On 25 February 2026 the Department for Business and Trade (DBT) published the UK SRS:

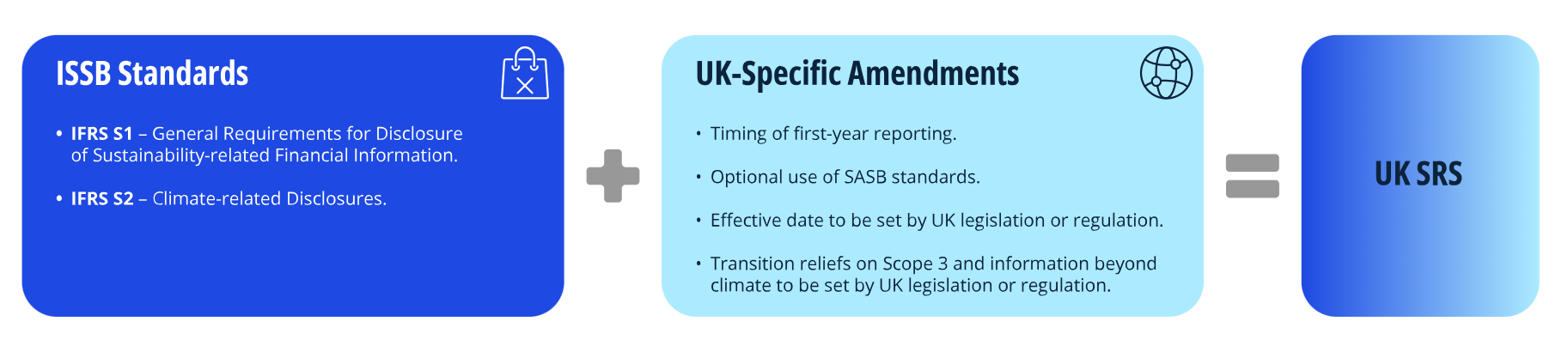

- UK SRS S1: General requirements for disclosure of sustainability-related financial information; and

- UK SRS S2: Climate-related disclosures.

The publication of these standards follows the public consultation that the DBT conducted, which closed on 17 September 2025.

These two standards are based on the inaugural two standards published by the International Sustainability Standards Board (ISSB) in June 2023, and revised in December 2025 (Amendments to clarify IFRS S2):

- IFRS S1: General Requirements for Disclosure of Sustainability-related Financial Information; and

- IFRS S2: Climate-related Disclosures.

UK SRS S1 and S2 are currently available for all UK companies to use on a voluntary basis. The Financial Conduct Authority (FCA) is conducting a public consultation to determine how the UK SRS will be mandated for UK listed company reporting. See this article for further information on this consultation.