Key findings

- Temp billings expand slightly for the first time in three months

- Candidate availability increases at softest rate in a year

- Stronger rises in both starting salaries and temp wages

Data collected 12-26 January

Key findings

Data collected 12-26 January

Summary

The first KPMG and REC, UK Report on Jobs survey for 2026 pointed to a relative improvement in hiring conditions in January. Recruiters signalled a softer drop in permanent staff appointments along with a fresh increase in temp billings. However, subdued overall market confidence and squeezed client budgets continued to dampen overall staff recruitment. Consequently, vacancies continued to decline, albeit at a slower pace than seen at the end of 2025.

The upturn in candidate availability meanwhile lost pace in January. Whilst sharp, the latest increase in staff supply was the slowest recorded in a year. At the same time, both starting salaries and temp wages increased at steeper rates amid greater competition for in-demand skills.

The report is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 UK recruitment and employment consultancies.

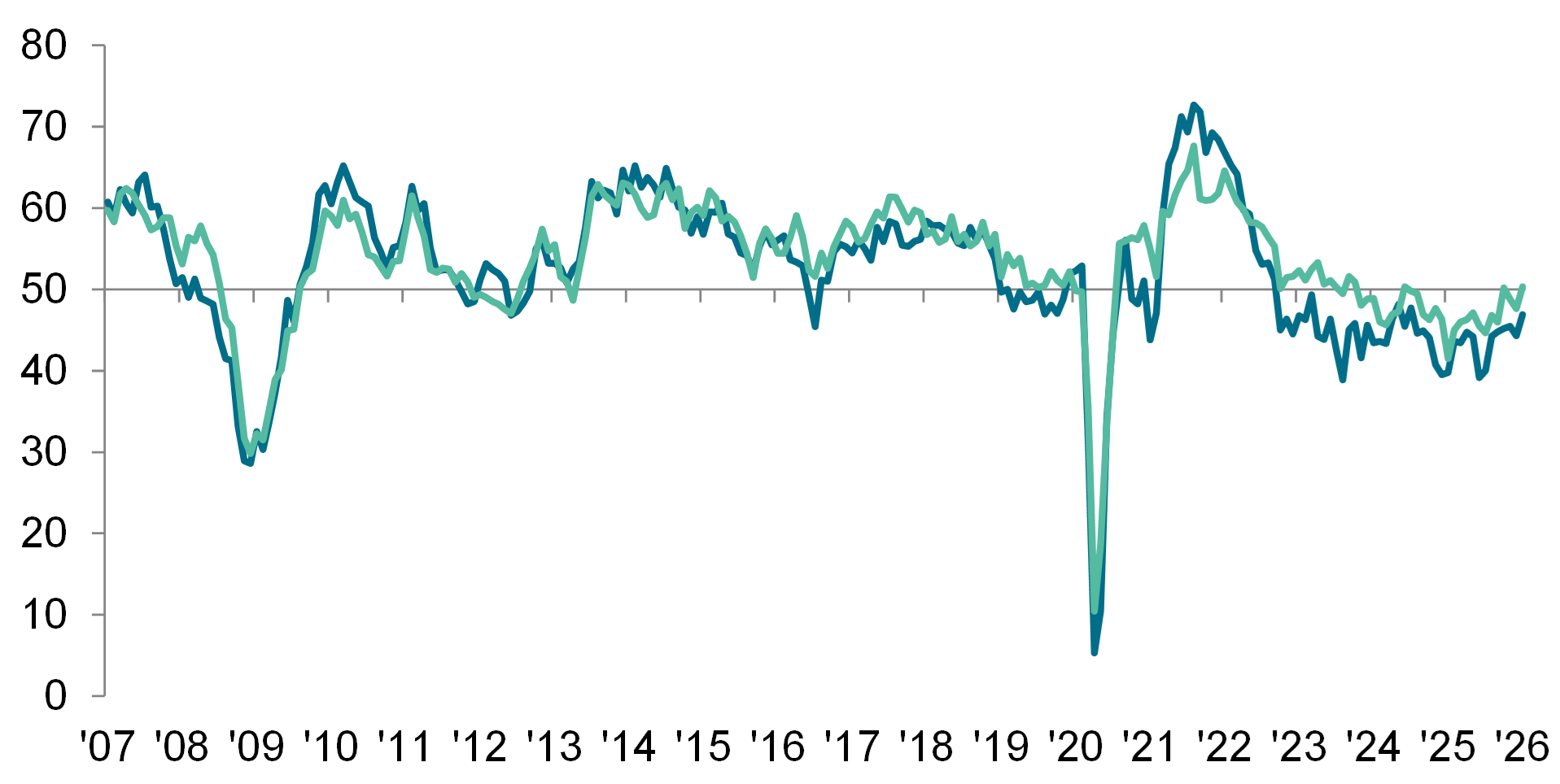

Downturn in permanent staff hiring eases

UK recruitment companies signalled a further decline in permanent placements in January amid reports of generally weak market conditions and employer concerns over costs. That said, the pace of reduction eased to the weakest in 18 months. Some companies reportedly pressed ahead with recruitment plans as a degree of market uncertainty had lifted following the government Budget announcement. At the same time, temp billings rose for only the second time since May 2024, though growth was marginal.

Permanent Placements Index (blue)

Temporary Billings Index (green)

50.0 = no-change

Sources: KPMG, REC, S&P Global PMI.

Softest rise in candidate availability for a year

The supply of candidates continued to rise at the start of 2026, which was frequently linked to redundancies as well as fewer job opportunities. However, the rate of expansion was the softest seen in 12 months. This was predominantly driven by a slowdown in growth of permanent candidate numbers, though temp candidate availability also improved at a weaker pace.

Pay trends improve for both permanent and temporary staff

Competition for skills that were often in short supply reportedly added further upwards pressure on rates of starting pay in January. Notably, starting salaries increased at a solid pace that was the quickest for nearly a year-and-a-half, while temp wage inflation hit the joint-highest since May 2024.

Demand for staff declines at slower but still sharp rate

Overall vacancies across the UK continued to decrease at the start of the year. The rate of reduction remained sharp, despite easing to the second-slowest seen over the past seven months. Demand for permanent staff contracted at a slightly softer pace than in December, but one that remained quicker than for temporary workers.

Regional and Sector Variations

Permanent placements fell at a notably softer pace in the North of England, and was slower than those seen in London and the South. The Midlands meanwhile recorded further marginal growth.

