Strengthening expectations for credit institutions: the significance of MNB’s new sustainability recommendation and the amendment to the Hpt.

In recent years, sustainability and particularly climate-related risks have gained an increasingly prominent role in the regulation of the financial system. The banking sector is at once a key player in financing the green economic transition and an institutional system exposed to substantial risks stemming from climate change and shifts in the economic structure. Accordingly, European supervisory authorities have placed growing emphasis on integrating ESG risks – that is, risks related to environmental, social, and governance factors – into banking operations.

In Hungary, one of the most important tools of this supervisory approach is the MNB’s green banking recommendation. In 2022, the central bank issued its comprehensive recommendation[1] for credit institutions on the management of climate-related and environmental risks, which for the first time set out system-level expectations for integrating environmental risks into banking operations. However, the rapid development of the regulatory landscape made it necessary to revise this framework, primarily prompted by the European Banking Authority’s (EBA) January 2025 Guidelines on environmental, social, and governance (ESG) risk management. As a result, in March 2026, the MNB issued a new recommendation[2], which significantly clarifies and tightens prior expectations. We provided a detailed overview of the EBA ESG Guidelines in the August 2025 issue of the KPMG Financial Risk & Regulation newsletter.

The new recommendation is more than a simple update: it reflects a clear shift in supervisory mindset. While the prior recommendation mainly served as guidance to help banks recognise climate and environmental risks and begin their management, the new recommendation already formulates much more specific, operational requirements for the full integration of ESG risks into banking operations.

In addition to the new recommendation, the legislative environment surrounding ESG risk management also tightened at the end of 2025. On 16 December, an amendment to Act CCXXXVII of 2013 on Credit Institutions and Financial Enterprises (Hpt.) introduced the obligation to appropriately integrate ESG into credit institutions’ operations. The definition of ESG risk has been added to the interpretative provisions and must be incorporated into institutions’ internal capital adequacy assessment process (ICAAP), their governance and risk management systems, and will be examined as part of the Supervisory Review and Evaluation Process (SREP).

The role of the 2022 recommendation: foundations for the integration of sustainability risks in banking

The 2022 green recommendation was a significant milestone in domestic financial regulation. The aim of the document was to help credit institutions recognise the financial relevance of climate and environmental risks and begin integrating them across different areas of banking operations.

At that time, the MNB primarily aimed to ensure that banks establish the organisational and methodological foundations necessary for managing sustainability risks. The recommendation emphasised that climate and environmental risks cannot be considered as independent risk categories in the traditional sense but may appear in various financial risks – such as credit, market, or operational risk.

Accordingly, the document set out expectations in several areas. In corporate governance, it highlighted the responsibility of governing bodies; in risk management, it required the incorporation of climate risks into the risk appetite framework; and in data management, it required the initiation of ESG data collection and processing.

However, it is important to emphasise that the 2022 recommendation left considerable flexibility for institutions regarding implementation. The central bank’s main objective was to support a shift in mindset and recognised that banks still had limited experience in this field.

Conceptual change in the new recommendation: from climate risks to ESG risks

One of the most important novelties of the 2026 recommendation is the broadening of its focus. While the previous document primarily concentrated on risks related to climate change and environmental factors, the new recommendation covers the full spectrum of ESG risks.

This shift is consistent with broader European regulatory trends. In recent years, both the European Banking Authority and the European Central Bank have increasingly emphasised that sustainability factors cannot be interpreted solely in an environmental dimension. Social and governance factors – such as labour rights, supply chain sustainability, or the quality of corporate governance – can also have significant impacts on the risk profile of financial institutions.

The new recommendation therefore represents an integrated approach in which ESG risks become an organic part of the banking risk management framework. This means that the management of sustainability risks can no longer be treated as a separate area; instead, it must appear across all relevant banking processes.

Expansion of expectations: the new sustainability recommendation in numbers

The new recommendation contains 241 expectations – counting subpoints individually – of which 14 are described as good practices. Forty-four expectations apply exclusively to large institutions, while simplified expectations appear in several areas for small and non-complex institutions.

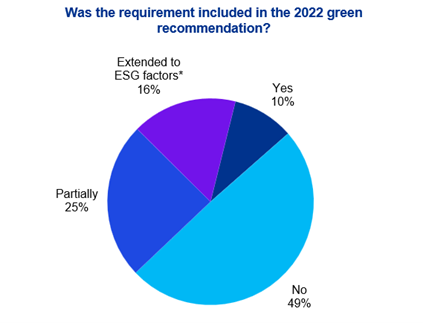

Comparing the new and the previous recommendations, it is evident that expectations have not only been refined and detailed but have also broadened significantly in terms of scope. The figure below illustrates the overlap between the expectations set out in the sustainability recommendation and those included in the 2022 recommendation: