- Singapore's AI funding soared by 77 percent to US$481.21 million in 2023 across 24 deals, signifying increasing faith in AI's potential.

- Singapore's crypto, payment, and insurtech sectors showed resilience amid market fluctuations, with investors evolving their strategies.

- Global fintech funding halved from US$196.6 billion (7,515 deals) in 2022 to US$113.7 billion (4,547 deals) in 2023, paralleled by a 68 percent decline in Singapore's fintech investments.

- Despite challenges, Singapore secured 21 percent of Asia Pacific's fintech deals, solidifying its regional prominence.

- The Americas led global fintech funding in 2023, drawing nearly 70 percent of total investments (US$78.3 billion), highlighting its sustained global significance.

6 February 2024, Singapore – Singapore's fintech sector has witnessed an extraordinary surge in funding for artificial intelligence (AI) technologies, despite a global downturn in fintech investments. The KPMG Pulse of Fintech H2’23 report reveals that AI fintech funding in Singapore skyrocketed to an impressive US$333.13 million in H2’23, marking a significant 77 percent increase from the US$148.08 million recorded in H1’23. This culminates in a total AI sector investment of US$481.21 million across 24 deals in 2023 in Singapore. Amidst this AI funding boom, companies have been rapidly innovating and launching AI-driven products to secure a competitive advantage.

In contrast, global fintech investments in the AI subsector experienced a slowdown, plunging from US$28.1 billion in 2022 to just US$12.1 billion in 2023. However, this decline in direct investment does not reflect a dwindling interest in AI. Many financial institutions and fintech firms worldwide have chosen to harness the power of AI through strategic alliances and product expenditure, rather than direct investment, throughout 2023.

