For the first time, KPMG conducted an in-depth analysis of tender offers covering the Central and Eastern Europe (CEE) region. The analysis is based on tender offers announced between 2016 and 2025 and reflects KPMG’s continued commitment to delivering robust, data‑driven insights that support informed decision‑making by investors, corporate executives, and other market stakeholders.

Key figures for 2016–2025

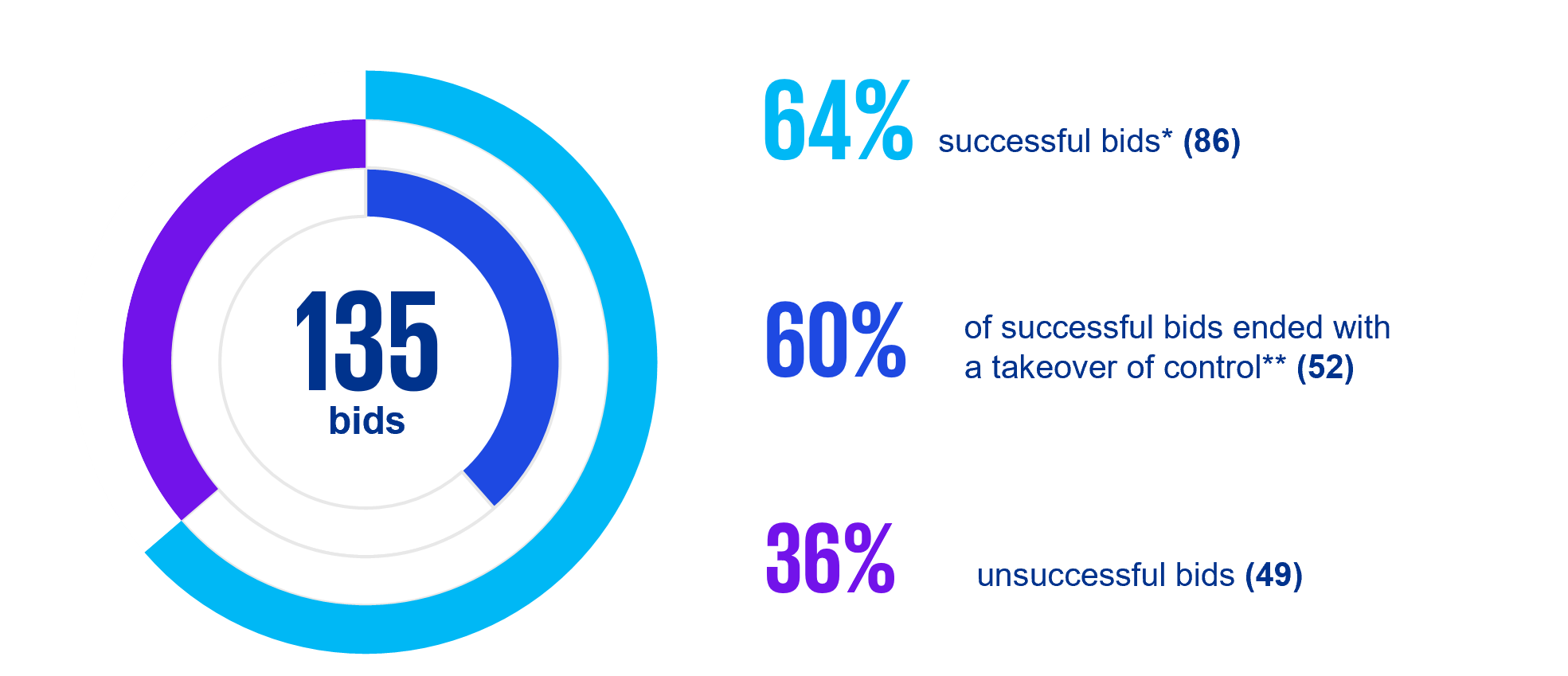

74%

Percentage of successful tender offers* (2025: 58%)

EUR 139m

Arithmetic average of successful tender offers in which the investor's intention was to acquire control of the company

