Introduction:

The following article is the second in a series of excerpts from KPMG’s 2024 West Africa Banking Industry Survey Report, highlighting banking customer behavior and expectations across retail, corporate, and SME industry segments. This article explores the nuances of Ghanaian banking customer behaviors and preferences when interacting with their banks’ digital platforms.

Consumers in Ghana are modifying their behaviours and digital preferences in line with changes in the broader economic landscape and advancement in technology. In this digital era, consumers hold significant bargaining power due to the wealth of readily accessible information at their fingertips. It was not surprising that, in this year’s survey, customers indicated product/service reviews, brand affinity and research as the top three factors influencing their purchasing decisions. This highlights a shift toward more discerning consumers who value transparency, trustworthiness and credible information.

Digital adoption continues to rise steadily – early in 2024, Ghana’s internet penetration and mobile connectivity rates stood at 70% and 113% respectively.1 This widespread connectivity has driven the growth of e-commerce, digital banking, and social media marketing, influencing how Ghanaians discover, evaluate and purchase products and services.

Sixty-two percent of respondents reported an increase in spending on airtime and data highlighting the growing reliance on digital connectivity. Customers indicated that their online activities primarily revolve around the usage of instant messaging apps such as WhatsApp, social media platforms such as X (formerly Twitter) and streaming movies.

The survey also revealed the extent to which digital consumption habits are evolving. With attention spans becoming shorter, 24% of respondents admitted to glancing at their phones every 10 to 15 minutes, highlighting the constant need for connectivity and engagement.

Globally, attention spans are shrinking, and this was evidenced in our survey as 52% of respondents indicated that shortform content such as Instagram reels and TikTok videos capture their attention

the most. This shift toward bite-sized, visually appealing content reflects the changing preferences of digital consumers and emphasises the need for businesses to create concise, high-quality, and visually compelling content that resonates with their audiences.

While internet usage has increased, we observed that consumers have become more conscious of the credibility of information available online. This growing awareness of misinformation is reflected in the fact that three in ten respondents remain neutral about their trust in online information. This neutrality suggests that while consumers recognise the value of the internet, they are also increasingly sceptical about the reliability of the content they encounter. To address this, businesses must provide verified, fact-based information and actively work to combat misinformation. Doing so not only strengthens consumer trust but also reinforces the brand’s integrity. This sentiment was echoed by customers, as one in every four respondents emphasised that excellent customer experience means being trustworthy, transparent and delivering on promises. Brands that establish themselves as trustworthy stand a better chance of improving customer loyalty and advocacy

Channel Usage

The payments system in Ghana continues to evolve driven by strengthened regulatory oversight, advances in AI/ machine learning and changing customer preferences. Customers are increasingly demanding more reliable, secure, faster, and efficient payment platforms. This year, quality of digital

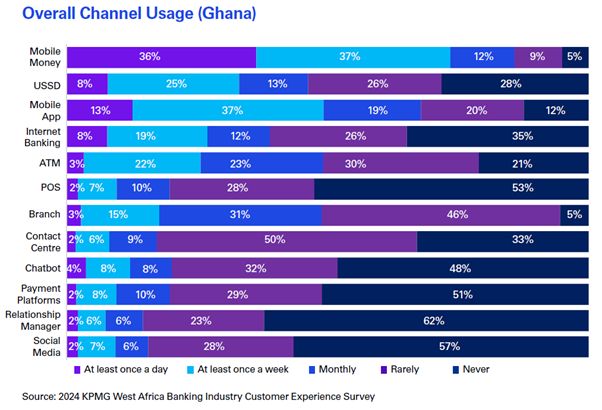

services emerged as the topmost reason for customers maintaining relationships with their banks. This was further evidenced by mobile money, mobile apps and USSD banking ranking as the top three most used payment channels for the second consecutive year.

Instant payment systems (IPS) are critical enablers of financial inclusion and convenience. Designed to facilitate real-time, secure transactions, IPS are shaping how individuals, businesses and financial institutions engage with the digital economy. According to The State of Inclusive Instant Payment Systems in Africa Report 2024, there are 28 IPS in 20 countries in Africa.

However, only seven countries have multiple IPS – Egypt, Ghana, Kenya, Morocco, Nigeria, South Africa and Tanzania. Ghana’s leadership in this space is evident, being the only African country with fully interoperable multiple instant payment systems.2 Ghana has two IPS, the Interbank Payment and Settlement Systems (GhIPSS) Instant Pay (GIP) and Mobile Money Interoperability, all of which are able to interact with each other seamlessly, enhancing customers’ ability to transfer their funds.

The impact of IPS in Ghana has been profound as the value and volume of transactions of GIP as at October 2024 increased by 174% and 32% respectively, compared to the same period last year. Mobile money continues to be the dominant payment form with the total value of mobile money transactions as at October 2024 reaching GHS 2.36 trillion, representing a 55% increase from last year. The total number of transactions increased by 20% over the same period to reach 6.6 billion transactions.3

In this year’s survey, 73% of retail customers indicated they use mobile money weekly, representing a 7-percentagepoint increase compared to last year. For the second consecutive year, retail banking customers ranked the ease of transferring money between their account and mobile wallet as the most important experience metric, highlighting the importance of interoperability between systems. Mobile money interoperability

continues to be a key driver of its adoption with the total value of mobile money interoperability transactions increasing by 23% as at October 2024.4

USSD banking is also driving payment interoperability. The survey revealed that 33% of retail banking customers use USSD banking services weekly as compared to 28% of respondents in 2023. However, concerns over service reliability persist, with customers reporting intermittent downtime of their USSD banking channels.

