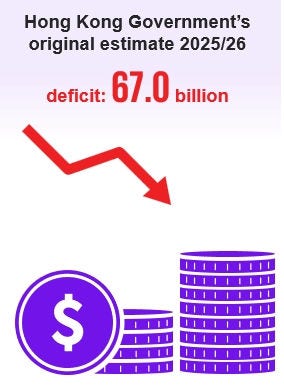

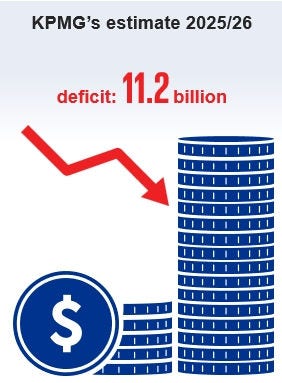

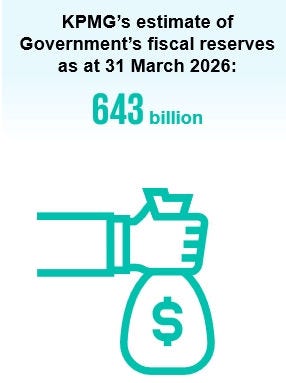

In Hong Kong dollars

Narrowed deficit compared to the original Government estimate

KPMG's proposed new measures for 2026-2027 Budget

Capitalise on the National 15th Five-Year Plan and strengthen Hong Kong as an international financial, shipping, trade and innovation and technology centre

- Attract more family offices to set up in Hong Kong – enhance the existing tax incentive regime for family offices, expanding their eligible investment scope to include digital assets and precious metals, to be attractive and effective

- Promote family offices to manage assets in Hong Kong - provide stamp duty exemption for asset transfers from high net worth individuals to their family-owned investment holding vehicles

- Support key industries – Revisit existing tax incentives for corporate treasury centre, aircraft / ship leasing and maritime services to ensure Hong Kong enterprises enjoying such tax incentives will remain competitive under BEPS 2.0 Pillar 2

- Encourage innovation and R&D activities – Expand the coverage of R&D tax deduction to include R&D activities outsourced to a Hong Kong company and performed in Hong Kong to encourage R&D activities

Strengthen Hong Kong's role as a “super connector” and attract multinational corporations and Chinese Mainland companies expanding overseas

- Reduce the costs of financing – revisit the existing stringent interest expense deduction rules to be more competitive compared to other jurisdictions

- Align with international practices – Consider introducing a withholding tax on interest income paid by non-financial institutions to non-Hong Kong residents to align with global tax standards

- Market Hong Kong as the ideal base for regional headquarters – Provide substance-based tax incentive (for example, an 8.25% preferential tax rate) for qualified profits derived from regional headquarters in Hong Kong to enhance Hong Kong's competitiveness in the Asia-Pacific region and attract foreign investment and create local job opportunities

- Enhance global competitiveness and attract multinational corporations – Revisit the tax relief available for overseas tax paid in jurisdictions with and without a double tax treaty with Hong Kong

- Promote the development of NM – Provide special policy package to the key enterprises located in NM, including but not limited to tax incentives and talent matching to promote comprehensive development

- Encourage fixed asset investment in NM – Provide accelerated tax depreciation for fixed assets located and used in NM

- Flexibly adopt public-private partnership approaches – Explore public-private partnership approaches such as joint ventures, build-operate-transfer to leverage combined expertise and share risks and costs in the development of NM

- Develop emerging industries – Develop a cross-border drone logistic network: Select pilot routes and areas to establish a cross-border low-altitude logistics network for creating new business opportunities and high-value jobs for the logistics industry

- Provide certainty and clarity on taxation of virtual assets market – Work with the industry players and tax profession to modernise the tax rules and provide greater clarity / certainty on taxation of virtual assets

- Support the development of virtual assets market – The Hong Kong SAR Government to identify suitable real world assets (RWA) (e.g. public infrastructure, commodities) and undertake a pilot RWA tokenisation project in Hong Kong

- Provide tax incentives – Introduce a general tax deduction for expenditure incurred on acquisition of intangible assets and allow a tax deduction where the intangible asset is acquired from related parties

- Foster talent and expertise – attract talents to Hong Kong to provide IP related professional services, and cultivate local expertise in IP management

- Ease the caretaking burden of working families – Provide working parents with an allowance of HK$60,000 who look after children aged 16 or below or disabled dependents through grandparents, or who employ domestic helpers through recognised institutions

- Address changing demographics and reduce financial burden of working families – Extend dependent parent and dependent grandparent allowances to eligible Hong Kong elderly who reside in the GBA

- Keep pace with the times – Adjust Salaries Tax rate bands and allowances with reference to consumer price index

- Support homebuyers – Increase the basic deduction for home loan interest from HK$100,000 to HK$120,000 per year of assessment

- Encourage charitable activities – Expanding the current tax rules regarding the deductibility of charitable donations to non-cash donation (e.g. donation of food)

- Relief for citizens and business – 100% Tax rebate capped at HK$6,000 for Profits Tax, Salaries Tax and tax under Personal Assessment

- Enhance competitiveness – Increase the cap of the Continuing Education Fund from HK$25,000 to HK$30,000, providing support for professional development and retraining for employees

- Allow the use of MPF for first home purchases – Under certain conditions, allow the use of part of MPF as a down payment for purchasing first home, providing more options for home purchase and retirement financial planning

Press release

Media coverage

Read news reporting on KPMG's recommendations designed to enhance Hong Kong’s competitiveness and ensure long-term fiscal sustainability.

etnet, etnet, etnet, i-CABLE, Infocast, Hong Kong Commercial Daily, Hong Kong Economic Journal, Hong Kong Economic Times, Hong Kong Economic Times, Hong Kong Economic Times, Metro Broadcast, Ming Pao, Quamnet, RTHK, Sing Tao, Ta Kung Wen Wei, Wen Wei Po, Yahoo Hong Kong, Yahoo Hong Kong