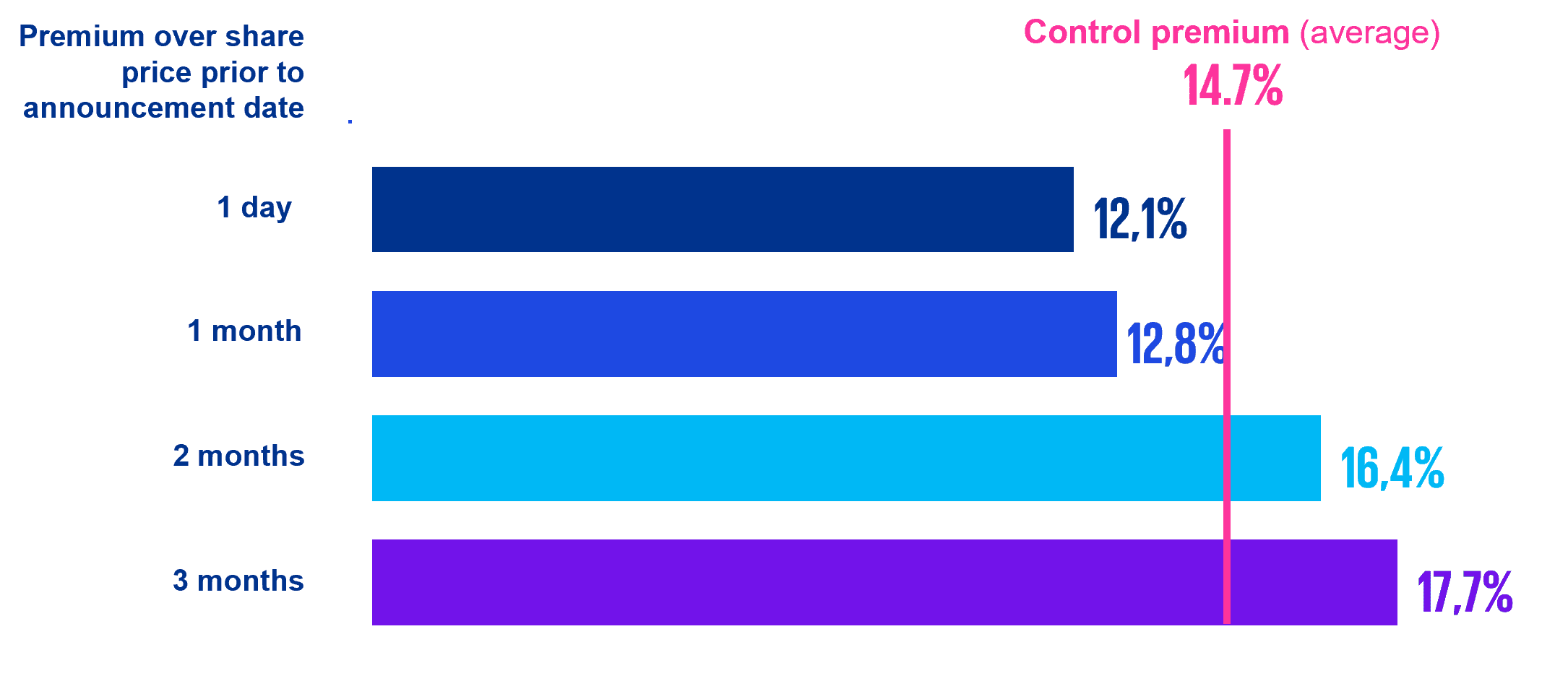

14.7%

Control premium based on an examination of the tender offers market in the CEE region during the period analysed

366

successful tender offers (excluding buybacks) for shares of the CEE region listed companies (2025: 15)

135

bids in which the investor's intent was to take control of the company (2025: 10)

*All tender offers that resulted in an acquisition of shares

What is a control premium?

Control premium is the excess over the pro-rata fair value of the equity interest in the business that a bidder is willing to pay to own a controlling stake in the acquired company.

Owning a controlling interest (without 100% ownership) in a company can bring additional benefits, including an ability to:

For comparative purposes, the report benchmarks control premiums observed in the CEE region against those recorded across six major global regions.

„KPMG CEE has been monitoring control premiums in tender offers announced on the Warsaw Stock Exchange for more than two decades. In this report, KPMG CEE presents - for the first time - the results of an extended analysis covering the Central and Eastern Europe (CEE) region. By broadening the geographical scope beyond a single market, the study offers a regional perspective on control premiums, enabling a more comprehensive assessment of similarities, differences, and underlying trends across CEE capital markets.

Control premiums in the CEE region are slightly lower than those observed in emerging markets, and materially lower than premiums recorded across all developed markets. Overall, the analysis confirms a clear structural trend: higher levels of capital-market development are generally associated with higher control premiums.”

Tomasz Wiśniewski

Partner, Chief Operating Officer, Head of Valuations Team in Poland & CEE

KPMG in Poland

Methodology

The calculation of the control premium is based on an analysis of successful takeover bids in which the acquirer’s stated intention was to obtain control of the target company.

