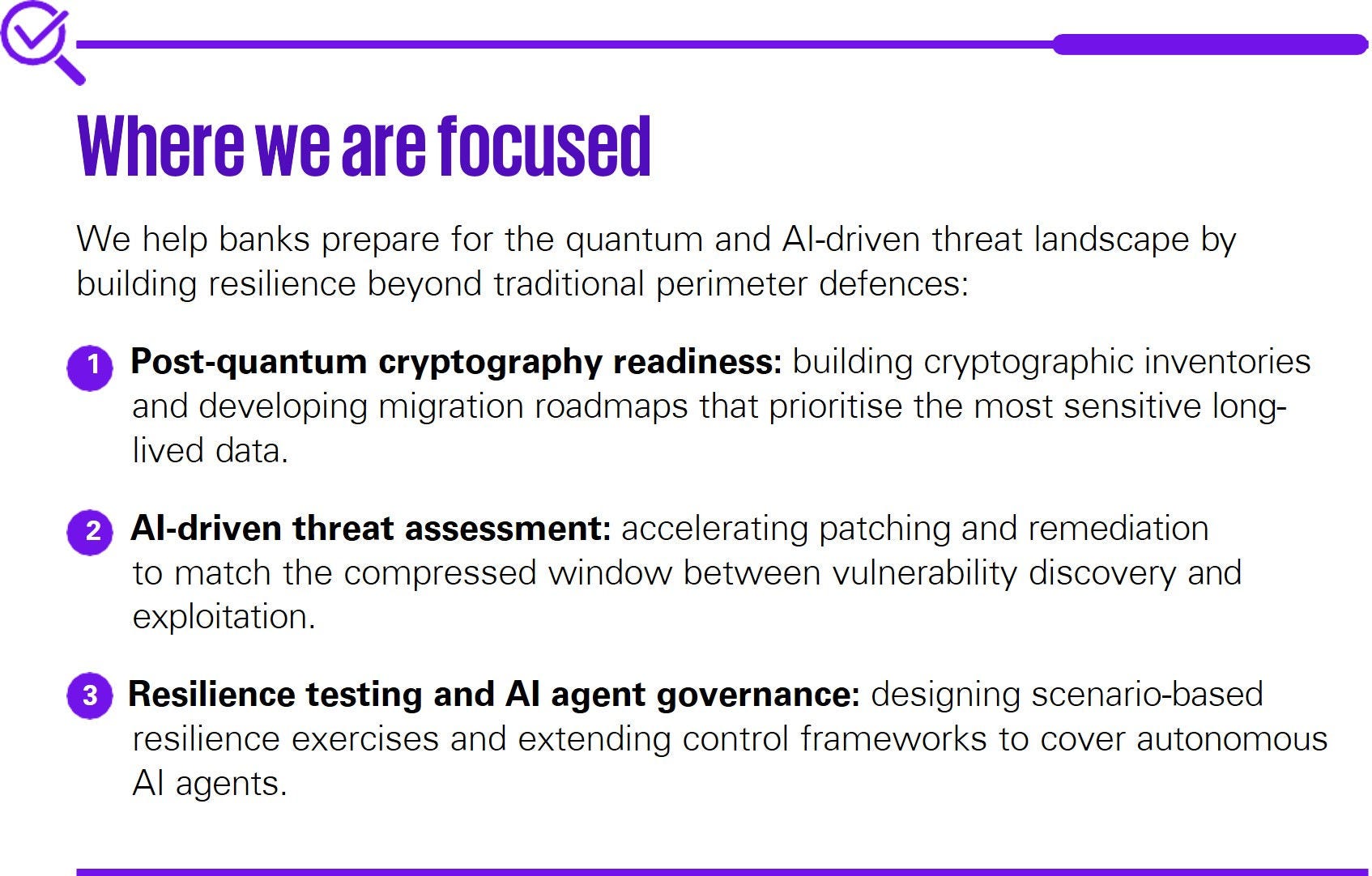

The discussion around post-quantum cryptography (PQC) has been running for several years, and the often-cited 2035 horizon can give the impression that there is still plenty of time for banks to prepare. In practice, the window for an orderly migration is narrower than it appears, and banks that leave the work until later in the decade are likely to find the exercise more difficult and more costly than it needs to be.

Two recent developments are worth noting. On the technical side, research published by Google Quantum in 2025 suggested that breaking one of the most widely used data encryption standards may require materially less computing power than previously thought1, and Google has since brought its own internal PQC migration deadline forward to 2029.

On the regulatory side, the G7 issued a coordinated PQC roadmap for the financial sector in January 20262, and in Hong Kong PQC now sits within the HKMA’s Fintech 2030 roadmap, supported by a new Quantum Preparedness Index intended to benchmark readiness across the sector3. Hong Kong banks are beginning to receive questions on how they are identifying quantum-at-risk assets.

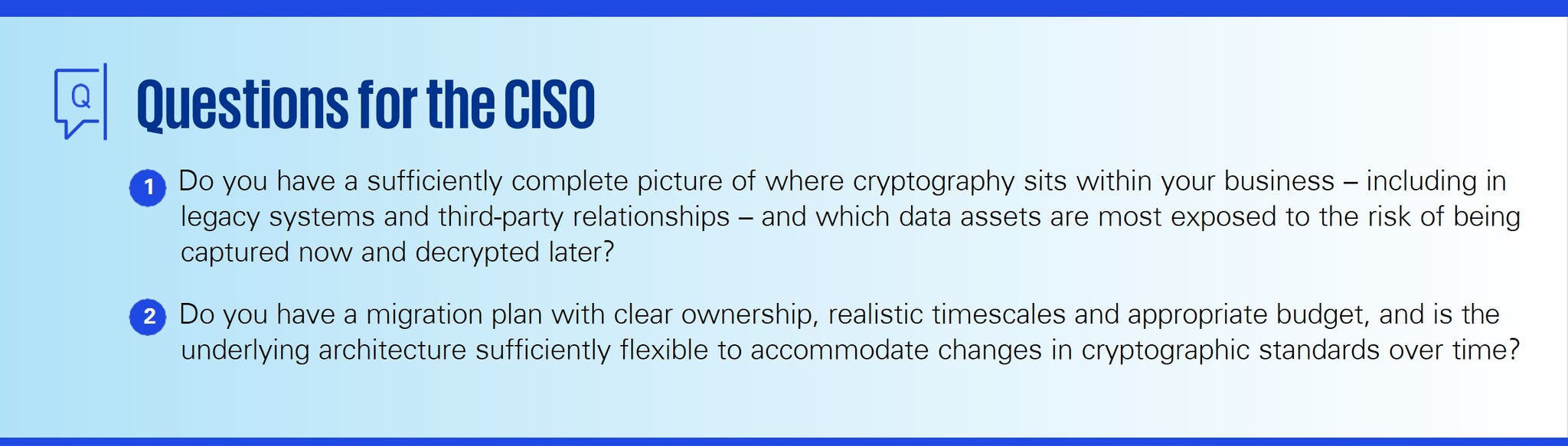

For banks, the more important point is what preparation actually involves. In our experience, the most demanding part is understanding where cryptography sits within the business in the first place. Most banks do not yet have a complete picture of which applications, data sets, keys and certificates rely on which forms of encryption, or how those dependencies extend into their third-party relationships.