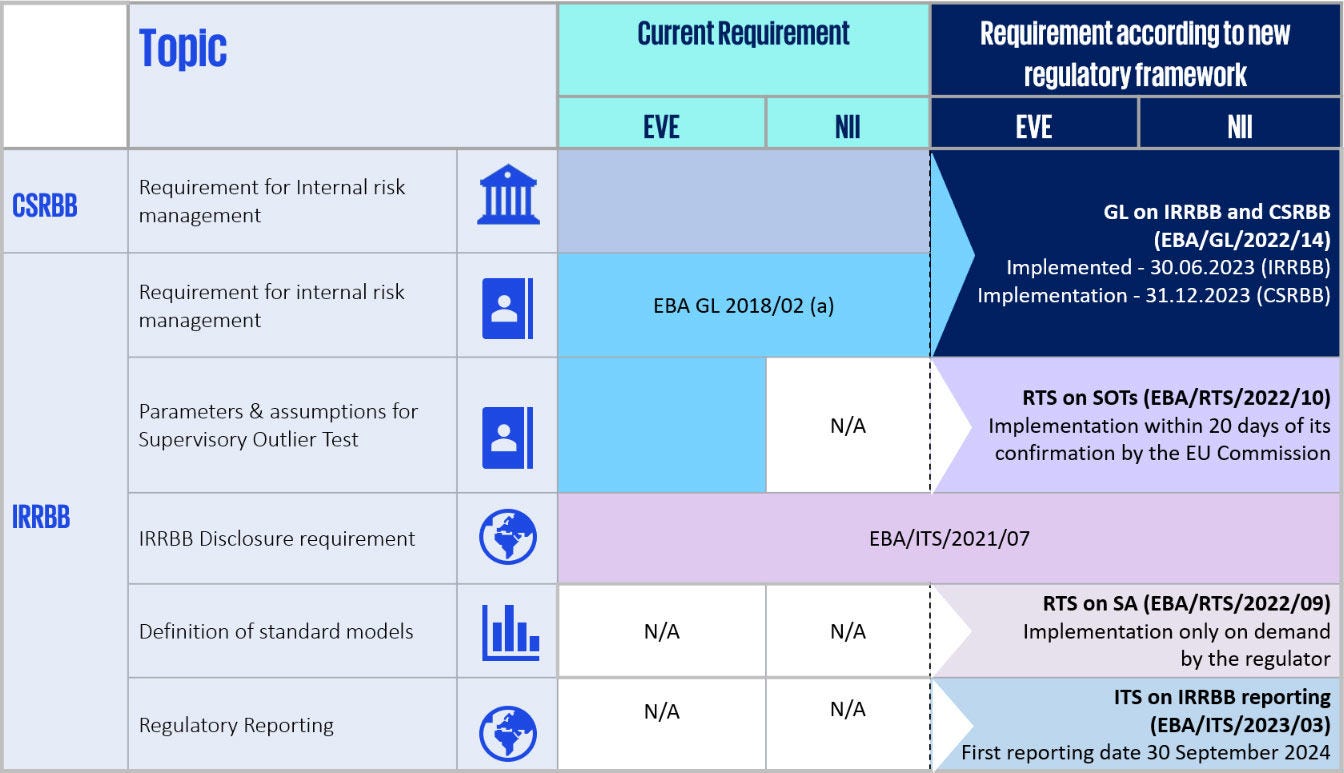

On 20 October 2022, the European Banking Authority (EBA) published a set of new regulatory requirements on interest rate risks for banking book (IRRBB) and credit spread risk arising from non-trading book activities (CSRBB). Ian Nelson and Adrian Toner of our Banking team take a look at these new Guidelines and Technical Standards which are applicable to all banks in the European Union (EU).

Together with Capital Requirements Regulation (CRR) II / Capital Requirements Directive (CRD IV), they complement the regulatory framework for IRRBB and CSRBB. The consultation package comprises:

- updated Guidelines on internal IRRBB and CSRBB management, which replace EBA/GL/2018/02;

- technical guidelines for the updated supervisory outlier test (SOT) for the economic value of equity (EVE) and the introduction of a new outlier test and outlier criteria for the net interest income (NII) perspective;

- technical guidelines for the introduction of two standard models for the EVE and NII perspectives that can be ordered by supervisory bodies if internal procedures are considered inadequate.

On 31 July 2023, the EBA published its final ITS on supervisory reporting with respect to IRRBB (EBA/ ITS/2023/03). The amended final draft ITS equips supervisors with the appropriate data to monitor risks arising from interest rates’ changes.

The new reporting distinguishes between three types of banks, i.e., Small- and non-complex institutions (SNCIs), Other institutions (non-SNCI’s that do not qualify as large institutions - CRR Art. 4(1) item 146) and large institutions. In this regard, the ITS partially include simplified templates for SNCIs and for ‘other’ institutions, which still require a large number of data fields.