For each transaction, the control premium is calculated as the median of the percentage differences between the price paid for the tendered shares and the target company’s share prices observed over a defined pre‑announcement period. To mitigate the impact of short‑term price volatility and outliers, four distinct share‑price observations prior to the tender offer announcement date are applied in the analysis.

For each target company, four individual medians are calculated based on these observations. The arithmetic mean of these medians represents the final control premium used in the analysis.

Analysis results

Structure of takeover bids in 2016-2025

*All tender offers that resulted in an acquisition of shares

** Not all bids have been included in the control premium analysis

KPMG study on tender offers for shares of WSE-listed companies in CEE

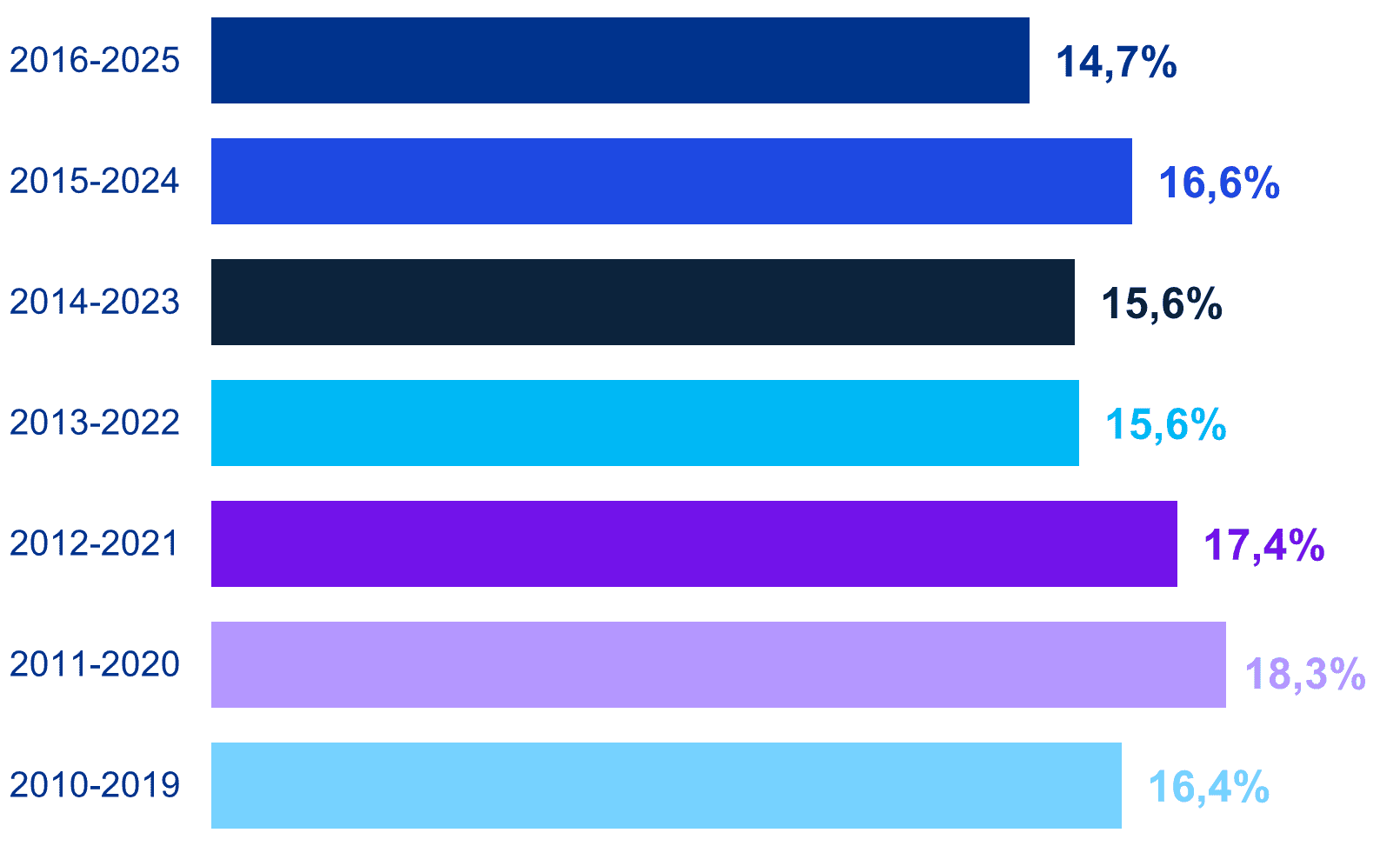

Control premium in historical perspective

Control premiums by decade

