Globally, banks, regulators and corporates are moving beyond experimentation in stablecoins, tokenised deposits, central bank digital currencies (CBDCs), real-world asset (RWA) tokenisation and blockchain-based settlement. What has changed and accelerated this activity over the past year is the foundation beneath it all. The United States enacted its first federal stablecoin law, the GENIUS Act1, in July 2025; the European Union’s Markets in Crypto-Assets Regulation (MiCA)2 is now fully in force; and the Basel Committee’s prudential standard for banks’ crypto asset exposures (SCO60)3, together with its disclosure framework, took effect on 1 January 2026. For the first time, banks have a clear – and capital-aware – basis on which to build.

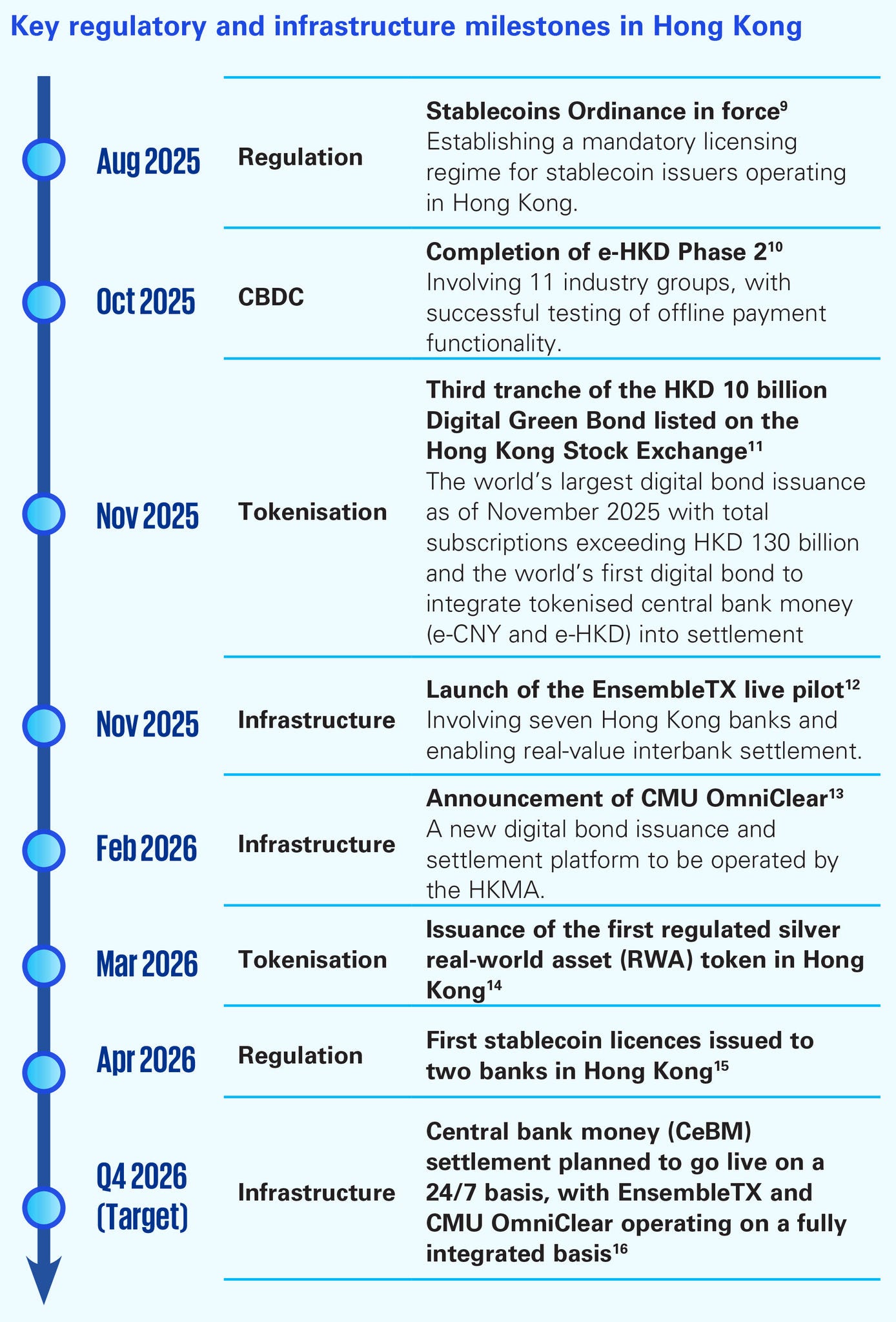

Hong Kong has moved faster and further than most. Within roughly a year it has set out a whole-of-government strategy in Policy Statement 2.04, brought a statutory stablecoin regime into force, granted its first stablecoin licenses, and – critically – taken live market infrastructure from sandbox to real-value settlement. For banks, the question is how to participate on terms that are commercially and prudentially sound.

It’s important to be candid about scale. Most digital-asset initiatives remain small relative to traditional banking, payments and capital markets activity. For many banks, the immediate priority should not be to generate significant new revenue, but to build capability, understand the risks, and avoid being left behind as market infrastructure rewires around them. We expect adoption to follow a J-curve, with a steeper acceleration likely between 2030 to 2035 as standards, interoperability and capital treatment mature.