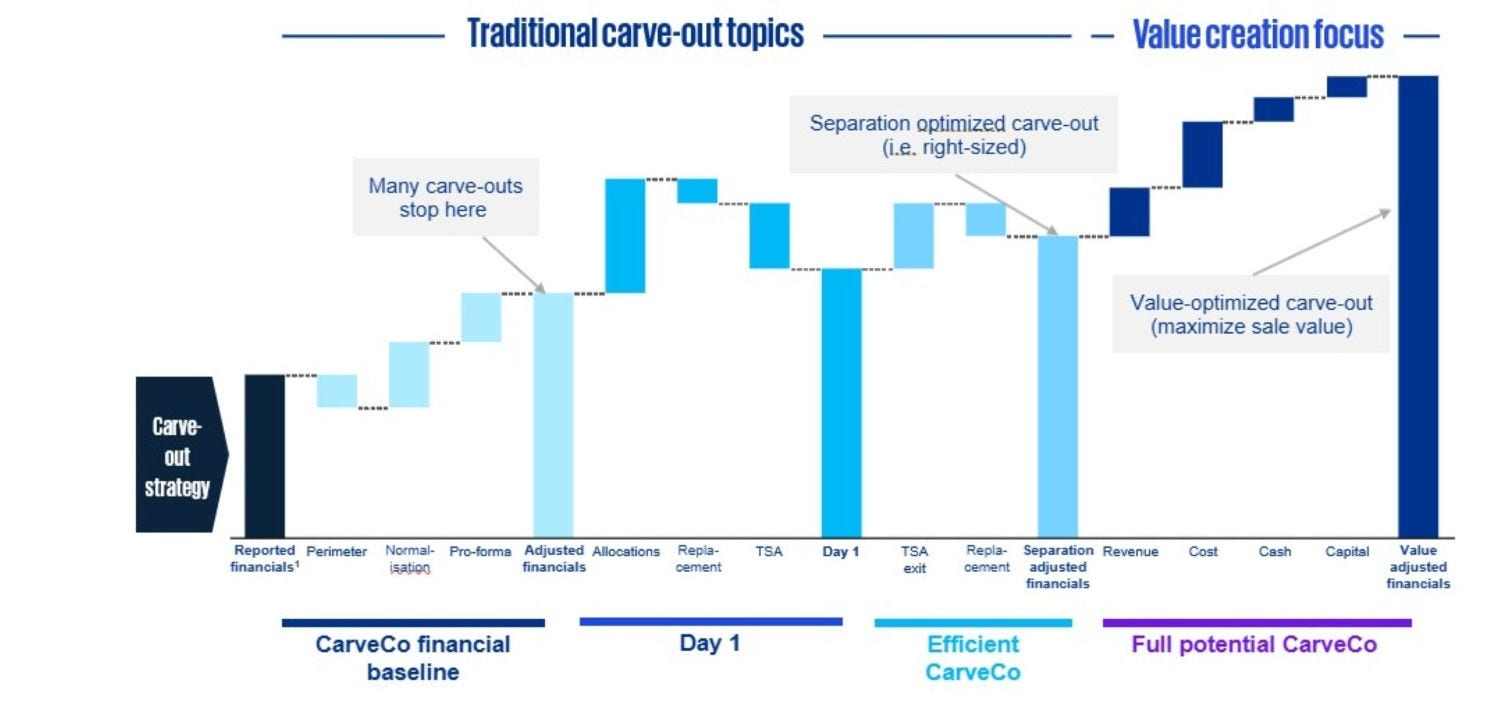

Many sellers continue to approach carve-outs as a clean-up exercise rather than a strategic value creation opportunity – ultimately leaving significant value on the table. At the same time, buyers are unlikely to price in upside that is not clearly articulated and evidenced by the vendor. In this article, our deals leaders explain how to present a credible full-potential CarveCo – and critically how to translate this into value buyers are willing to actually pay.

UK companies increasingly see carve outs as a great way to release capital to reinvest into the business or to return to shareholders (to find out why, read our first article in this series). Yet, for some reason, few sellers tend to take the opportunity to put their assets in the best light when preparing for a carve out. And that means they are underselling the equity story.

At the same time, buyers don’t just take what a seller tells them at face value. They want to see credible numbers, presented clearly and transparently that reflect the true value of the asset. That means providing three key proofs: a financial baseline for the CarveCo reflective of the separated business, a credible upside plan and a realistic cost to get there.

Sophisticated sellers who are targeting strategic buyers get ahead by developing sell-side synergies upfront (i.e. the potential synergy value that potential bidders may be able to realise from the acquisition and subsequent integration of the asset). This enables them to be on the front foot for maximising value from the transaction – including not only deal negotiations (e.g. ensuring that at least some of the bidder’s expected synergy value is also reflected within bids) but even using synergy value as a lens to help identify the most attractive bidders in the first place.

Finally, whilst not for the buyer, do not lose sight of the impact on the parent company. A sharp CarveCo story will mean little if it leaves behind significant stranded costs. Specifically for a listed business, execution could matter as much as price where your stated corporate strategy includes divestments. Markets will reward clean, credible delivery of divestments, even if it means accepting a lower headline valuation.