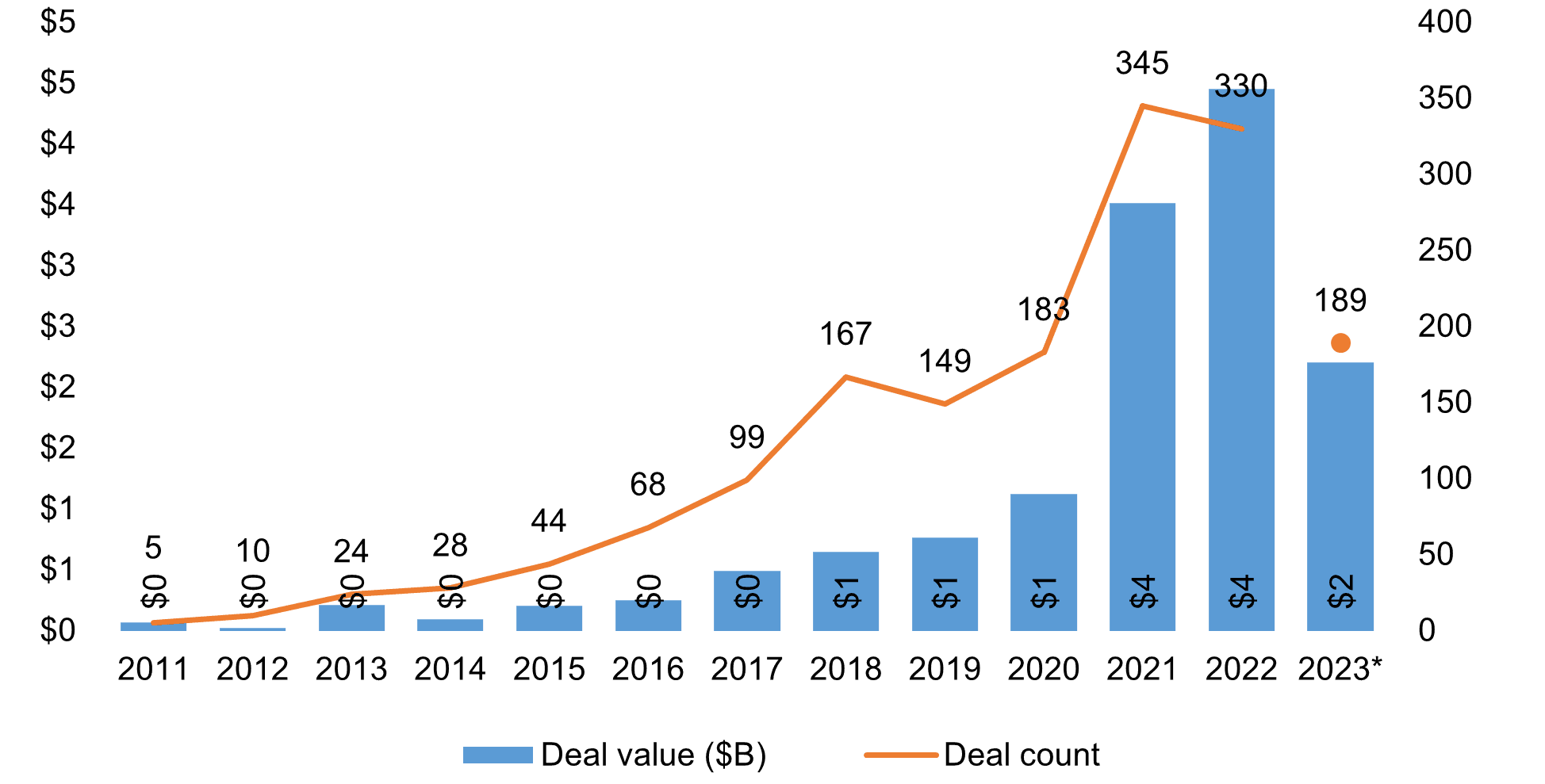

On a broader scale, Singapore's fintech sector amassed total funding of US$2.20 billion, inclusive of mergers & acquisitions (M&A), private equity (PE), and venture capital (VC) deals in 2023. This represents a substantial 68 percent decrease from the US$4.4 billion raised in 2022. Deal activity also saw a sharp decline, halving to 189 in 2023 from the previous year. This downward trend was particularly pronounced in H2’23, with funding falling by 64 percent, from US$1,455 million across 102 deals to US$747 million across 87 deals.

“The fintech market floundered somewhat in 2023, buffeted by many of the same issues challenging the broader investment climate. While there were still good deals to be had, investors were definitely sharpening their pencils—enhancing their focus on profitability,” said Anton Ruddenklau, Global Head Fintech and Innovation, Financial Services, KPMG International. “While it was a depressed year for the fintech market overall, there were a few particularly bright lights. Proptech, ESG fintech, and investors embraced AI-focused fintechs—which helped particularly in the last six months.”

This marks the slowest performance for fintech funding since the Covid-19 year of 2020, when only US$1.13 billion was raised across 183 deals. The dampened investor sentiment can be attributed to geopolitical conflicts, a high interest rate environment, and a lacklustre exit environment across regions, which prompted fintech investors to exercise caution and conserve their cash reserves throughout 2023. Furthermore, the increased scrutiny of potential fintech deals, with an emphasis on profitability and avoidance of down rounds, further shaped the funding landscape in 2023.

Singapore Continues to Dominate Asia Pacific's Fintech Landscape in 2023

Despite a widespread slowdown in the fintech sector, Singapore has emerged as a leader in the Asia Pacific region, accounting for a substantial 21 percent of all fintech deals in the area. This reinforces its reputation as a premier fintech hub in Asia.

The year 2023 saw some significant fintech deals in Singapore. A venture capital deal with digital bank AnextBank topped the list, raising an impressive US$359 million. Close on its heels was insurtech firm Bolttech, which secured US$246 million in funding.

Furthermore, the resilience and evolution of Singapore's fintech sector in 2023 were truly commendable. In an environment fraught with challenges, investors shifted their focus towards early-stage companies, resulting in 74 deals, and seed funding, leading to 63 deals. These transactions were primarily responsible for smaller deal sizes.

This trend underscores a strategic move by investors to diversify risk while remaining committed to exploring, learning, and assessing the commercial viability of a diverse array of next-wave fintech business models.

