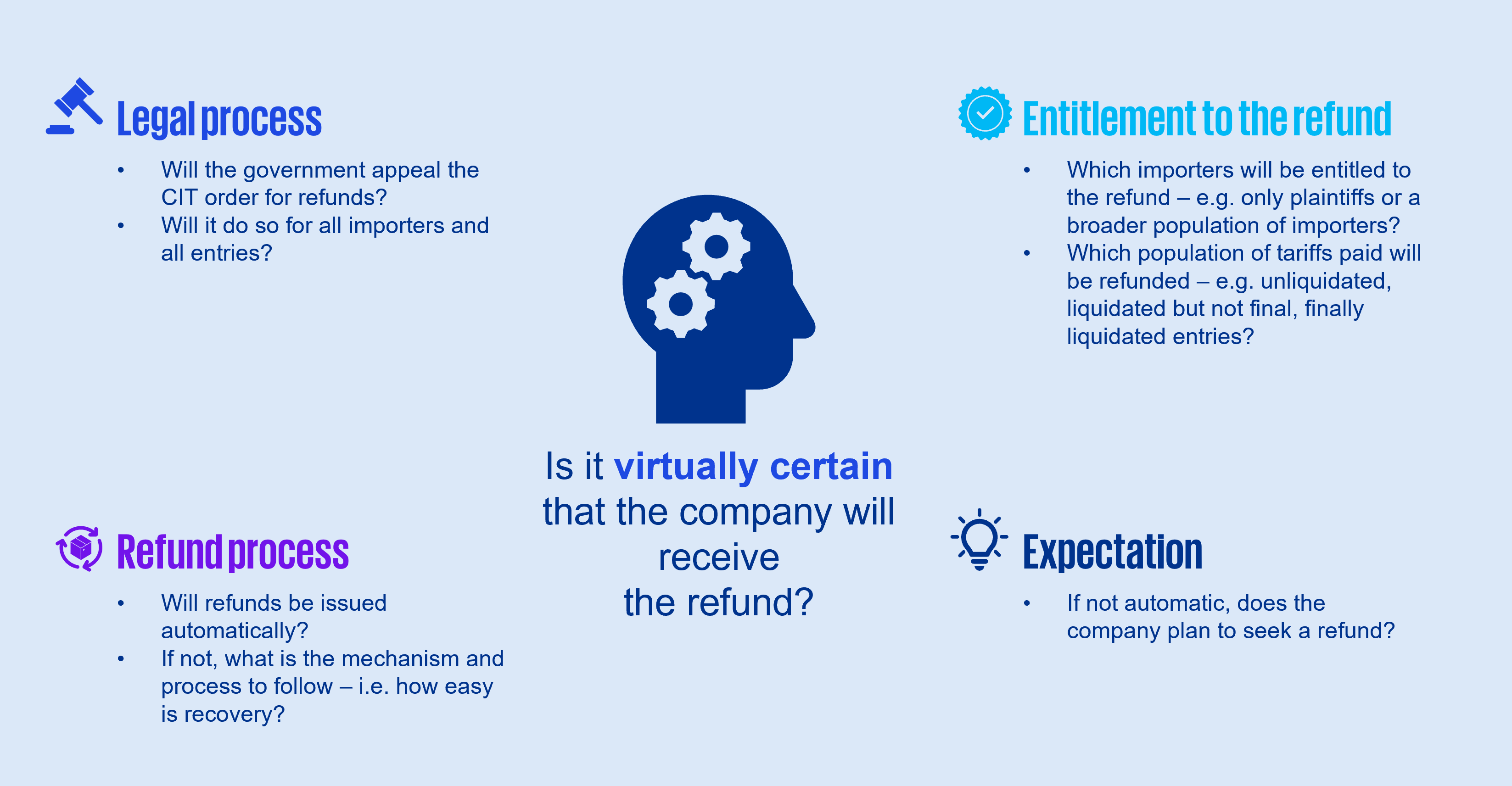

Some companies have paid tariffs on US imports and may now be entitled to a refund. However, there is uncertainty over whether and when refunds would be received.

The situation continues to evolve. Judgement is required to determine whether it is virtually certain at the reporting date that a refund will be received and can be recognised. Clear and transparent disclosures about potential future refunds are critical to providing users of financial statements with relevant information.