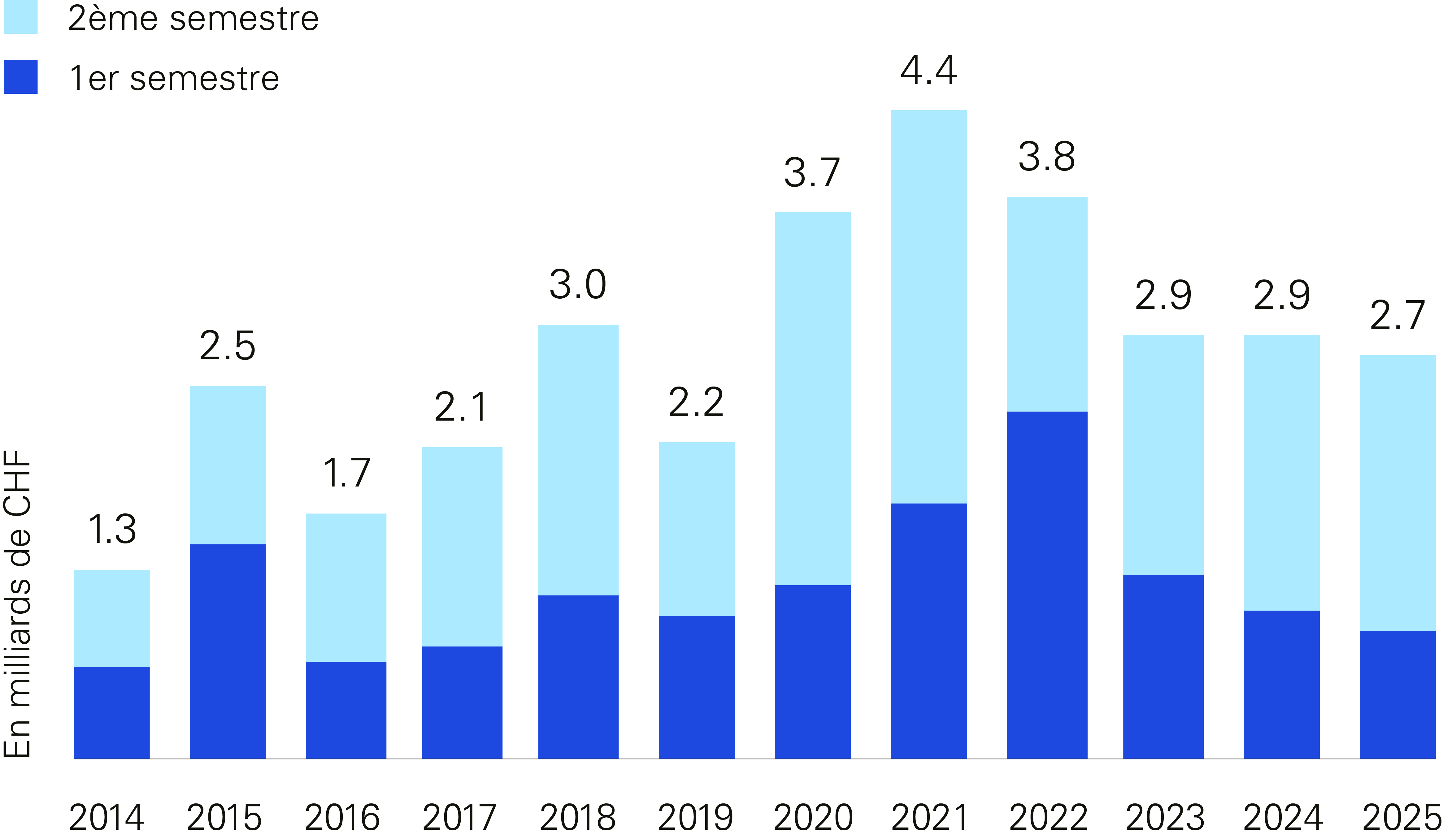

With approximately CHF 2.7 billion invested in 2025, the Geneva real estate investment market is entering a critical phase following a two-year correction period. While the recorded transaction volumes reflect a certain economic slowdown, several leading indicators point to a gradual return of transaction momentum.

In an environment marked by ongoing economic and geopolitical uncertainty, falling interest rates and solid local fundamentals in Geneva are leading to a realignment of investors’ investment strategies.