Global Fintech Investment Trends and Top Deals in 2023: A Year of Challenges and Opportunities

The global fintech market faced a series of hurdles in 2023, as total investment dropped to a six-year low of US$113.7 billion across 4,547 deals, down from US$196.6 billion across 7,515 deals in 2022. However, the second half of 2023 showed slight resilience with a marginal gain over the first half, rising from US$55.5 billion in H1’23 to US$58.2 billion in H2’23.

This slight recovery was significantly bolstered by six notable deals exceeding US$1 billion each, including the acquisitions of Black Knight (US$11.7 billion) and Adenza (US$10.5 billion), a private equity raise by Finastra (US$6.9 billion), the buyout of Avantax (US$1.2 billion), and a venture capital raise by Generate (US$1 billion) along with the acquisition of Pismo by Visa (US$1 billion). Despite these highlights, VC investment experienced a downward trend, falling from US$27.5 billion to US$18.8 billion between H1’23 and H2’23.

Regionally, the Americas dominated the fintech funding landscape in 2023, accounting for nearly 70 percent of total investment (US$78.3 billion across 2,136 deals). The United States spearheaded this surge with an investment of US$73.5 billion. In contrast, the EMEA region received US$24.5 billion of total fintech investment across 1,514 deals, and the ASPAC region saw US$10.8 billion across 882 deals.

In terms of sectors, the payments space attracted the highest share of fintech investment globally (US$20.7 billion), albeit at a substantial drop from the US$58 billion in 2022. Meanwhile, proptech and ESG were very hot with investors. Proptech investment soared to a record high of US$13.4 billion in 2023, while ESG-focused fintech investment saw a significant year-over-year increase, rising from US$1.2 billion to US$2.3 billion.

Fintech investment in the Asia-Pacific Region Falls by More than 75 percent

It was an incredibly soft year for fintech investment in the ASPAC region, with only US$10.8 billion of investment across 882 deals in 2023—down from US$51.3 billion in investment in 2022—although the 2022 numbers were buoyed by the US$29 billion acquisition of Australia-based Afterpay. Fintech investment in India was particularly soft, falling from US$6.8 billion to US$3 billion between 2022 and 2023, although investment also dropped in Singapore—from US$4.5 billion to US$2.2 billion. Fintech investment in China rose year-over-year—from a ten-year low of US$800 million to US$1.9 billion. VC investment in the ASPAC region dropped from US$15.4 billion in 2022 to US$7.8 billion in 2023. Of this, corporates participated in US$4.1 billion of deals.

H2’23 was slightly slower in ASPAC, with fintechs attracting US$3.4 billion in investment. VC raises accounted for the vast majority of investment in H2’23, including by Hong Kong (SAR), China-based Micro Connect (US$458 million) and Singapore-based Boltech (US$246 million)), India-based Perfios (US$229 million), and Japan-based Gojo & Company (US$110.6 million).

Crypto Continues to Attract Singapore Investors Despite Challenges

Despite experiencing a decline from the previous year, the crypto/blockchain subsector remained the top fintech focus in Singapore in 2023. Investments totalled US$626.8 million across 88 deals, compared to US$1,169.8 million across 131 deals in 2022.

This indicates that even amidst a challenging environment, Singapore remains resolute in its dedication to progressing the crypto space. The nation strikes a careful balance between fostering innovation and implementing necessary regulations.

This commitment was particularly evident in H2’23. Singapore rolled out new requirements aimed at safeguarding customer assets held by Digital Payment Token providers. Additionally, the regulatory framework for stablecoins was finalised. This resulted in approvals being granted to Paxos and StraitsX to issue regulated USD and SGD stablecoins.

