Serbia: Rulebook on arm’s length interest rates for 2023

Interest rates for for all non-finance entities and a single interest rate for banks and finance leasing companies

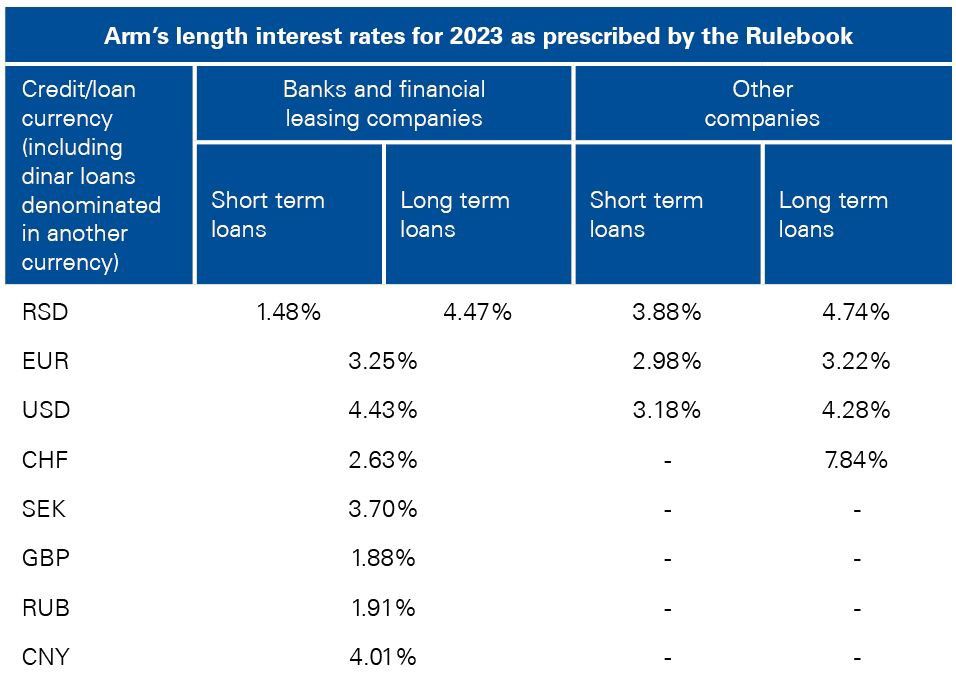

Interest rates for 2023

The Ministry of Finance adopted the rulebook on arm’s length interest rates for 2023. The rulebook was published in the official gazette dated 29 March 2023 and is effective 6 April 2023.

Background

According to the provisions of article 61 of the corporate income tax law, in determining arm’s length interest income or expense, taxpayers can:

- Use interest rates as prescribed by the rulebook

- Apply general OECD-based methods for assessment of arm’s length interest as prescribed by the corporate income tax law

The selected option must be consistently applied to all intercompany loans, and prescribed interest rates must be applied to income and expense recognized during 2023 regardless of the period from which loan(s) originate.

Rulebook

The rulebook prescribes separate interest rates for long-term and for short-term borrowings for all non-finance entities and a single interest rate for banks and finance leasing companies (except for RSD denominated loans when interest rate is prescribed separately for short-term and long-term loans).

KPMG observation

The rulebook provides an upward trend of interest rates from 2022 in line with increasing average borrowing costs in the economy.

Companies exposed to significant, long-term related-party financing may want to consider applying general OECD-based methods for assessment of arm’s length interest, as that approach may be more beneficial and provide an increased level of certainty in relation to future tax treatment.

The effect of the rulebook on the application of beneficial withholding tax rates on interest in accordance with income tax treaties requires detailed review.

Read a March 2023 report [PDF 2.0 MB] prepared by the KPMG member firm in Serbia

The KPMG name and logo are trademarks used under license by the independent member firms of the KPMG global organization. KPMG International Limited is a private English company limited by guarantee and does not provide services to clients. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. For more information, contact KPMG's Federal Tax Legislative and Regulatory Services Group at: + 1 202 533 3712, 1801 K Street NW, Washington, DC 20006.