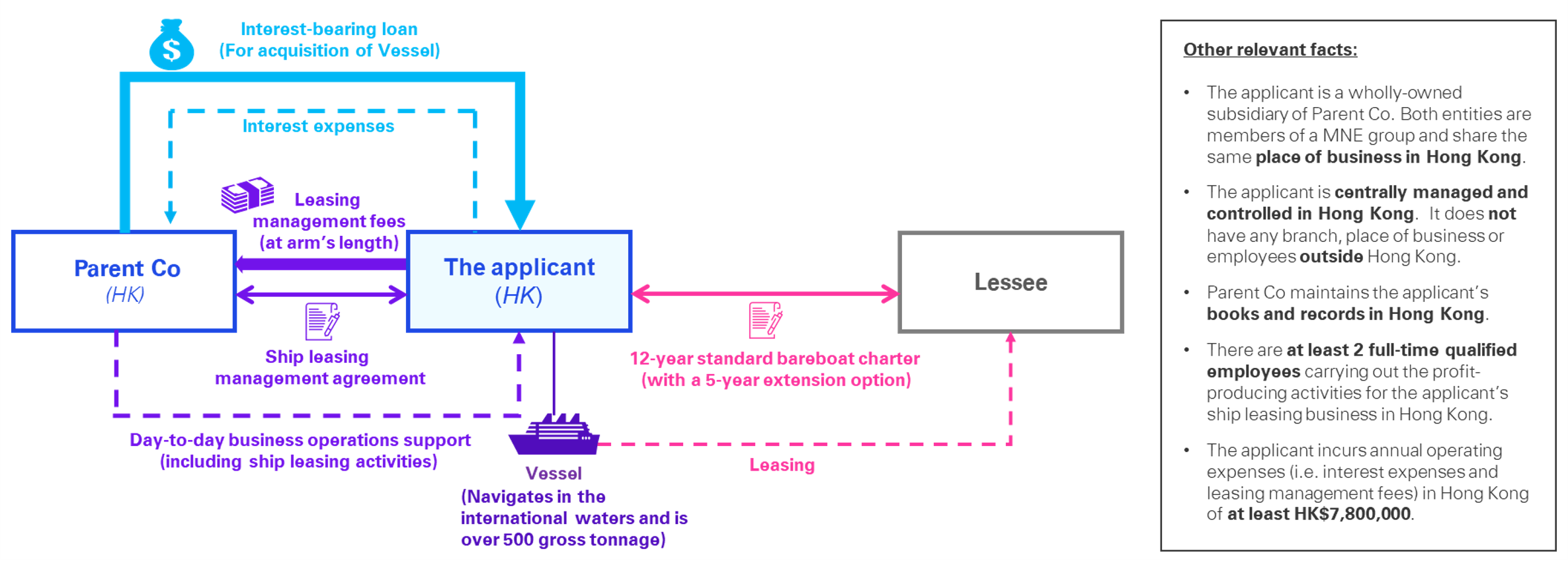

The Inland Revenue Department (IRD) recently published Advance Ruling Case No. 781. It is the first published advance ruling case on the ship leasing tax concession in the Hong Kong SAR (Hong Kong) since the concession took effect from 1 April 2020. The IRD granted a favorable ruling to the applicant (i.e. the applicant is a “qualifying ship lessor” eligible for the 0% concessionary tax rate).

In this tax alert, we summarise the key points of the case and share our observations on the application of the tax concession.