H1'23 | H2'23 | |||

Deal size US$ (Millions) | No. of Deals | Deal Size US$ (Millions) | No. of Deals | |

Reg Tech | $1.3 | 2 | $12.8 | 3 |

Insur Tech | $4.1 | 1 | $284.1 | 4 |

Wealth Tech | - | - | $35 | 2 |

Proptech | $0.20 | 1 | $0.50 | 2 |

Cybersecurity | $0.10 | 1 | - | 1 |

Payments | $43.49 | 10 | $142.65 | 14 |

Crypto | $460.5 | 50 | $166.3 | 38 |

AI & ML deals | $148.08 | 10 | $333.13 | 14 |

Figure 2: Singapore’s fintech subsector deal size and volume for H1 2023 vs H2 2023

2022 | 2023 | |||

Deal size US$ (Millions) | No. of Deals | Deal Size US$ (Millions) | No. of Deals | |

Reg Tech | $63.2 | 10 | $14.1 | 5 |

Insur Tech | $362.6 | 9 | $288.2 | 5 |

Wealth Tech | $500 | 4 | $35 | 2 |

Proptech | $16.4 | 6 | $0.70 | 3 |

Cybersecurity | $15.4 | 6 | $0.10 | 2 |

Payments | $984.78 | 23 | $186.13 | 24 |

Crypto | $1,169.8 | 131 | $626.8 | 88 |

AI & ML deals |

|

| $481.21 | 24 |

Figure 3: Singapore’s fintech subsector deal size and volume for 2022 vs 2023

Insurtech and Payment Sectors in Singapore Demonstrate Resilience Amid Market Fluctuations

Singapore's insurtech sector experienced a significant surge in investment during H2’23, marking a 194 percent increase to US$284.1 million from US$4.1 million in H1'23. A total of four deals were struck, amounting to US$288.2 million, with Bolttech, a Singapore-based insurtech firm, securing the largest investment through a US$246 million early-stage VC round.

The sector has seen a strategic shift towards catering to the small and medium-sized enterprises (SME) market, capitalising on the untapped potential within this segment. However, the success of these insurtech firms will hinge on their ability to navigate the inherent complexities of insurance products.

In an apparent pivot, insurtech firms are now focusing on addressing specific pain points within the insurance value chain, including claims management, rental market solutions, and broker enablement. This B2B-oriented approach deviates from direct competition with incumbent insurers and is expected to gain further traction, indicating a strategic evolution within the insurtech landscape.

Despite a considerable drop in annual investment—from US$984.78 million in 2022 to US$186.13 million in 2023—the payments sector sustained one of the largest shares of fintech investment in Singapore. The resilience of this sector is evidenced by the stability in deal volume, maintaining 23 deals in 2022 and slightly increasing to 24 deals in 2023.

While the overall investment size has declined, the consistent level of interest and activity indicates that the payments sector remains a critical component of the fintech ecosystem. Fintech firms operating in this space continue to adapt to evolving market dynamics, regulatory changes, and heightened competition, which have led to adjustments in funding strategies.

Other Global Highlights and Developments in 2023

- Global fintech investment was US$113.7 billion across 4,547 deals in 2023 – down from US$196.6 billion across 7,515 deals in 2022.

- The Americas attracted US$78.3 billion across 2,136 deals in 2023—of which the US accounted for US$73.5 billion across 1,734 deals—while the EMEA region attracted US$24.5 billion across 1,514 deals, and the ASPAC region attracted US$10.8 billion across 882 deals.

- Global M&A deal value dropped from US$98.2 billion in 2022 to US$56.4 billion in 2023; global VC investment declined from US$88.8 billion to US$46.3 billion year-over-year. PE growth investment showed the most resilience, up from US$9.6 billion in 2022 to US$11 billion in 2023.

- Payments remained the strongest area of fintech investment globally in 2023, with US$20.7 billion in investment compared to US$58 billion in 2022; 2023 investment in other notable sectors included proptech (US$13.4 billion), insurtech (US$8.1 billion), crypto and blockchain (US$7.5 billion), regtech (US$2.6 billion), ESG fintech (US$2.3 billion), and cybersecurity (US$1.3 billion)

- Corporate-participating VC investment globally fell from US$45.9 billion in 2022 to US$25.2 billion in 2023.