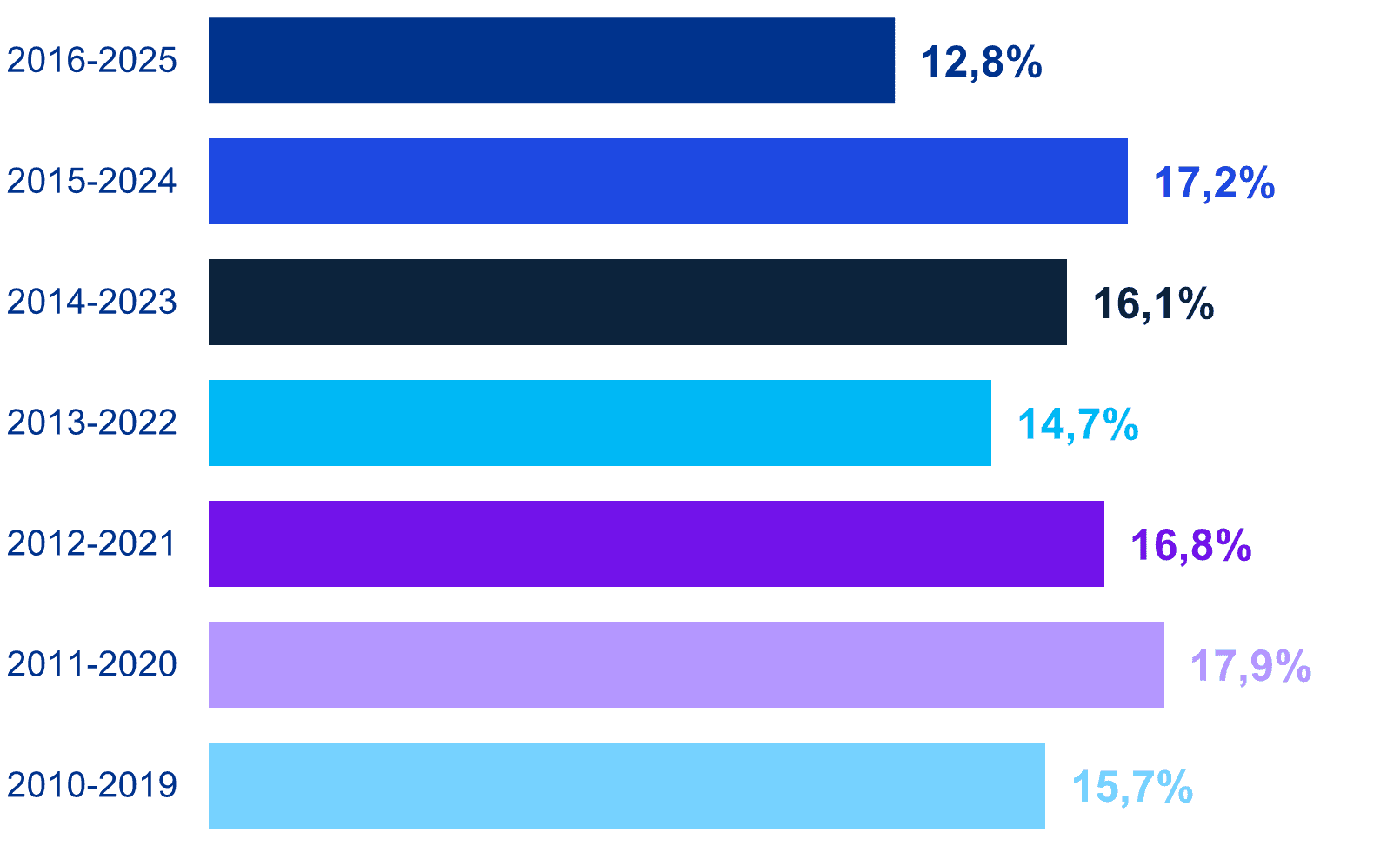

Premium over target company’s share price 1 month prior

to the announcement date

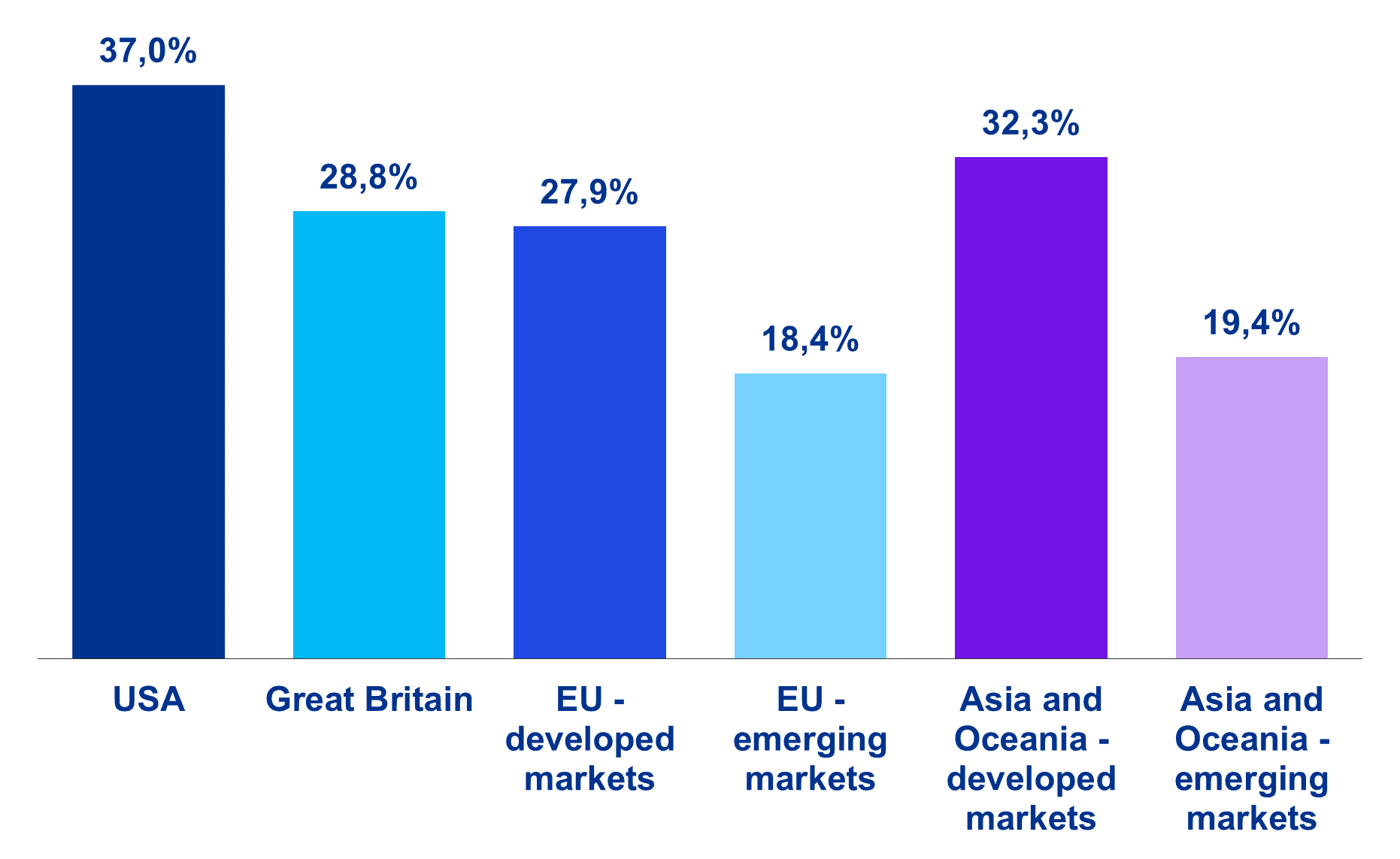

Control premiums globally

Along with the analysis of control premiums observed in the CEE region, the results with premiums offered in other capital markets were also compared. Regional control premiums were calculated on a cumulative basis using takeover bids announced between 2005 and 2025.

The results indicate that, over the period analysed, control premiums in the CEE region remain lower than those observed in all developed markets included in the study. Among these, the United States continues to exhibit the highest control premium levels, reflecting market‑specific factors such as depth, liquidity, and competitive dynamics in takeover transactions.

Regional control premiums in 2005-2025

To ensure consistency and comparability across geographies, a simplified and standardised calculation approach was applied. Unlike the more granular, market‑specific analysis of control premiums for CEE presented in earlier sections of this report, this regional comparison is based on premiums measured relative to the share price one month prior to the tender offer announcement date. This approach is widely applied in academic research and international comparative studies on control premiums.

Applying this methodology resulted in an estimated control premium of 15.4% for the CEE region. The difference compared with KPMG’s estimate of 14.7% reflects variations in data selection methodologies, in particular the use of the S&P Capital IQ database versus KPMG’s proprietary research and adjustments.

Download the report

Contact us

Learn more about how KPMG's knowledge and technology can help you and your business.

Our experts

Tomasz Wiśniewski

Partner, Chief Operating Officer, Head of Valuations Team in Poland & CEE

KPMG in Poland

Newsletter

Want to receive the latest business updates? Subscribe to our newsletter.