The current economic environment remains characterised by heightened uncertainty and structural change. Persistently elevated interest rates, inflation volatility, geopolitical tensions, cost of living pressures and emerging longer-term risks such as climate transition continue to influence traditional credit risk assumptions, driving greater complexity and judgement in IFRS 9 analysis. Against this backdrop, Expected Credit Loss (ECL) provisioning under IFRS 9 remains a critical mechanism for ensuring balance sheets appropriately reflect forward-looking credit risk.

Background

Introduction

KPMG helps banks keep their IFRS 9 frameworks (data and systems, economic scenarios, policies, models, overlays and governance) robust, proportionate and fit‑for‑purpose in a volatile risk environment. Our credit risk, modelling and climate specialists deliver targeted, end‑to‑end enhancements across Significant Increase in Credit Risk (SICR) and staging performance, macroeconomic scenarios, ECL model redevelopment, data and platform enablement, PMA governance, and controls and monitoring. We help firms enhance their models, incorporate emerging risks (including climate), improve audit and regulatory defensibility, and enable controlled adoption of ML/AI – supporting more stable outcomes, clearer governance and a credible path to unwinding overlays as uncertainties are resolved.

In Q1 2026, we launched a UK‑wide IFRS 9 benchmarking survey across banks, building societies and challenger institutions. The survey explored how firms are maintaining robust, proportionate and fit‑for‑purpose IFRS 9 frameworks in an evolving economic and risk environment. It examined current practices across key areas such as staging and SICR, macroeconomic scenarios, ECL modelling, management overlays, and data and governance, alongside emerging themes including climate risk and the use of AI and machine learning.

This report presents insights from the survey, highlighting where industry practices are converging and where material differences remain by firm type and portfolio mix. It also summarises common challenges and planned areas of enhancement, offering a forward-looking view of how firms expect their IFRS 9 frameworks to continue evolving in the coming years. We hope this analysis supports constructive discussion on the ongoing evolution of IFRS 9 and would welcome the opportunity to discuss it with you in more detail.

Current state of IFRS 9 ECL

IFRS 9 ECL modelling across the UK financial sector is now well developed and firmly embedded within core risk and capital frameworks. Following several years of implementation and refinement, most institutions operate stable, well understood models and apply broadly consistent approaches to staging, scenario design and expected credit loss estimation.

At the same time, there is recognition across the industry that further enhancement is both expected and ongoing. Data remains an important area of focus, particularly in relation to historical depth, transparency and traceability, which can influence model responsiveness and confidence in outputs. Management overlays continue to play a constructive role in addressing uncertainty, especially as firms navigate evolving economic and risk environments. Climate risk integration is also developing, with large banks progressing through overlays, parameter adjustments and linkages to Climate Scenario Analysis, while many building societies and challenger banks continue to treat climate impacts as outside IFRS 9 or as not yet material.

Adoption of AI and ML techniques is currently advancing in a cautious and tightly governed manner, focused on selective use cases and efficiency gains, constrained by explainability, data quality and model risk management expectations.

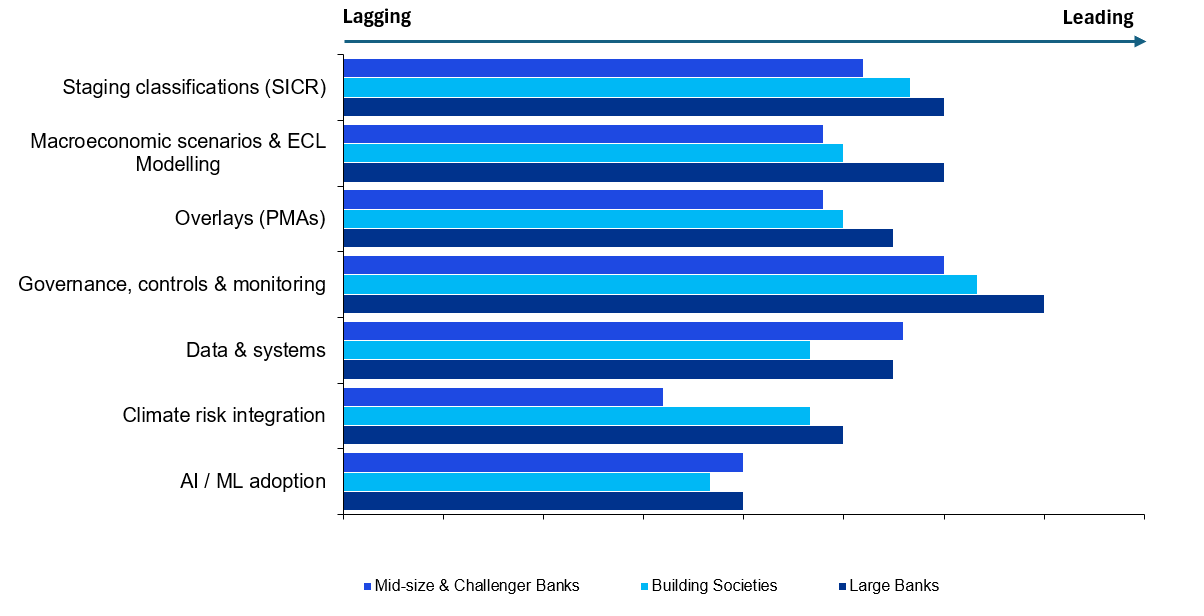

IFRS 9 ECL Maturity Model

The IFRS 9 ECL Maturity Model reflects KPMG’s qualitative view of current industry practices, informed by survey responses and KPMG’s wider experience working with UK-based firms. The assessment is judgement-led and does not rely on a prescriptive or quantitative methodology. Participating firms were assessed based on a scale representing an absolute benchmark, distinguishing between lagging and leading practices.

Descriptions of lagging and leading practices are provided in the table below.

Areas of focus

Firms are prioritising targeted refinements to mature IFRS 9 frameworks rather than wholesale transformation, with a strong focus on stability and defensibility of the ECL estimates and proportionality of the IFRS 9 framework factoring in the firm’s scale, complexity and risk profile.

Over the next planning horizon, firms expect modest but sustained investment focused on models, data and governance rather than major re‑architecture. Emerging areas such as GenAI for documentation, climate risk translation and controlled ML adoption are gaining traction but remain secondary to the core objective of having robust IFRS 9 ECL modelling approaches.

For more information, please reach out to: Steven Hall, Andrew Fulton, Charlotte Lo, James Philpott, Ayan Haldar or Himanshu Bagga.

Get in touch

KPMG in the UK is dedicated to supporting clients by providing insights and leading practices that can drive success in the industry. By staying at the forefront of industry trends and regulatory changes, KPMG can support firms to navigate complexity and capitalise on new opportunities. Please do reach out if you’d like to hear more about the survey or discuss the latest trends in IFRS 9 ECL modelling.

Our regulatory insights

Something went wrong

Oops!! Something went wrong, please try again

Get in touch

Discover why organisations across the UK trust KPMG to make the difference and how we can help you to do the same.