Temp billings rose sharply in the Midlands and increased for the first time in two years in the South of England. Meanwhile, a steep reduction was once again seen in the North of England, while London recorded a softer, but nevertheless solid decline.

Permanent staff vacancies declined across all ten monitored job categories at the start of the year. The sharpest reduction was seen across the Nursing/Medical/Care sector, while the softest fall was recorded across the Engineering category.

Blue Collar was the only employment category to register an increase in temporary staff demand in January, though the rate of growth was marginal. Meanwhile, Nursing/Medical/Care and Retail recorded the steepest falls in temporary job opportunities.

Comments

Commenting on the latest survey results, Lisa Fernihough, Head of Advisory at KPMG UK said:

“After a difficult end to last year, it’s encouraging to start this year with tentative signs that hiring appetites are beginning to improve as chief execs respond to signs of easing uncertainty by starting to push forward with their plans.

“Skills shortages in specialist areas continue to impact the market, particularly where competition for talent remains intense. There are parts of the economy poised for investment, and as skills needs align with greater market stability, we could start to see more consistent improvement in hiring as the year progresses.”

Neil Carberry, REC Chief Executive, said:

“There have been increasing signs from businesses as we enter 2026 that uncertainty on hiring plans is giving way to action. That does not mean a general hiring upswing, but the “wait-and-see” period seems to be ending. Rising temp billings and a levelling off in the permanent market speak to these clearer plans. REC members across the country report a change in tone since the start of the year.

“The decisions firms are now making involve lots of trade-offs, such as whether to create jobs in the UK or elsewhere, or which jobs need the human touch as opposed to an automated solution. A growing, inclusive economy requires high levels of employment – a focus on encouraging firms to create jobs rather than discouraging that investment is more important than ever. So far, the Government has struggled to convince businesses it wants them to hire. That has to change in the decisions that are made this year if we are to avoid a continued rise in unemployment.”

Comments

Commenting on the latest survey results, Jon Holt, Group Chief Executive and UK Senior Partner KPMG, said:

“The jobs market at the end of 2025 was still signalling caution. After a long stretch of rising cost pressures and higher global economic uncertainty, many firms continue to pause hiring and are flexing where they can by using temporary staff.

“As we head into the New Year, this restraint is likely to remain in the near term. Chief execs who have been prioritising increased investment in tech to improve resilience and productivity, will be looking for signs of greater confidence in the wider economy before turning the hiring taps back on.”