Mobile apps, the second most used channel after mobile money, saw a slight decline in usage, with 50% of respondents indicating weekly usage compared to 53% last year. Availability of service, ease of use and variety of features of mobile apps ranked among the ten most important experience measures for retail customers. While customers appreciate the convenience and features of banking apps, concerns around reliability remain prevalent. For instance, one aggrieved customer said, “my bank’s app consistently fails whenever I attempt to complete a transaction.” Regular updates and proactive maintenance are critical to resolving technical glitches and preventing service interruptions.

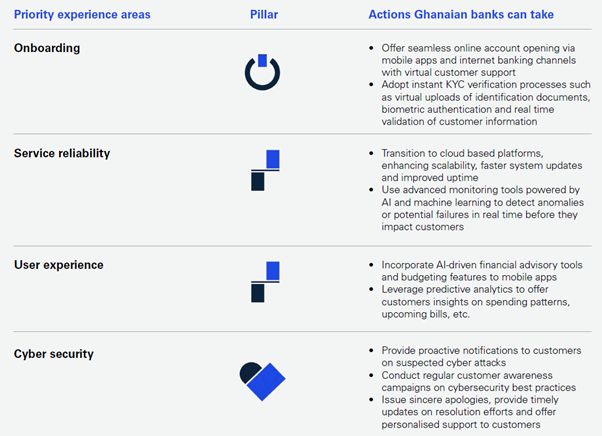

Mobile apps continue to play a vital role in the payments space offering greater convenience compared to the in-person banking experience. In this year’s survey, customers expressed significant dissatisfaction with wait times and long queues at branches, highlighting this as a critical pain point in their overall banking experience. To address this issue, banks must focus on enhancing their mobile apps with innovative features that do not only improve user convenience but also reduce the need for customers to visit branches.

Features such as instant account opening, seamless loan applications and digital document submission can streamline processes that typically require physical branch visits. Additionally, integrating advanced tools such as AI-powered virtual assistants, real-time customer support and personalised financial planning tools can further enrich the customer experience.

For instance, the Bank of America introduced Erica, an AI-powered virtual assistant, that helps users manage transactions, monitor spending and receive personalised financial advice.5

Internet banking remains the preferred channel for corporate entities, with 81% of corporate respondents reporting monthly usage. Corporates prioritise reliability and the variety of features available on online platforms, ranking these among their top ten most important experience metrics.

However, the dominance of internet banking in the corporate space is not mirrored in retail banking. This year, retail usage of internet banking saw a slight decline, with 39% of respondents indicating monthly usage compared to 43% last year. Retail customers primarily use internet banking to check account balances, pay bills and transfer funds. There was a slight increase in the percentage of respondents opening accounts online, rising to 5% from 3% last year. Despite this progress, account opening at branches remain high, with 67% of respondents indicating they opened their accounts in a branch, up from 64% last year.

Banks must prioritise adding innovative features to their internet banking channels to reduce reliance on physical branches. For instance, integrating AI-driven financial planning tools, personalised insights and goal-setting functionalities can enhance the appeal of retail internet banking. Simplified loan applications, instant dispute resolution and integrated investment management options could further incentivise retail customers to adopt internet banking.

We observed a decline in ATM usage, with monthly usage dropping from 59% in 2023 to 48% in 2024. Despite this decrease, customers generally expressed satisfaction with the availability of cash and the service uptime when using ATMs. While overall usage declined, ATMs remained the second most-used channel among Gen X and Baby Boomers highlighting a generational divide in channel preferences, with older customers continuing to rely on traditional channels for their banking needs while the younger generations prefer digital channels.

Although significant progress has been made in digital channels adoption, cybersecurity remains a critical industry concern, despite continued investments by industry players to mitigate cyber risks. The 2024 KPMG Africa CEO Outlook reported cybersecurity as the second biggest threat to CEOs and their businesses.6 This concern is further underscored by the 2023 Bank of Ghana Fraud Report, which revealed a total loss of GHS 63 million due to fraud – a 21% increase from 2022.7

Understanding and addressing the emotional toll of cyber threats on customers is just as critical as implementing technical solutions.

While the adoption of digital channels continues to grow steadily, Ghanaians remain cautious of migrating to a fully digital banking model with no physical presence. When asked whether they would consider using a banking service that operates entirely online, with no physical branches, 23% of respondents indicated they do not trust a bank without physical locations. This scepticism highlights the importance of a physical presence and human touch in building trust and confidence among Ghanaian customers.

Although digital banking offers convenience and efficiency, customers still value the reassurance and accessibility provided by physical branches, particularly when addressing complex issues or seeking personalised support. Furthermore, security and data privacy remain paramount, with 62% of respondents indicating it is extremely important for banks to protect their personal information.

For banks looking to accelerate the adoption of fully digital services, it is vital to bridge this trust gap. Strategies such as offering robust customer support systems, enhanced security measures and user-friendly digital experiences can help address customer concerns. Additionally, providing a hybrid model – blending digital services with selective physical touchpoints – may serve as a transitional approach to encourage broader acceptance of fully digital banking solutions.

Endnotes

- https://datareportal.com/reports/digital-2024-ghana

- https://www.africanenda.org/uploads/files/siips-2024-mainreport-EN.pdf

- https://www.bog.gov.gh/wp-content/ uploads/2024/11/Summary-of-Economic-and-Financial-Data-November-2024.pdf

- Ibid.

- https://promotions.bankofamerica.com/digitalbanking/mobilebanking/erica

- https://assets.kpmg.com/content/dam/kpmg/za/pdf/2024/CEO Outlook Report final_22102024.pdf

- https://www.bog.gov.gh/wp-content/uploads/2024/09/BANKS-SDIs-PSPs-2023-FRAUD-REPORT.pdf