The bedrock of the corporate international tax framework is all set to change from 2023. As part of the reforms introduced under BEPS 2.0, the Inclusive Framework (IF) members agreed to a minimum tax of 15% on worldwide profits earned by Multinational Enterprises (MNEs). While the work was carried out to address tax challenges brought about by the so-called digital economy, the impetus is the mitigation of tax competition that has prompted a ‘race to the bottom’ on corporate tax rates in turn putting a strain on tax revenues.

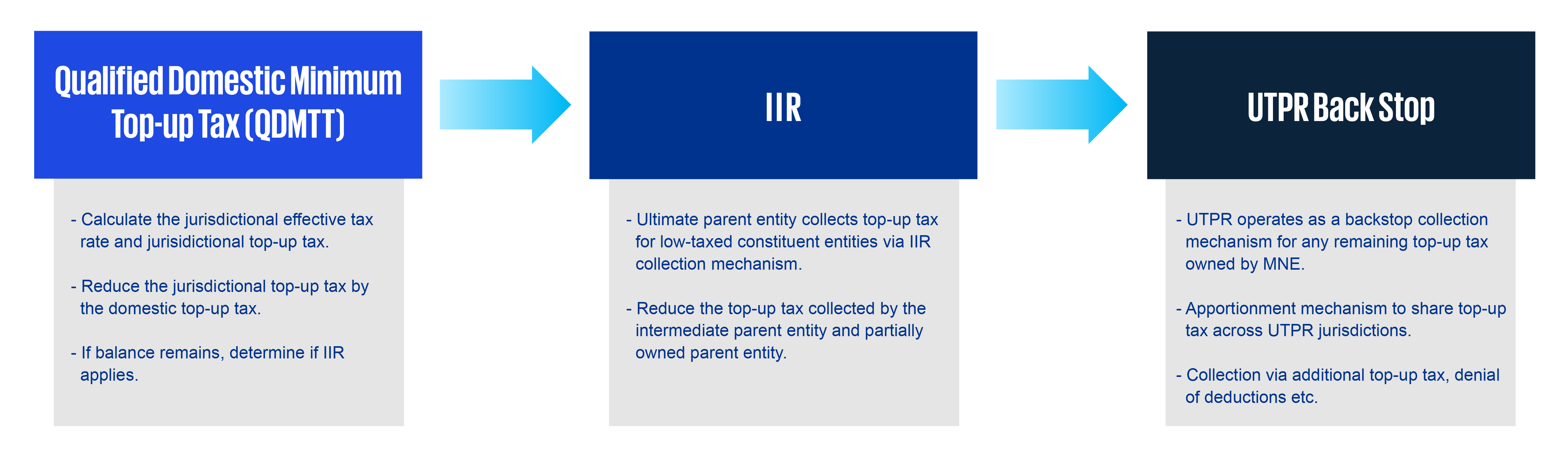

The Global Anti-Base Erosion (GloBE) Rules that form part of Pillar II lay down the framework for ensuring the collection of minimum taxation by deploying an interlocking mechanism comprising the income inclusion rule (IIR) and the undertaxed profits rule (UTPR). The IRR imposes a top-up tax on the ultimate parent entity of a low-taxed subsidiary, while the UTPR is an adjustment that acts as a backstop in cases where the IIR fails to achieve the minimum corporate tax. Rules ensure that the relevant income is subject to at least 15% tax somewhere. For this reason, several jurisdictions are opting to reduce or eliminate tax revenue leakages by introducing a domestic top-up tax, thus ensuring that in-scope entities resident in their jurisdiction are subject to minimum corporate taxation therein.