Second Best Year for ESG Fintech Investment

2023 was the second-best year for fintech investment on record, with the US$2.3 billion in investment second only to 2021’s peak high of US$3.7 billion. The US accounted for the largest deals in this space in 2023, including US$1.1 billion deal by sustainable infrastructure startup Generate, a US$1 billion PE raise by carbon custody platform Rubicon Carbon, a US $525 million VC raise by environmental commodities firm Xpansiv, and a US$500 million raise by cleantech investment firm CleanCapital. The combination of ongoing regulatory changes and the ambitious net zero commitments by both governments and businesses will likely keep investment in ESG-focused fintech solutions on a positive trend heading into 2024.

US Accounts for US$73.5 billion of the US$78.3 billion in Fintech Funding Seen in Americas

Total annual fintech investment in the Americas fell from US$95.4 billion across 3,467 deals in 2022 to US$78.3 billion across 2,136 deals in 2023. The US attracted the vast majority of fintech deals activity during the year, accounting for US$73.5 billion of investment across 1,734 deals. Brazil attracted US$2.6 billion across 111 deals, while Canada saw US$920 million across 109 deals. VC investment fell sharply in the region, dropping from US$44.7 billion to US$26.6 billion year-over-year. Corporates participated in US$15.1 billion of these deals.

The second half of 2023 was particularly weak for the fintech market in the Americas—with US$38.4 billion of investment across 916 deals in H2’23. The US accounted for US$35 billion of this investment.

EMEA Region Sees Investment in Fintech Drop to a Seven-Year Low of $24.5 billion in 2023

Fintech investment in the EMEA region plummeted to US$24.5 billion across 1,514 deals in 2023 from US$49.6 billion across 2,478 deals in 2022. H2’23 saw an increase in investment over the first half of the year, accounting for US$16.3 billion compared to US$8.2 billion. The US$6.9 billion PE raise by UK-based Finastra accounted for over half of this funding, however.

H2’23 showcased the geographic diversity of the EMEA region’s fintech market, with fintechs from seven different countries represented in the region’s top ten deals. In addition to the UK’s, Sweden (Macrobond Financial - US$763.8 million), the Netherlands (PayU - US$610 million), Italy (Banco BPM - US$548.9 million), the United Arab Emirates (Tabby – US$950 million, Haqqex - US$400 million), Finland (Nomentia - US$385.1 million), and Spain (Gestión Tributaria Territorial - US$325.7 million) all attracted large fintech deals.

Fintech Investment Expected to Remain Soft into H1’24

Given the ongoing global conflicts, the high interest rate environment, and the continued lack of exits, global fintech investment is expected to remain soft heading into the first quarter of 2024. As interest rates stabilise and possibly begin to decline, investment could begin to pick up. AI and B2B solutions will likely remain big tickets for investors. M&A activity could also start to rebound as investors more seriously look at distressed assets.

“The fintech market has been evolving and maturing since it got its start in 2004 and really came into its own in 2008. The technology underpinning fintech keeps changing—and right now, we’re seeing it change again with the application of AI and generative AI,” said Karim Haji, Global Head of Financial Services, KPMG International. “You could say that we’re coming into the next wave of fintech. While the investment numbers are soft now—due to broader market conditions—the next year could be quite exciting for innovation in the fintech space.”

For media queries, please contact:

Asha Raghu

Manager, Marketing & Communications

KPMG in Singapore

E: asharaghu@kpmg.com.sg

Jeanie Lee

Director, Marketing & Communications

KPMG in Singapore

E: jeanielee@kpmg.com.sg

Brian O’Neill

Senior Manager, Global External Communications

E: Brian.O’Neill@kpmg.co.uk

About KPMG International

KPMG is a global organization of independent professional services firms providing Audit, Tax and Advisory services. KPMG is the brand under which the member firms of KPMG International Limited (“KPMG International”) operate and provide professional services. “KPMG” is used to refer to individual member firms within the KPMG organization or to one or more member firms collectively.

KPMG firms operate in 143 countries and territories with more than 273,000 partners and employees working in member firms around the world. Each KPMG firm is a legally distinct and separate entity and describes itself as such. Each KPMG member firm is responsible for its own obligations and liabilities.

KPMG International Limited is a private English company limited by guarantee. KPMG International Limited and its related entities do not provide services to clients.

For more detail about our structure, please visit kpmg.com/governance.