Pay rates improve in April

Pay rates picked up during April as firms remained willing to raise wages to attract suitable candidates. Latest data signalled that pay has now increased for both permanent and temporary staff for 38 months in a row. For permanent workers, the rate of growth accelerated to its highest in the year-to-date, though remained below its historical survey trend. Temporary staff saw their pay rates rise at the steepest pace since June 2023 and to a degree that was slightly above average.

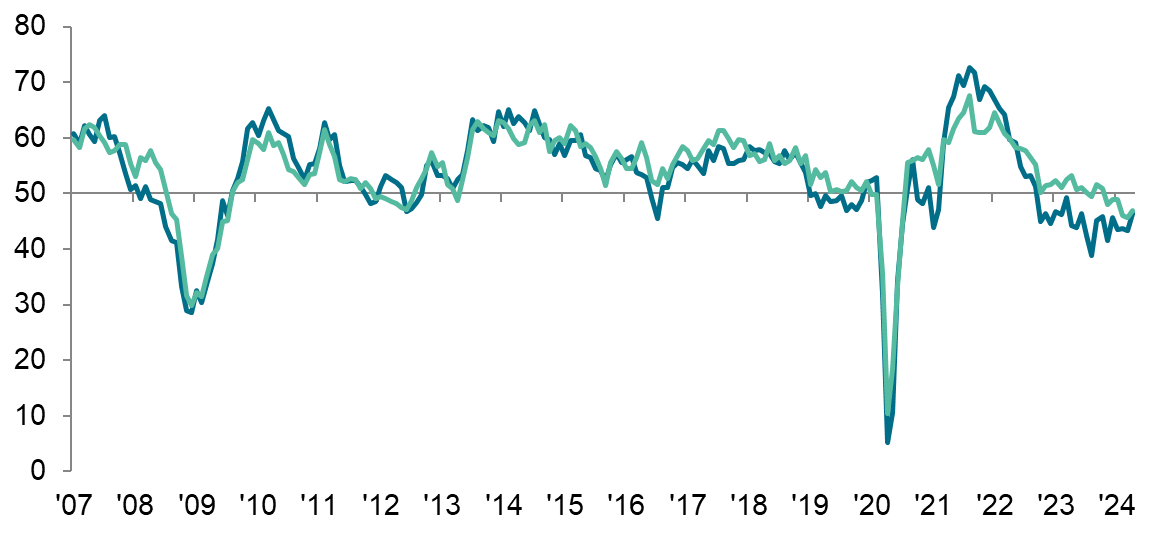

Slower falls in staff demand signalled

April’s survey data showed that overall demand for staff continued to fall, extending the current downturn to six months. That said, the rate of contraction was modest and the slowest since January. Temp staff demand was down only marginally and to a slower degree than for permanent workers.

Fastest increase in staff availability since last November

Candidate availability continued to rise during April, with the rate of growth for all staff hitting its best for five months. Panellists noted a higher number of redundancies, whilst also signalling a general increase in the number of people looking for work. Rates of growth in candidate availability were similarly strong for both permanent and temporary staff.

Regional and Sector Variations

As has been the case throughout the year so far, permanent candidate numbers declined across all English regions during April. The steepest reduction was again found in the South of England.

Of the three English regions that recorded a decline in temp billings, by far the steepest cut was seen in London. The Midlands bucked the broader trend, registering modest growth during April.

Led by the Retail category, April saw seven out of ten broad sectors covered by the survey register a drop in demand for permanent staff. Of the three sectors where growth was registered, the strongest rise was for Engineering.

For temporary vacancies, half of the sectors covered recorded a fall in demand during April, with retail registering by far the steepest contraction. Of the five categories that saw growth, the strongest increase was seen for Blue Collar, followed by Engineering.

Comments

Commenting on the latest survey results, Jon Holt, Chief Executive and Senior Partner of KPMG in the UK, said:

“UK CEOs continue to grapple with the Bank’s hawkish stance on interest rates, and will no doubt hope April’s survey data is another marker in the sand on the journey towards a summer cut.

“While there are still complexities, like pay rates improving due in part to last month’s 9.8% rise in the National Living Wage, overall pressure is easing on the labour market. Ongoing weak demand is driving the steady decline in permanent staff appointments month on month, and we’ve seen a sharp uptick in candidate availability.

“Business leaders see this cooling, combined with weakening inflationary pressure, as indicators for the Bank to hopefully shift to a more dovish position. Companies would then have the confidence and certainty to press go on their investment strategies.”

Neil Carberry, REC Chief Executive, said:

“The critical moment in any labour market slowdown is the point at which demand starts to turn around. Today’s hiring data suggests that point is close, with fewer recruitment firms reporting a drop in demand. While the trend is still gently down, the pace of decline in permanent hiring is the slowest in ten months. Temporary hiring, which has had much less of a decline overall, also scored better than last month. Firms have told us all year that they will be willing to hire and invest in their business when confidence returns to the wider economy – and there is a glimmer of lower inflation and the prospect of lower interest rates starting to drive that now.

“Pay continues to rise, with a slight bump up this month likely to have been driven by the April peak in employer pay rises and the recent Minimum Wage rise. With substantial wage rises attracting people to work, and low unemployment, businesses and government alike will need new approaches to developing and engaging our labour force – alongside new technology – if the UK is going to grow in the way it needs to.

“Our flexible labour market is at the heart of this. It is one of the big success stories of the UK economy, with millions of workers and companies building their futures in ways that would not be possible in the one-size-fits-all approach of the past. It’s why, for instance, nurses choose to work via agencies so they can get control over their working lives. Any government needs to work hard to understand what workers and companies need now – a more nuanced debate than is often centre stage in Whitehall and Westminster. A partnership approach with businesses is essential.”

Contact