Investment outlook supported by energy transition and digital infrastructure

While UK business investment has underperformed international peers since 2016, recent growth has been driven by two areas, the energy sector and information and communication, supported by renewable capacity expansion and demand for AI-enabled data infrastructure.

Investment outside these sectors remains subdued, raising the risk of a K-shaped recovery in which gains remain concentrated rather than economy-wide. However, policy reforms to planning, energy systems and skills could broaden the investment uplift.

Growth strengthens in 2027

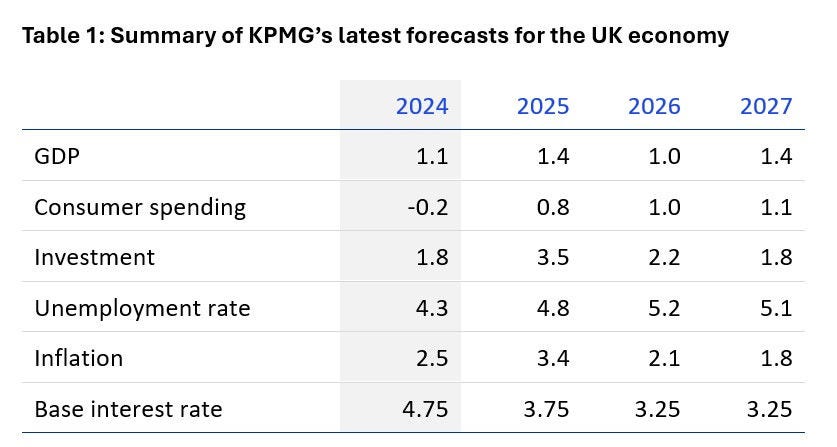

GDP growth is forecast to improve to 1.4% in 2027 as investment momentum strengthens, public infrastructure projects scale up and planning reform begins to feed into housing supply.

External demand is expected to offer limited support to the UK economy in 2026, with a slowing US economy and higher tariffs weighing on exports, while trade diversions boost imports, leaving net trade broadly flat.

Monetary Policy: more rate cuts to come

A more benign inflation outlook and greater fiscal clarity will strengthen the case for continued monetary easing. The Bank of England is expected to cut rates once more in December 2025, to 3.75%, before slowing the pace of reductions in 2026 where they are likely to settle at 3.25%.

However, UK borrowing costs are expected to remain high relative to other advanced economies unless fiscal credibility is strengthened and long-term spending pressures addressed.

Headline inflation is forecast to continue easing over the coming year, helped by the measures in the Autumn Budget, which will see household energy bills fall from April 2026, alongside, Improving global food trends and softer domestic demand. Inflation is expected to return to the Bank’s 2% target by Spring 2026, although persistent wage pressures mean core inflation is likely to fall more slowly.