Yael Selfin, Chief Economist at KPMG UK, said: “The UK and Europe are once again confronting a major energy-related shock, but the nature of this crisis differs materially from the start of the 2022.

“Direct gas exposure is lower than during the Russia-Ukraine energy crisis, reducing the risk of physical shortages. However, the broader impact on global commodities and supply chains means the economic effects could prove more widespread.”

Broader commodity disruption creates new supply chain risks

The outlook across Europe remains highly dependent on the duration and severity of the disruption. A relatively quick reopening of the Strait later this summer could limit broader economic damage.

Elevated transportation costs and higher input costs including fertilizers could continue to feed through into inflation into 2027, keeping inflation potentially higher for longer. Disruptions to other commodities such as aluminium and helium are already feeding into industrial supply chains, creating additional pressures for sectors including automotive manufacturing, semiconductors and defence production.

Potential constraints in jet fuel supply also pose downside risks to Europe’s tourism sector during the peak summer season. Tourism-dependent economies such as Croatia, Portugal and Greece could be particularly exposed should travel disruptions or weaker booking demand materialise.

Yael added: “The breadth of the commodities affected makes this shock potentially more pervasive than the one experienced in 2022. Supply chain disruption now extends well beyond energy itself, affecting industrial and agriculture production as well as tourism activity across Europe.”

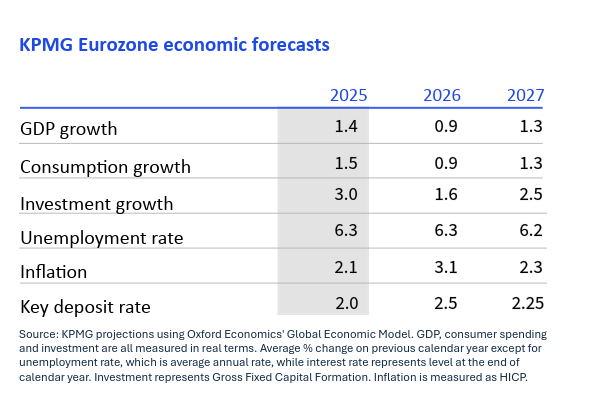

Inflation expected to rise again across Europe

Eurozone inflation is forecast to average 3.1% in 2026, driven primarily by rising energy prices and transportation costs. Fuel prices have already increased sharply since the onset of the conflict, with indirect price pressures expected to broaden the inflationary impact beyond energy components over the coming months.

The inflationary effects are likely to vary considerably across countries depending on energy exposure and electricity market structures. Economies more reliant on gas, including Italy and Ireland, may experience stronger inflationary pressures, while countries such as Spain and Switzerland are expected to see more limited pass-through effects due to lower dependence on gas.

Consumer spending to remain key driver of growth

Despite the renewed squeeze on household purchasing power, consumer spending is still expected to remain the primary driver of European growth.

Although rising energy prices are weighing on real incomes and consumer confidence has deteriorated sharply, labour markets across much of Europe remain resilient by historical standards. Continued resilience in some European labour markets is expected to help cushion the impact on household spending.

European central banks face difficult balancing act

The European Central Bank is expected to adopt a more hawkish stance, with policymakers signalling that interest rate increases could begin as early as June should inflationary pressures persist.

There is a possibility that the Bank of England may follow a similar path, with a first hike as early as July. Despite a weaker labour market, the risk of a resurgence in domestic price pressures in the UK is still high.