Neil Carberry, REC Chief Executive, said:

“It’s always difficult to draw conclusions from jobs data in December, but the fact that the market slipped back a little on November is a reminder of the pressure employers are under. Nevertheless, the second half of 2025 showed some signs of a long run of negative data softening, and with placements falling at a slower pace than the 2025 average in December there is some hope that we are seeing a December dip, rather than a change in the trend. There is certainly a wider range of experience now, with recruitment in the Midlands growing for both temp and perm roles last month. Activity kicked off this month is what will really tell us if the tide is turning.

“Making this a better year for hiring will require a focus on building business confidence to invest. With the Budget behind us, the government needs to set out a clear path that firms can believe in, from the industrial strategy to pragmatic approaches on the Employment Rights Act, which is worrying many firms.”

-ENDS-

Contact:

KPMG

Claire Barratt

Deputy Head of Media Relations

T:+44 (0)7923 439264

claire.barratt@kpmg.co.uk

REC

Hamant Verma

Communications Manager

T: +44 (0)20 7009 2129

hamant.verma@rec.uk.com

S&P Global

Annabel Fiddes

Economics Associate Director

S&P Global Market Intelligence

T: +44 (0)1491 461 010

annabel.fiddes@spglobal.com

Hannah Brook

EMEA Communications Manager

S&P Global Market Intelligence

T: +44-7483-439-812

hannah.brook@spglobal.com

press.mi@spglobal.com

Methodology

The KPMG and REC, UK Report on Jobs is compiled by S&P Global from responses to questionnaires sent to a panel of around 400 UK recruitment and employment consultancies.

Survey responses are collected in the second half of each month and indicate the direction of change compared to the previous month. A diffusion index is calculated for each survey variable. The index is the sum of the percentage of ‘higher’ responses and half the percentage of ‘unchanged’ responses. The indices vary between 0 and 100, with a reading above 50 indicating an overall increase compared to the previous month, and below 50 an overall decrease. The indices are then seasonally adjusted.

Underlying survey data are not revised after publication, but seasonal adjustment factors may be revised from time to time as appropriate which will affect the seasonally adjusted data series.

For further information on the survey methodology, please contact economics@spglobal.com.

Full reports and historical data from the KPMG and REC, UK Report on Jobs are available by subscription. Please contact economics@spglobal.com.

About KPMG in the UK

KPMG is trusted to make the difference for our clients, people and the communities we work in. With our people’s deep sector expertise and cutting-edge technology, we help organisations overcome their biggest challenges and unlock new opportunities to transform and grow.

On 1 October 2024, KPMG UK and KPMG Switzerland merged to form KPMG UK/Swiss Group, scaling our strengths and amplifying the difference we make.

KPMG International Limited is a global organisation of independent professional services firms providing Audit, Tax and Advisory services in 138 countries and territories. Each KPMG firm is a legally distinct and separate entity and describes itself as such.

About REC

The REC is the voice of the recruitment industry, speaking up for great recruiters. We drive standards and empower recruitment businesses to build better futures for their candidates and themselves. We are champions of an industry which is fundamental to the strength of the UK economy. Find out more about the Recruitment & Employment Confederation at www.rec.uk.com.

About S&P Global

S&P Global (NYSE: SPGI) S&P Global provides essential intelligence. We enable governments, businesses and individuals with the right data, expertise and connected technology so that they can make decisions with conviction. From helping our customers assess new investments to guiding them through ESG and energy transition across supply chains, we unlock new opportunities, solve challenges and accelerate progress for the world.

We are widely sought after by many of the world’s leading organisations to provide credit ratings, benchmarks, analytics and workflow solutions in the global capital, commodity and automotive markets. With every one of our offerings, we help the world’s leading organisations plan for tomorrow, today. www.spglobal.com.

Disclaimer

The intellectual property rights to the data provided herein are owned by or licensed to S&P Global and/or its affiliates. Any unauthorised use, including but not limited to copying, distributing, transmitting or otherwise of any data appearing is not permitted without S&P Global’s prior consent. S&P Global shall not have any liability, duty or obligation for or relating to the content or information (“Data”) contained herein, any errors, inaccuracies, omissions or delays in the data, or for any actions taken in reliance thereon. In no event shall S&P Global be liable for any special, incidental, or consequential damages, arising out of the use of the Data.

This Content was published by S&P Global Market Intelligence and not by S&P Global Ratings, which is a separately managed division of S&P Global. Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content.