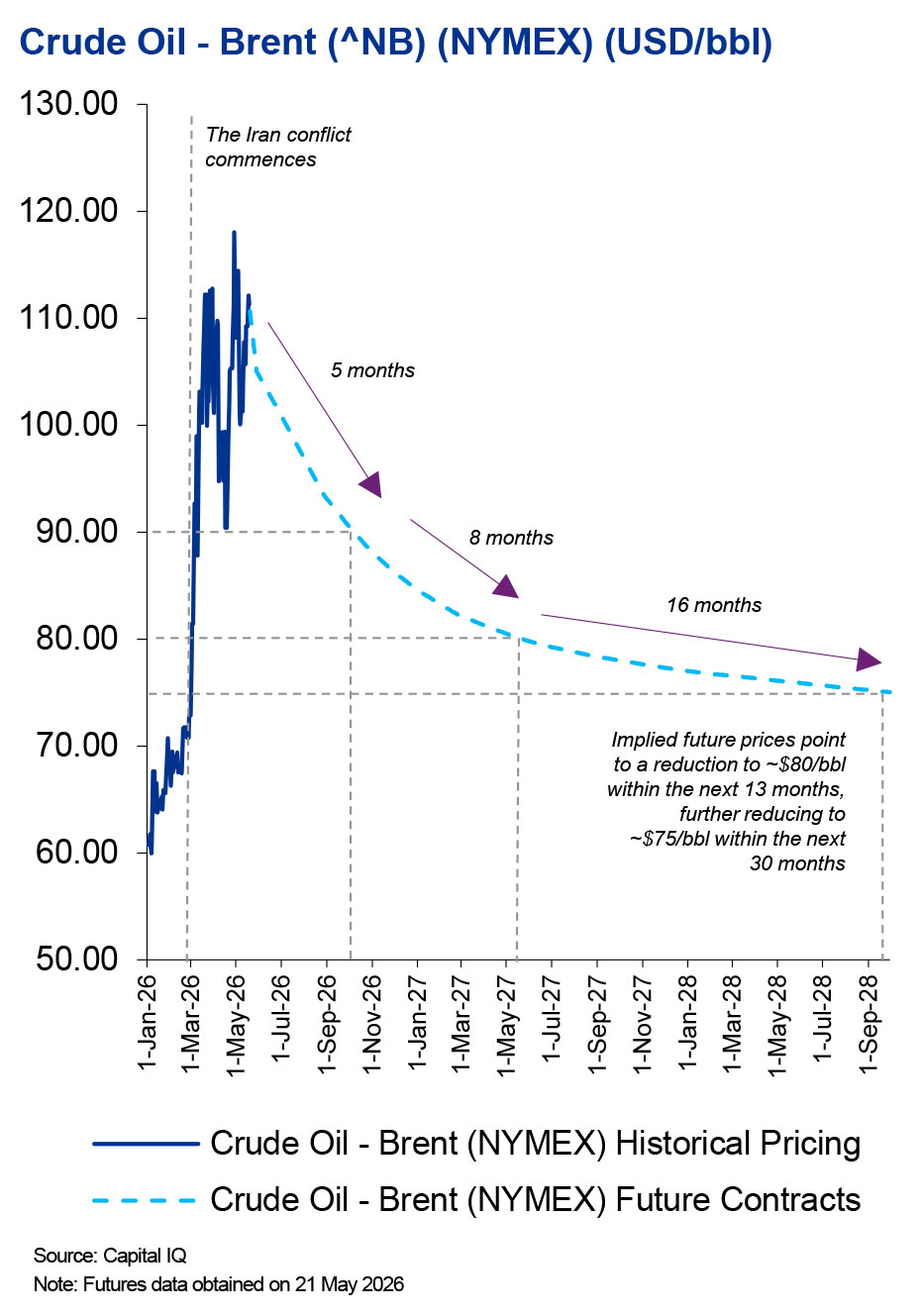

Brent future prices

> Click on the image to enlarge it

> Click on the image to enlarge it

Futures curve indicates an uncertainty‑led upward reset of crude prices by 2028: Futures prices spiked above USD 110/bbl, with an implied reduction to USD 90/bbl within first 5 months, 80/bbl within the next 8 months and USD 75/bbl within 16 months thereafter.

Recovery assumptions appear directionally aligned to market estimates: Recovery assumptions implicit within future prices appear to reflect market base‑case pricing under a sustained ceasefire. However, any further escalation would delay normalisation, with risk premia unwinding more gradually and extending price and earnings impacts beyond current expectations.

KPMG Deal Advisory

"KPMG provides a full range of valuation services for all sell-side, buy-side, tax restructuring, fund raising, and joint venture transactions."

Capital market and business valuation insights - May 2026

Special edition from Deal Advisory services, KPMG in Thailand

Key contacts

- Ian Thornhill

- Canopus Safdar

- Surayos Chuepanich

- Boonyaporn Donnapee

- Theraphol Saikaew

- Dominic Kobel

- Worachit Sirikajornkij

- Ming Ern Chew