The pace of market polarization in the consumer and retail sector is accelerating. And the implications for companies and brands are real. Expect to see increased divestment and acquisition activity over the next few years.

The disappearance of the middle class

Globalization may have lifted tens of millions out of poverty. Yet it has done little to slow the rising inequality between the top 10 percent of earners and the bottom 50 percent.

Even before the global pandemic, inequality was rising sharply in some markets. Since the mid-1990s – when comparable data started being collected – the gap between the low- and high-income classes has widened, with wealth becoming increasingly concentrated.

The disappearance of the mass market

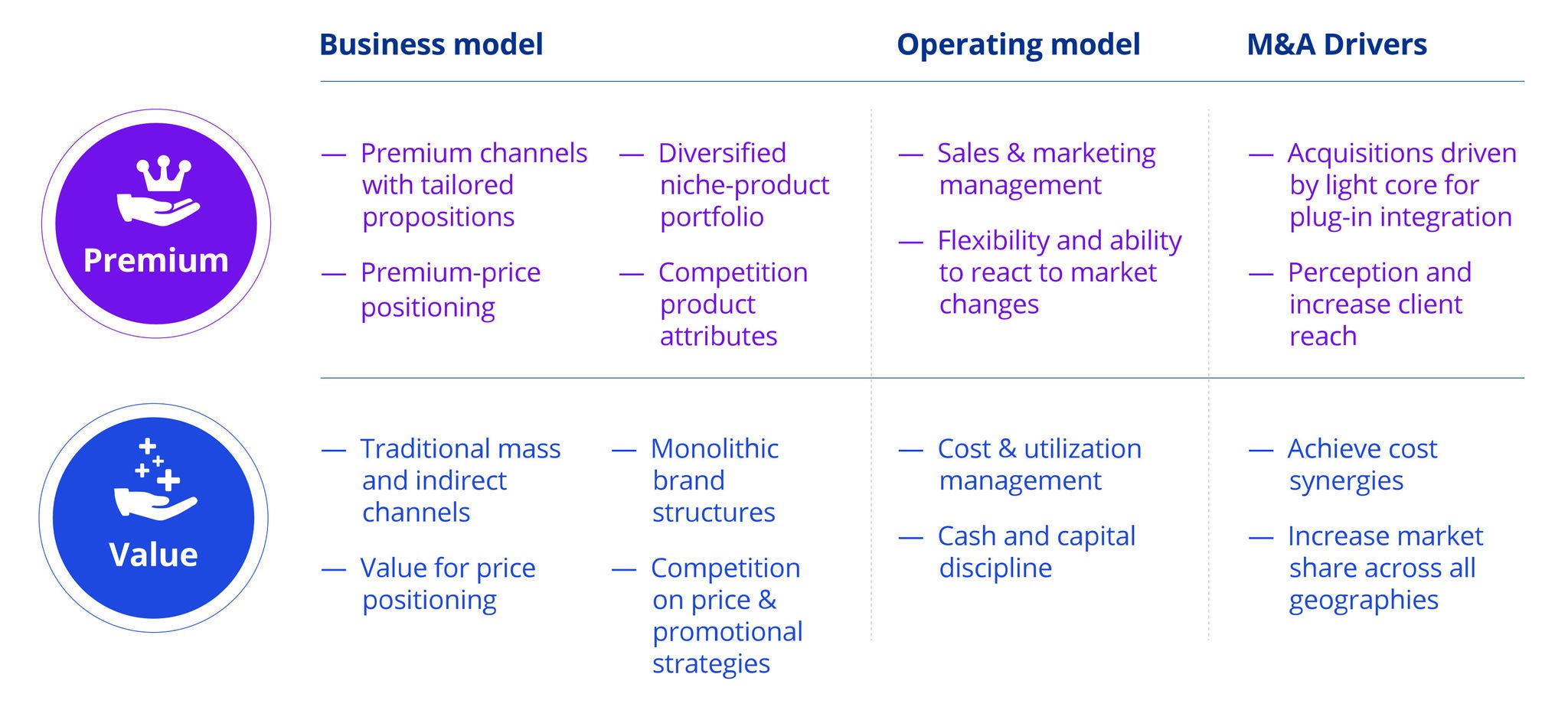

As this gap in income equality widens, markets are seeing the emergence of new customer segments with significantly different purchasing behaviors that gravitate around two polarized segments: ‘Premium’ and ‘Value’.

For FMCG companies, the main challenge lies in the fact that these segments have significantly different business and operating models. While Premium brands usually require sophisticated distribution channels and complex marketing strategies, Value products are mainly driven by cost discipline and economies of scale.

How to grow in a polarized environment

Premium products generally deliver higher margins when compared to their value equivalents. At the same time, the value segment often enjoys a much larger addressable market. A quick look at a ‘basket’ containing different food items clearly shows how premium products deliver higher margins when compared to their value equivalents. Products classified as ‘organic’, for example, tend to deliver higher growth rates than non-organic.

Download the full report to see how each of these segments breaks down in terms of consumer preferences and purchasing behavior.

Market polarization: The implications for FMCG companies

This dichotomy has led many consumer goods leaders to strive to create product portfolios that contain some combination of both premium and value segments. The premium segment represents an opportunity to penetrate fast-growing markets with higher levels of profitability, and value products are key to increasing the existing customer base and enabling economies of scale.

Investors want to go premium

The KPMG analysis suggests that companies with higher shares of premium products among their product portfolios performed better in the capital markets. Indeed, between 2018 and 2022, those ‘premium-oriented’ FMCG companies saw their share prices rise by an average of 89 percent, while those more focused on value products enjoyed an average rise of 4 percent for the same period.

Taking a closer look at the financial data, what investors really seem to be looking for are sustainable growth rates of more than 3 percent per annum and EBIT margins above 15 percent. Miss those targets and – based on the historical data – investors will punish you.

Refining the portfolio

Expect the years to come to bring increased activity in the deal space, with many companies divesting their non-strategic and underperforming assets while looking to acquire attractive brands in promising, fast-growing segments.

Where are the opportunities? Check out the full report to find out where the greatest volume of divestments will likely occur, and which subsectors are ripe for M&A activity.

Key takeaways for FMCG companies and PE funds

You can read more insights by downloading the full report here.

Consumer goods companies

- Shape the portfolio: Thoroughly analyze your current business and brand portfolio in terms of each business’s stand-alone attractiveness, fit to group’s strategy and synergy possibilities.

- Dress the assets: For assets being divested, take time to prepare them for market sounding.

- Set the sail for growth: Organic growth will probably not be sufficient to offset lost revenues amid divestments and you may need to actively search for promising add-on acquisitions.

- Integrate smart and capture value: Having a deal playbook with enough flexibility will likely be key to helping ensure value is captured, particularly in the integration phase.

Private equity funds

- Apply advanced analytics: Anticipate developments early with a forward-looking, data-driven analytical approach to predicting activity on the corporate sell-side.

- Have a vision: Develop a clear roadmap to transform the business over the investment cycle and provide the ‘right’ resources in terms of funding and professional operational support.