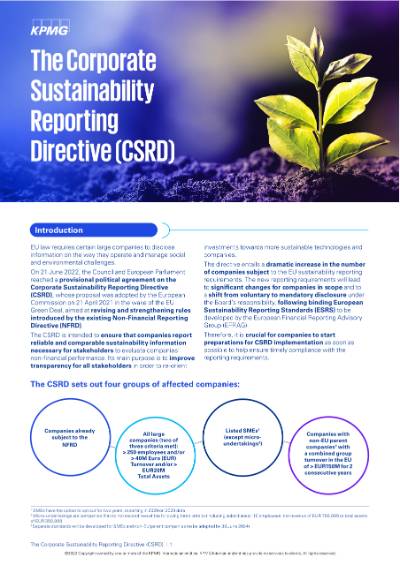

The Corporate Sustainability Reporting Directive (CSRD) adopted by the EU Parliament in November 2022 radically changes the scope and nature of sustainability reporting by companies. The CSRD significantly expands existing rules on non-financial reporting. According to the provisions of the current regulations, in addition to capital market-oriented companies (with the exception of micro-enterprises), all other large companies and groups will also be affected by the reporting obligation if they fulfil two of the following three criteria (EU thresholds, subject to transposition into national law):

- Balance sheet total > 25 million euros

- Net sales > 50 million euros

- Number of employees > 250

With the first omnibus package, the EU Commission is now proposing significant simplifications with regard to the dates of initial application, the personal scope of application and the content requirements for the reporting itself. In future, only large companies and groups with more than 1,000 employees will be required to report. The date of first-time application for non-capital-market-oriented companies in the second wave and capital-market-oriented SMEs is to be postponed by two years.

Until the amendments are adopted, the proposal published by the EU Commission must undergo the further EU legislative process involving the European Parliament and the European Council. In order to become legally effective for German companies, the provisions of the CSRD, including the amendments resulting from the omnibus initiative, must first be transposed into national law.

Our recommendations for you

Even though the EU Omnibus Initiative aims to make things easier for companies, the timing of the proposed amendments leads to a high degree of uncertainty as to whether and from when companies will be subject to which legal requirements.

Companies should use the time gained to analyse the extent to which sustainability reporting can be an important part of the corporate strategy that supports ecological change, irrespective of legal requirements. The following considerations are useful here:

- To what extent can the results of a materiality analysis that has already been carried out be used as a basis for (revising) the sustainability strategy?

- Has the preparation for reporting supported the implementation of processes, guidelines, targets and measures that are to be continued even without a reporting obligation in light of their embedding in the corporate strategy?

- Which strategic measures, guidelines and targets should the focus be on in future, for example

- Developing a transition plan for climate protection

- Identifying and managing climate risks and other sustainability-related risks

- Focus on the data points that are used for strategic decision-making

- How to maintain and improve dialogue with stakeholders on strategies, actions and targets on all material topics.

- For companies below the newly proposed thresholds: What are the reporting requirements of the VSME standard and what are the benefits of voluntary standardised reporting and its verification to meet the information needs of companies in the value chain?

Implementing sustainability reporting effectively

Our experts support you across all ESG reporting levels to make the transition to sustainability as smooth and beneficial as possible - so that you can embed the requirements of the Corporate Sustainability Reporting Directive (CSRD) in your organisation and at the same time take advantage of ESG-related opportunities.

The modular project approach can of course be customised to your needs to provide you with pragmatic solutions and services to manage the extensive sustainability reporting requirements.

Further Information

Your contacts

Stay up to date with what matters to you

Gain access to personalized content based on your interests by signing up today

Eun-Hye Cho

Partnerin, Audit, Regulatory Advisory, Sustainability Reporting & Governance

KPMG AG Wirtschaftsprüfungsgesellschaft

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia