With Hong Kong’s Pillar Two framework entering its first year of implementation, in-scope MNE groups will be navigating their initial or early years of Pillar Two compliance. This article provides a practical roadmap to the key compliance milestones under Hong Kong’s Pillar Two regime, highlighting how each step interacts with existing profits tax and global reporting frameworks.

Detailed Analysis

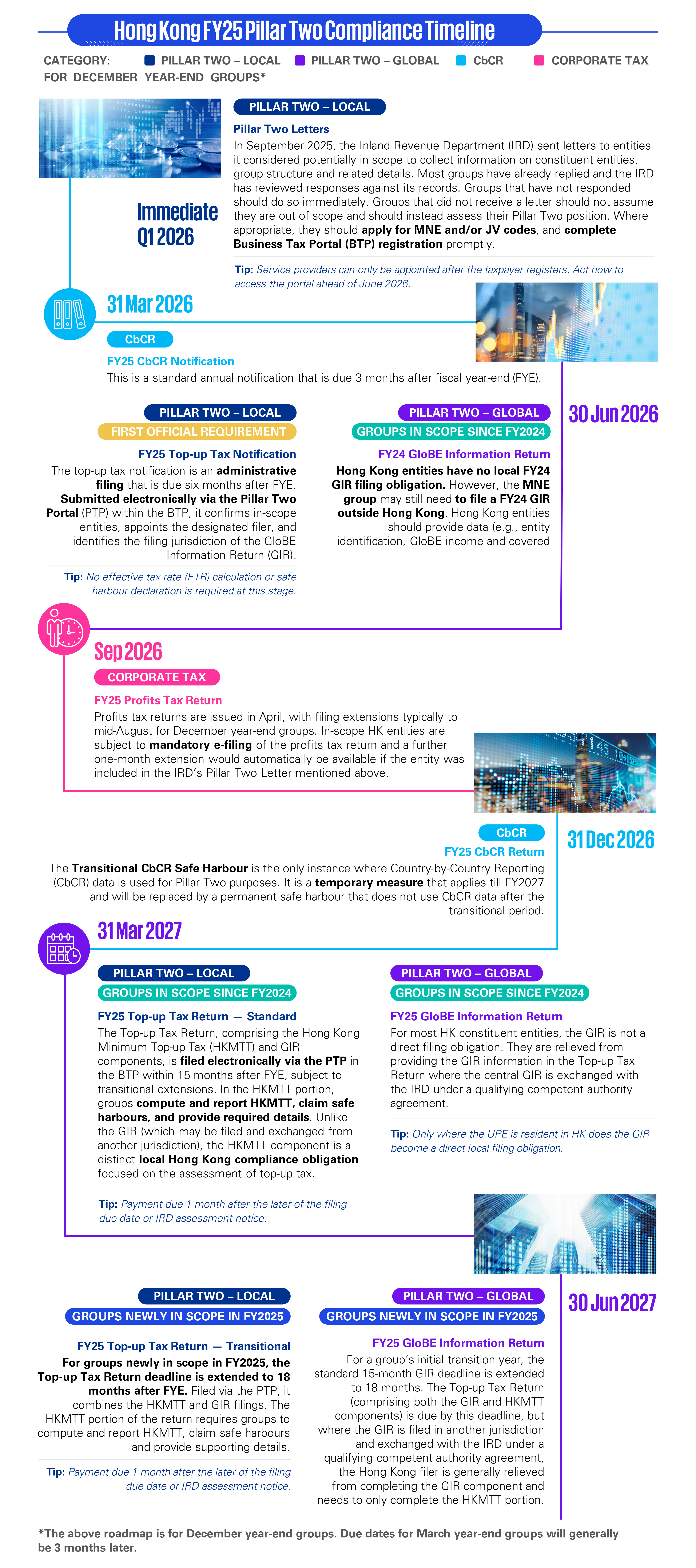

1. IRD Pillar Two Letters issued in September 2025

In late September 2025, the IRD issued letters to entities it identified as potentially part of an in-scope MNE group under Hong Kong’s Pillar Two regime. For further background on the IRD letters, please refer to our article.

For taxpayers that responded to the IRD’s letter

The IRD has been cross-checking replies against existing data, such as prior CbCR reports. Where a declaration of out-of-scope status appears inconsistent with previously submitted information, the IRD has been requesting for further clarification or supporting details. Taxpayers whose replies may not fully align with information previously submitted to the IRD should consider how to explain divergences and, if necessary, whether to supplement their responses.

For taxpayers that did not receive the IRD’s letter

Not receiving the IRD’s letter does not automatically mean that a group is out of scope. The IRD’s outreach relied on existing data and may not have captured all in-scope groups, particularly those with complex ownership chains or recent structural changes. Groups that consider they are in-scope but have not received a letter should act proactively by applying for the relevant MNE and/or JV code(s) and registering for BTP accounts. Although there is currently no legal obligation to complete these steps, obtaining the codes is mandatory for submitting top-up tax notifications and returns and so taxpayers should act sooner rather than later.

Application for MNE group code(s) and JV code(s)

An in-scope MNE group should complete Form IR1485 to apply for a unique MNE group code. It should also apply for a separate JV code(s) if the group has standalone joint ventures or JV groups in Hong Kong. These codes are mandatory for submitting top-up tax notifications and returns, which must be filed via the PTP.

Applying early allows MNE groups to access the portal ahead of the first top-up tax notification filing in June 2026. With the MNE group code, groups can test the portal’s functions, assign authorised users, and configure settings in advance. Additionally, certain information provided on Form IR1485 (such as MNE group name and UPE details) will be automatically populated in the top-up tax notification, reducing manual data input and minimizing the risk of errors.

Registration of Business Tax Portal accounts

The top-up tax notification and return are submitted electronically through the PTP, which is an extension of the BTP. The BTP is the IRD’s online platform for managing tax and/or business affairs (including profits tax e‑filings) and the PTP is a dedicated module within it for Pillar Two–related notifications and returns. To prepare for compliance, in-scope MNE groups should ensure that at a minimum the notifying entity (and any other entity that will need to access the PTP or manage appointments) has registered for a BTP account, as this is a prerequisite for using the PTP.

A key reason to register for the BTP is that Service Providers for Pillar Two filings can only be appointed within the PTP, which is accessed via the BTP. Historically, taxpayers could rely on service providers to file profits tax returns via the Tax Representative Portal (TRP) without having their own BTP accounts, but for top-up tax notification and return filings, taxpayers must first register for their own BTP accounts and then appoint Service Providers online, making timely BTP registration essential.

Enhanced e-Cert requirement

The individual authorised to file on behalf of the entity, whether an internal officer, designated filer, or Service Provider, must use a valid e-Cert (Organisational) with AEOI Functions. This is a digital certificate issued by the Hongkong Post Certification Authority that is used to authenticate the authorised user for access to the IRD’s AEOI-related electronic services, including the PTP. In practice, the entity must apply to Hongkong Post for the e-Cert, submit a supplementary application for the AEOI Function, complete the required verification process, and install the certificate on the computer or system used to access the PTP. By contrast, profits tax electronic submissions generally use the standard eTAX credentials or e-Certs without the AEOI mandate. Given that the first top-up tax notification for calendar-year groups is due by 30 June 2026, groups should complete BTP registration, representative appointments, and e-Cert set up as early as possible.

2. Top-up Tax Notification

Due Date for FY2024 Top-up Tax Notification

For December year-end groups: N/A

For March year-end groups: N/A

Due Date for FY2025 Top-up Tax Notification

For December year-end groups: 30 June 2026

For March year-end groups: 30 September 2026

Due Date for FY2026 Top-up Tax Notification

For December year-end groups: 30 June 2027

For March year-end groups: 30 September 2027

The top-up tax notification is an annual requirement for in-scope MNE groups and is due six months after the end of the relevant Pillar Two fiscal year. For Pillar Two purposes, the fiscal year generally follows the accounting period used for the UPE’s consolidated financial statements, rather than Hong Kong’s usual profits tax year of assessment. The notification is submitted electronically via the PTP and serves primarily as an administrative and scoping step. It does not require detailed ETR calculations, top-up tax computations, or safe harbour assessments.

As the first formal compliance step under Hong Kong’s Pillar Two regime, the top-up tax notification provides early clarity on group structure and reporting responsibilities. It is distinct from the IRD’s letter, which was a one-off, non-statutory outreach to identify potentially in-scope groups. By contrast, the top-up tax notification is a mandatory, recurring annual electronic filing for all in-scope MNE groups.

The notification requires MNE groups to confirm the list of in-scope Hong Kong entities, designate the group filer and identify the jurisdiction where the GIR will be filed. As the notification deadline precedes the extended profits tax return and top-up tax return deadlines, it serves as an early checkpoint for validating key compliance details and resolving uncertainties.

3. Top-up Tax Return

Each Hong Kong constituent entity of an in-scope MNE group is required to file a single top-up tax return (the “Top-up Tax Return”) that covers both the global Pillar Two regime and Hong Kong’s domestic minimum top-up tax regime. In substance, the Top-up Tax Return has two main components: (a) a GIR component that captures the standardised GloBE information, and (b) a HKMTT component that deals with Hong Kong’s domestic top-up tax computation and reporting (“HKMTT Return”). For ease of discussion, we consider each component separately in this article.

As of today, the IRD has not released the Top-up Tax Return form or template yet. Current IRD guidance and user resources focus on notification filing, registration (Form IR1485), and preparatory steps, with the second phase of the PTP (for return submissions, assessment viewing, and related functions) scheduled for launch in Q4 2026.

The Top-up Tax Return must be submitted electronically via the PTP, generally within 15 months after the end of the fiscal year, or within 18 months for groups newly in scope for Pillar Two. Therefore, for FY2025, groups already subject to Pillar Two in 2024 must meet the standard 15-month deadline, while newly in-scope groups benefit from the 18-month extension.

Due Date for FY2024 GIR (no Top-up Tax Return obligation in Hong Kong)

For December year-end groups: 30 June 2026

For March year-end groups: 30 September 2026

Due Date for FY2025 Top-up Tax Return

For December year-end groups already subject to Pillar Two in 2024: 31 March 2027

For March year-end groups already subject to Pillar Two in 2024: 30 June 2027

For December year-end groups newly subject to Pillar Two in 2025: 30 June 2027

For March year-end groups newly subject to Pillar Two in 2025: 30 September 2027

Due Date for FY2026 Top-up Tax Return

For December year-end groups: 31 March 2028

For March year-end groups: 30 June 2028

3a. GloBE Information Return

Under the OECD’s GloBE rules, the standardised GIR is filed centrally by the UPE or DFE, typically within 15 months after fiscal year-end, or 18 months for the transitional year.

GIR obligations where the UPE is in Hong Kong

For outbound MNE groups where the UPE is a Hong Kong tax resident, there is no GIR filing obligation in Hong Kong for FY2024. However, if the MNE group is in scope of Pillar Two in other jurisdictions for FY2024, a GIR will still need to be filed in those implementing jurisdictions.

From FY2025 onwards, there is a GIR filing obligation in Hong Kong. The Hong Kong UPE (or another Hong Kong DFE) will generally be responsible for filing the GIR via the PTP. The GIR will then be available for exchange with other jurisdictions in which the group operates, provided the necessary qualifying competent authority agreements are in place.

GIR obligations where the UPE is outside Hong Kong

There is no GIR filing obligation in Hong Kong for FY2024.

From FY2025 onwards, the GIR is unlikely to be a direct filing obligation for most Hong Kong constituent entities of inbound MNE groups. Where the GIR is filed in another jurisdiction and exchanged with the IRD under a qualifying competent authority agreement, Hong Kong entities should generally not be required to provide the GIR information in the Top-up Tax Return.

Information collection for GIRs to be filed outside of Hong Kong in respect of FY2024 and future years

There is no GIR filing obligation in Hong Kong in respect of FY2024. However, many groups will operate in jurisdictions where a FY2024 GIR filing obligation does exist, and Hong Kong information may be required to be included in those GIRs and future GIRs.

The scope of information that Hong Kong constituent entities should supply in respect of the FY2024 and future GIR filings could depend on the specific filing requirements implemented in the filing jurisdiction, the taxing rights of that jurisdiction, and whether the Transitional CbCR Safe Harbour can be applied. Where the Transitional CbCR Safe Harbour is available, the data required is limited to broadly CbCR-based and financial statement data (e.g., revenue, profit before tax, taxes accrued, employees and tangible assets) with no full GloBE calculations needed. Where the safe harbour cannot be applied, a full GloBE computation may be required, including detailed GloBE income adjustments and covered tax computations. Determining safe harbour eligibility early is therefore critical, as it materially drives the scale and complexity of the data collection exercise.

It is important for groups to establish clear internal protocols early and to identify which jurisdiction or entity will take responsibility for coordinating data collection and preparing the GIR. Factors to consider include where the majority of relevant data resides, the systems and processes in place, and which entity has the resources and expertise to compile and prepare the returns in respect of FY2024 and future years.

3b. HKMTT Return

The HKMTT Return is the component of the Top-up Tax Return that deals with Hong Kong’s domestic minimum top-up tax computation and reporting. This filing serves as the compliance mechanism for Hong Kong, computing the HKMTT liability (if any) by applying safe harbours and the relevant HKMTT rules. It forms the basis for the IRD to issue a notice of assessment. Payment is generally due one month after the later of the filing deadline or the IRD’s assessment notice.