Looking ahead to 2026, three key trends are shaping this new cycle:

- Increased selectivity among investors when acquiring investment properties

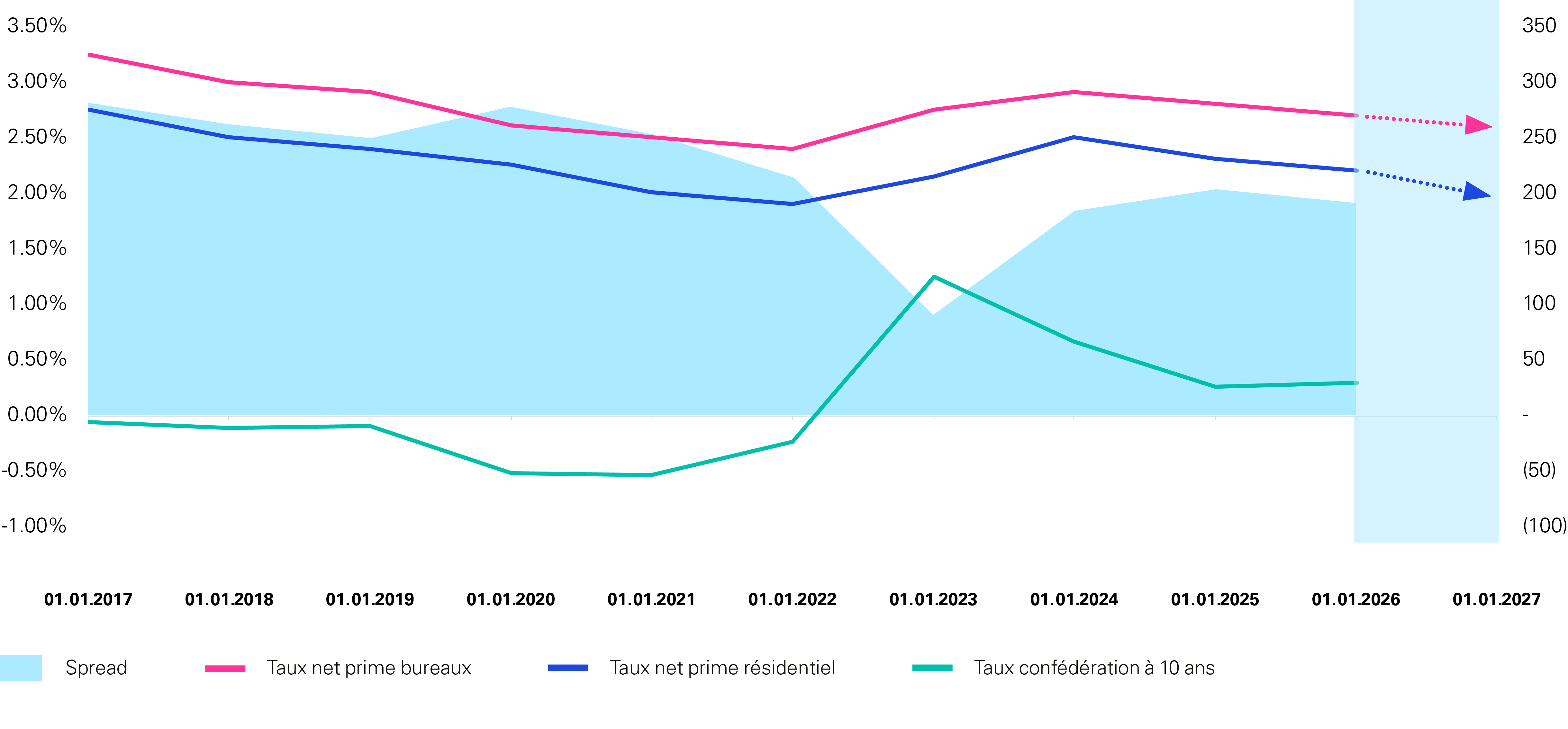

- Persistent pressure on yields, exacerbated by the SNB’s easing of its key interest rate

- Growing and sustained investor interest in ESG-compliant residential real estate, driven by robust tenant demand

The study analyzes the development of the market for direct real estate investments in the Canton of Geneva, including investment volumes, returns, investor structures, and outlook for 2026.