As previously discussed, where the GIR is filed in another jurisdiction by the UPE or a DFE and exchanged with the IRD under a qualifying competent authority agreement, Hong Kong constituent entities are generally not required to complete the GIR section of the Top-up Tax Return. However, this relief does not extend to the Hong Kong specific information which is included in the HKMTT Return. In-scope Hong Kong entities must still complete and file the HKMTT Return portion of the Top-up Tax Return with the IRD.

4. Profits Tax Return

Due Date for FY2025 Profits Tax Return

For December year-end groups: May 2026 - September 2026

For March year-end groups: May 2026 - December 2026

Due Date for FY2026 Profits Tax Return

For December year-end groups: May 2027 - September 2027

For March year-end groups: May 2027 - December 2027/January 2028

The FY2025 Hong Kong profits tax return, issued in April 2026, is typically filed between May and mid-September under block extensions and e-filing grace for December year-end groups. The Hong Kong profits tax compliance process will continue to digitalise in 2026. All block extension applications must be submitted electronically via the TRP. Entities within an in-scope MNE group that is subject to Hong Kong’s Pillar Two regime are generally required to file their profits tax returns electronically, subject to certain exceptions, and to submit all supplementary forms and supporting documents electronically. The profits tax return has also been updated to include new disclosure fields, such as identifying whether the entity is within the Pillar Two regime. These changes enhance alignment and transparency between the profits tax and Pillar Two regimes.

While there is limited direct overlap in computational data between the profits tax return and Pillar Two filings, the profits tax return process plays a key role in confirming foundational information, such as legal names, Hong Kong Business Registration Numbers, and, via financial statement disclosures, ownership and residency. These details should align with the Hong Kong constituent entity list in the top-up tax notification and the entity master for the GIR. In practice, the interaction between the profits tax return and Pillar Two compliance is more about ensuring consistency and robust governance across regimes. Early confirmation of in-scope entities and reporting responsibilities through the top-up tax notification provides a framework for profits tax return preparation, while the finalized profits tax return and underlying accounts serve as a reference point for subsequent Pillar Two filings.

5. CbCR Notification and Filing

Due Date for FY2025 CbCR Notification

For December year-end groups: 31 March 2026

For March year-end groups: 30 June 2025

Due Date for FY2025 CbCR Filing

For December year-end groups: 31 December 2026

For March year-end groups: 31 March 2026

Due Date for FY2026 CbCR Notification

For December year-end groups: 31 March 2027

For March year-end groups: 30 June 2026

Due Date for FY2026 CbCR Filing

For December year-end groups: 31 December 2027

For March year-end groups: 31 March 2027

CbCR obligations operate alongside Pillar Two but are governed by separate rules. The only explicit use of CbCR data for Pillar Two purposes is to assess the eligibility for the Transitional CbCR Safe Harbour.

Originally, the Transitional CbCR Safe Harbour was generally available until FY2026. However, as announced in the OECD’s Side-by-Side Package, the transitional period was extended by one year. In other words, the safe harbour can now apply up to the year ending 31 December 2027 for December year-end groups and up to the year ending 31 March 2028 for March year-end groups. For groups with an unusually long fiscal year, the safe harbour cannot be used for any fiscal year that ends after 30 June 2029. The Transitional CbCR Safe Harbour is a temporary measure and is conditional on the availability of a Qualified CbC Report.

All three safe harbour tests – the de minimis test, the simplified ETR test, and the routine profits test – draw on data from the Qualified CbC Report. The report qualifies only where it is prepared and filed using Qualified Financial Statements, being the financial statements used to prepare the UPE’s consolidated accounts or the local statutory accounts prepared under an acceptable financial reporting standard. This means that where any jurisdiction’s data within the CbCR is drawn from management accounts, internal reporting systems, or other non-qualifying sources, the CbCR will be treated as non-qualified for that jurisdiction, and the safe harbour will be unavailable regardless of whether the underlying Pillar Two calculation would otherwise support it.

In practice, many MNE groups have relatively weak CbCR processes, such as incomplete templates or unreliable local level data, which may result in a failure to produce a Qualified CbC Report. Groups should therefore review the quality and robustness of their CbCR processes as a matter of priority, as any deficiency at the CbCR level directly affects the availability of the safe harbour.

After the transitional period, the safe harbour will be replaced by the permanent Simplified ETR Safe Harbour regime, which does not rely on CbCR data.